April Market Expectations Report

Cautioned Advised For Dip Buyers

Check out my appearance on the Lead-Lag Live podcast/X space, hosted by the award-winning portfolio manager Michael A. Gayed, CFA.

The Ivory Hill RiskSIGNAL™ has remained green since December 5th. Our short-term and mid-term volatility signals have been red since last month, and they are working, as evidenced by the recent sell-off in stocks.

As long as the RiskSIGNAL™ remains green, we believe that stocks will be higher later this year than today.

The S&P 500 is now down nearly 4% from its all-time highs. On the daily chart, early Q2 saw a breakdown through uptrend support, leading to further declines. A key support level was breached last Friday, marking a significant technical downturn and setting the S&P 500 to close at a one-month-low. This breach sets a new near-term target at 5,045, potentially leading to a 5.5% drop from Friday’s close and hitting a two-month low. Monday was also the first close below the 50-day moving average since November.

Small-Caps

We took a stab at small caps at the end of March, but we were stopped last week, so the trade was short-lived. It would have been a lot worse if we hadn’t gotten out when we did. We plan to hold on to that cash and redeploy it as the market gives us opportunities.

This confirms my theory that we are not in a “real” bull market because small caps have been unable to sustain a breakout. They are being weighed down by higher rates.

As long as small-caps stay in their range-bound cycle lows (since November 2021), I still believe we are not in a real bull market. You can’t just have narrow blue chip stocks leading; you need to have smaller and less capitalized companies follow, and we are still not seeing that.

The multi-month uptrend in the Russell 2000 is reversing, and if the 2024 lows are taken out in the weeks ahead, expect a retest of the 2023 lows.

It is also worth noting that the Russell 2000 made a series of higher highs and higher lows in 2007 before completely rolling over during the 2008 Global Financial Crisis, and we are seeing similar price action in the Russell right now.

April Market Expectations Report

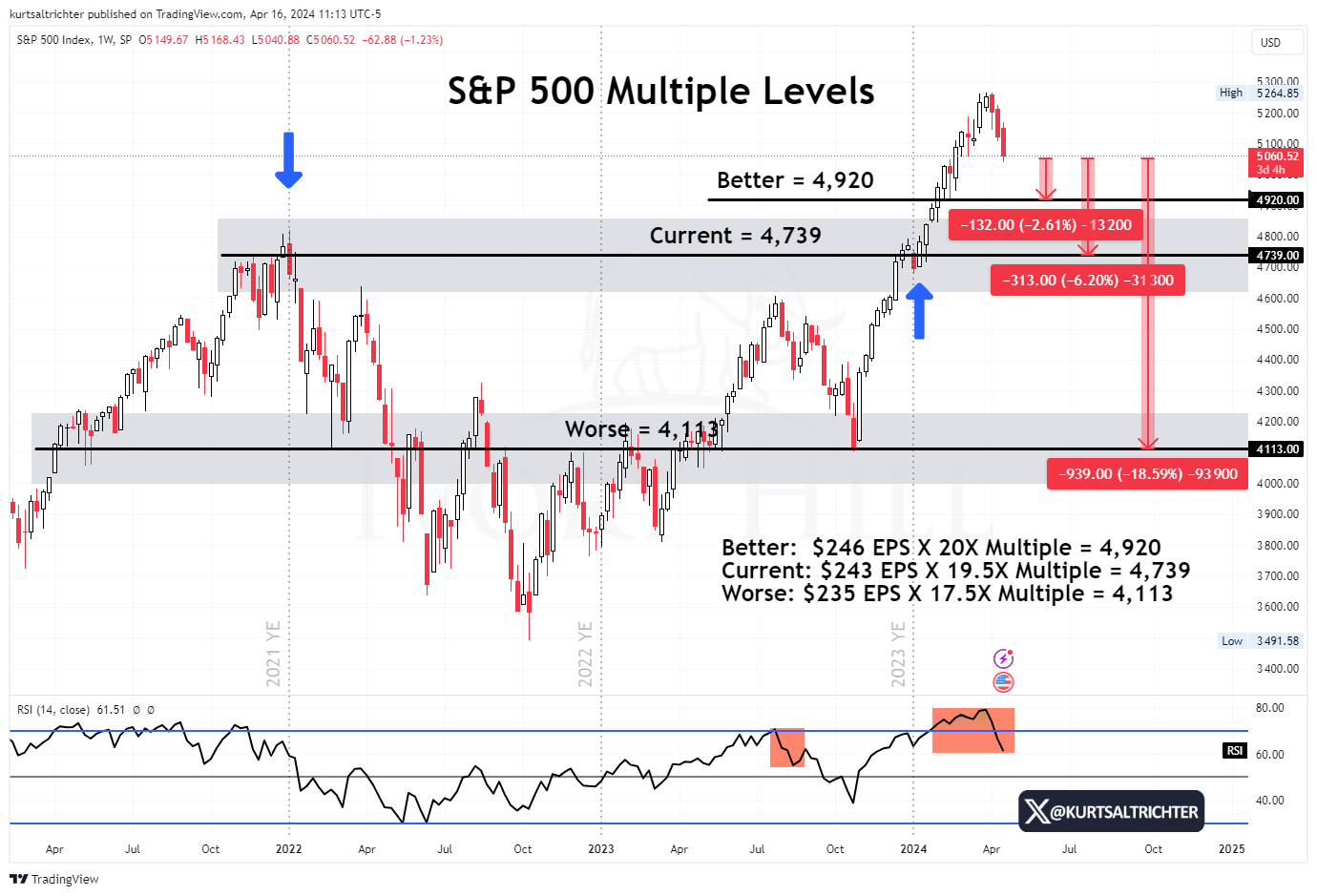

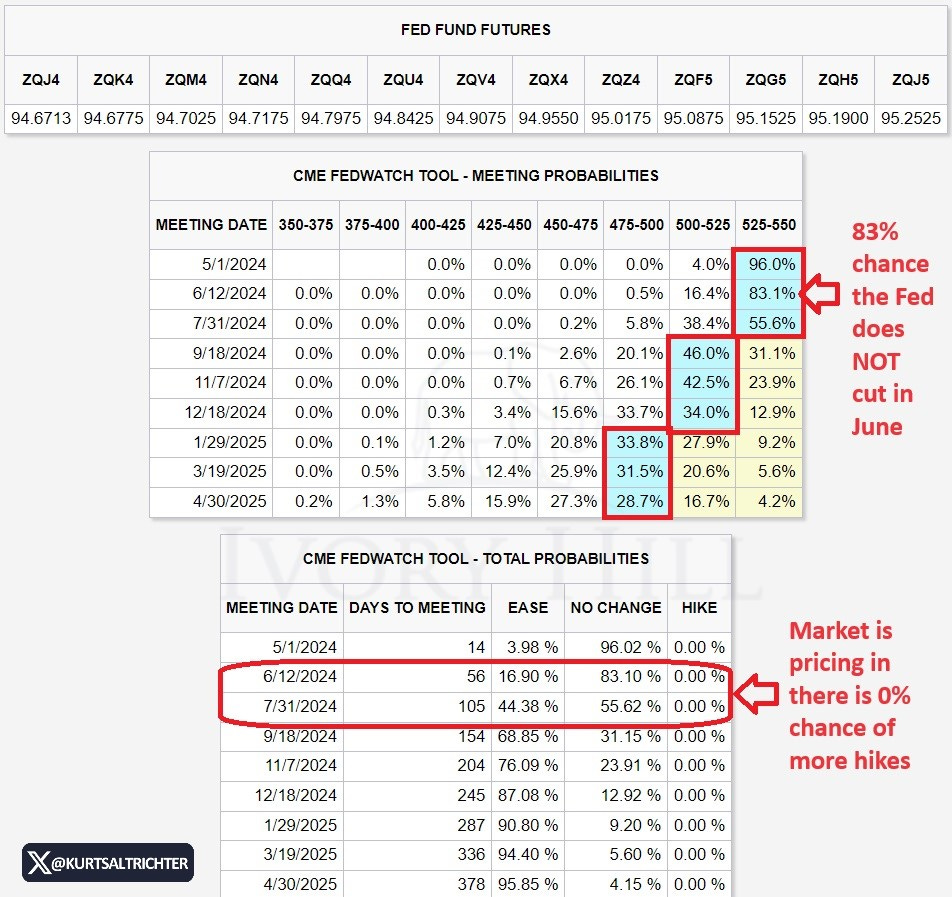

The April Market Expectations Table reveals a significant deterioration across multiple aspects of the macroeconomic environment over the past month, underscoring that the recent decline in stocks is justified and likely to continue unless conditions improve. Notably, three out of five market influences deteriorated last month. Fed expectations were adversely impacted by the “unexpectedly” high CPI report, reducing expectations for a June rate cut and now suggesting no more than two rate cuts in 2024, a sharp decline from the seven cuts anticipated at the start of the year.

In essence, despite the unfavorable news across multiple fronts, the lack of adjustment in fair market value emphasizes that the S&P 500's current level is unsupported by fundamentals. This prompts investors to recognize that the macro environment is not improving, placing downward pressure on stocks and nudging them towards, but not yet reaching, fundamentally supported valuations.

The market expectations table indicates that the recent market pullback is warranted and suggests that stocks are not yet attractively priced fundamentally. Given this backdrop, a further decline in the market is both logical and rational, reflecting not a major trend shift but rather a healthy correction—bringing the market back down to reality.

Current Situation:

The Federal Reserve is resisting a rate cut in June.

Economic growth remains solid but not excessively strong.

The decline in inflation has halted.

AI enthusiasm continues to be strong (for now).

Geopolitical risks are increasing.

The current situation indicates a generally positive setup with solid growth, the potential of easing inflation, anticipated future rate cuts by the Fed, and strong AI enthusiasm. However, this environment is not as favorable as what was observed earlier this year, leading to downward pressure on stocks. Near-term, further market correction should not be a surprise as valuations remain high.

Conditions Improve If:

The Fed signals a potential June rate cut again.

Economic data continues to show "Goldilocks" conditions.

The Core PCE Price Index demonstrates a faster decline in inflation than anticipated.

AI-related earnings maintain strength, and geopolitical risks decrease.

This scenario would signify a return to a near-perfect macroeconomic environment, leading to a rebound towards and potentially beyond previous highs. This would entail ideal conditions for stocks, including imminent rate cuts, strong but not overheated growth, declining inflation, AI enthusiasm, and reduced geopolitical risks, potentially resulting in the S&P surpassing 5,200.

Conditions Get Worse If:

The Fed pushes back on the idea of two rate cuts in 2024.

Economic growth experiences a sudden downturn.

The Core PCE Price Index rebounds.

AI-related earnings disappoint.

In this scenario, the assumptions underpinning much of the rally in Q4 and year-to-date would be undermined, potentially leading to substantial stock declines. A retracement of much of the October-to-present rally could occur, possibly into the mid-4,000s in the S&P 500. While it may seem unlikely given current elevated valuations, this scenario is plausible if data trends unfavorably.

Cautioned Advised For Dip Buyers

Volatility has emerged as a prominent theme in Q2, with the market rally from October lows losing steam and beginning to fade in April. While the recent 4% pullback in the S&P 500 since late March may appear as a potential "buy the dip" opportunity, several factors suggest otherwise:

1. Overbought Conditions: The S&P 500 became overbought in Q1, as indicated by RSI indicators on daily and weekly timeframes, failing to confirm new highs registered in March, signaling concerns about trend sustainability.

2. Market Weakness: Both S&P 500 futures and the S&P cash index fell to one-month lows, suggesting a potential pullback of at least twice the current magnitude is more likely than a quick reversal to new highs.

3. Small Caps: Small caps collapsed and turned negative, mirroring a pattern from 2007, with the Russell 2000 tracking its bearish trajectory, indicating a potential downside resolution. How quickly and sharply small caps turned lower last week was surprising, given that the Fed rate cut cycle is fully priced in. This tells us that investors are not fully trusting that we are truly in a bull market.

4. Sector Performance: Recent sector performance reveal key insights:

a) Consumer is showing weakness

b) Rates will be higher for longer

c) Energy’s outperformance is saying that inflation is not coming down as expected by the market.

d) Recent declines in Technology (XLK) and Communication Services (XLC) sectors have resulted in the loss of their leadership positions. These sectors have significantly contributed to the S&P's gains since October 2022.

5. Treasury Yields: Treasury yields surged to multi-month highs, with the yield curve bear-steepening reminiscent of patterns preceding the 10% correction last summer.

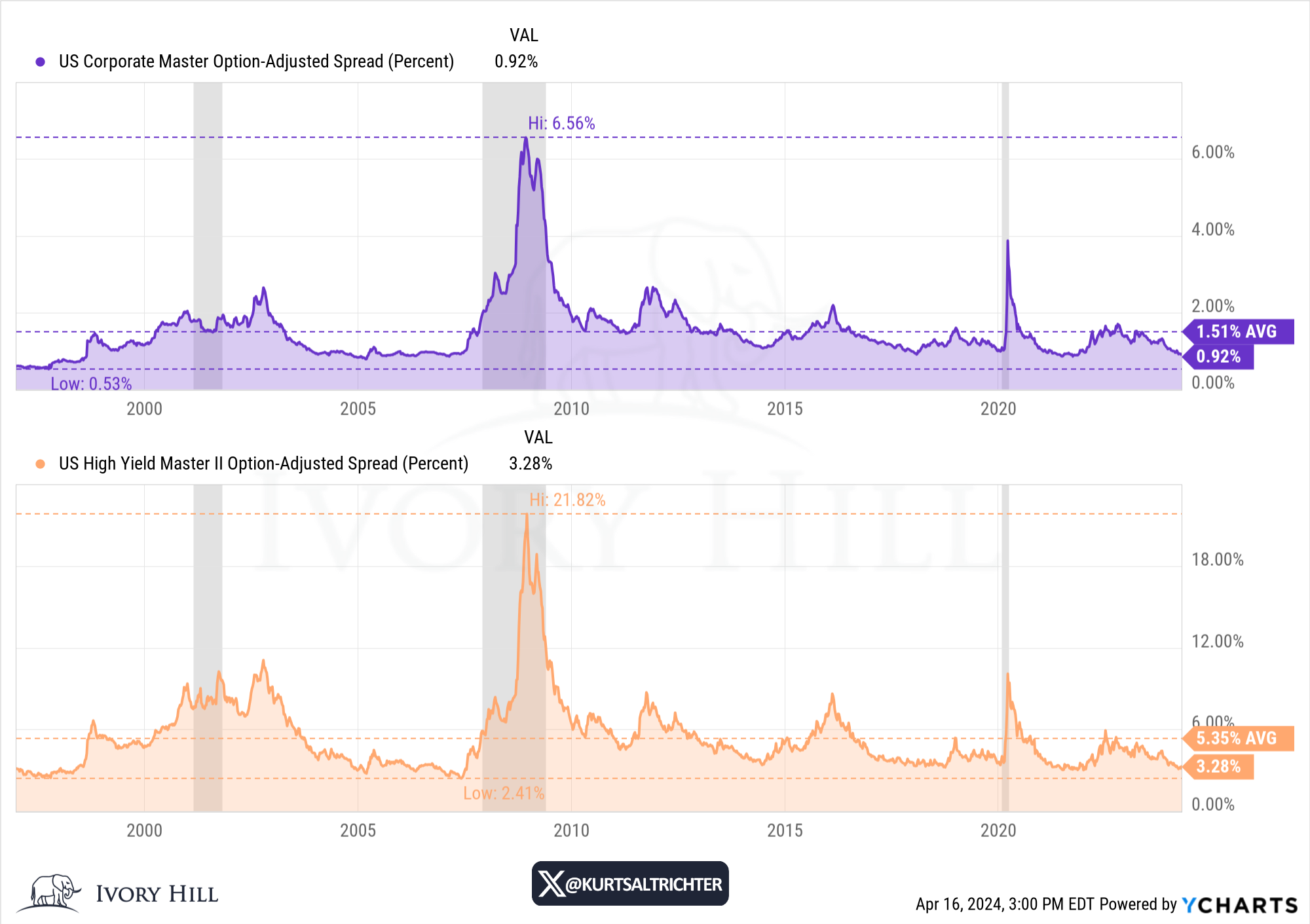

6. Real Rates: Real rates surpassed 2%, historically associated with stock market losses and higher volatility, while credit spreads, though tight, show negative dynamics for risk assets.

7. Credit Spreads: Credit spreads are narrow, but internal dynamics are unfavorable for risk assets. Safe-haven Treasury yields have risen, while high-yield debt has not participated in the risk-on rally in Q1. Additionally, junk-debt yields reached new highs in 2024 last week, signaling a cautionary note for risk assets.

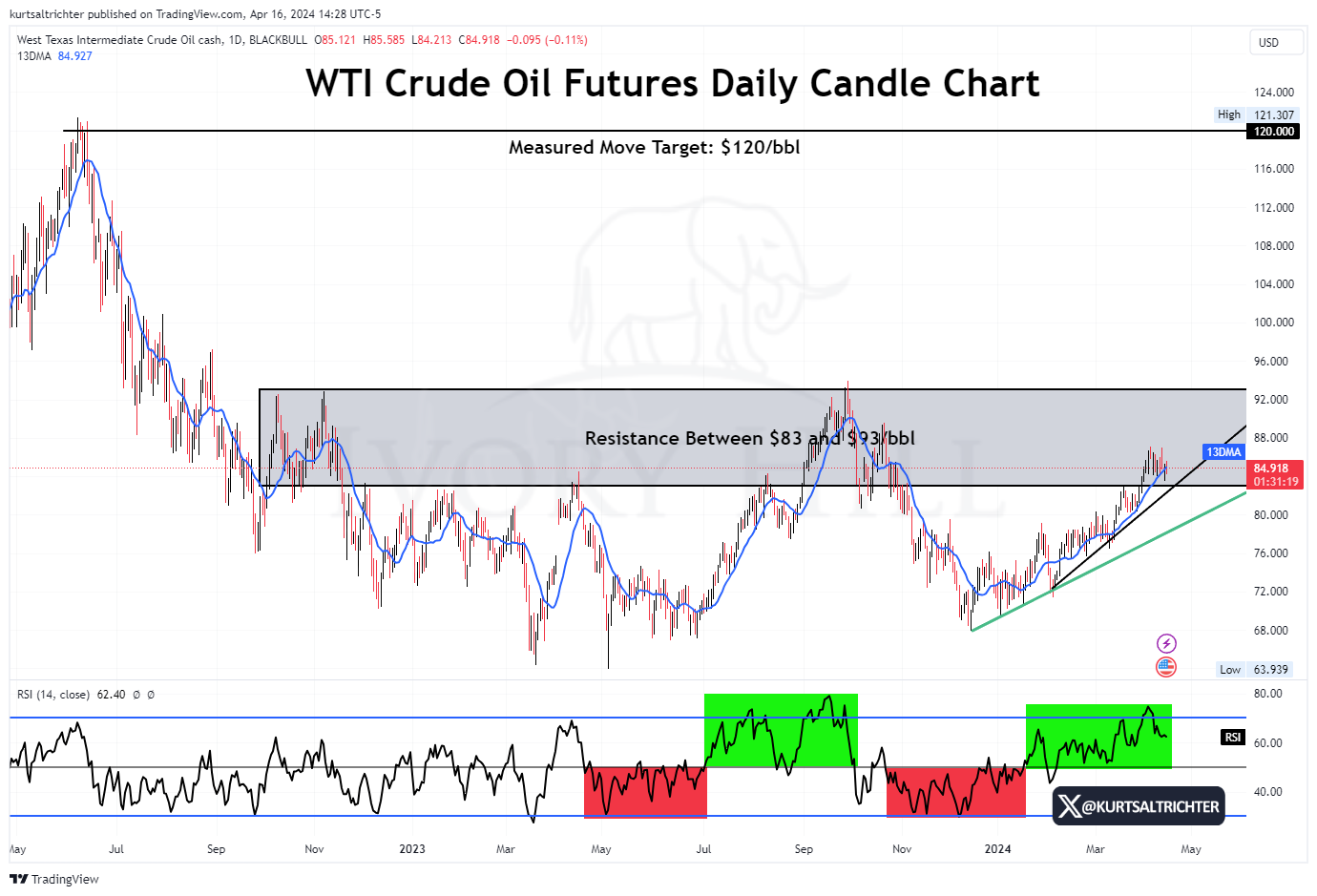

8. Geopolitical Tensions: Escalating geopolitical tensions pose upside risks to oil prices and inflation.

9. Dollar Strength: A firming dollar presents risks to U.S. corporate earnings as a stronger dollar makes US goods and services more expensive for foreign buyers, reducing demand for exports. This can lead to lower revenues for US companies that rely heavily on international sales.

10. Indicators: Indicators such as the VIX, SKEW, and Put/Call Ratio suggest that sophisticated investors are on edge, with the potential for volatility to reach 52-week highs in the coming weeks.

11. Fed policy expectations have turned notably hawkish compared to earlier in the year.

Bottom line: the risks of buying stocks at current levels outweigh the potential rewards. Waiting for a deeper pullback or confirmation of new highs would offer better entry points.

While the RiskSIGNAL™ remains green, we will be laser-focused on finding entry points into this market.

If the RiskSIGNAL™ flips red, we will not hesitate to raise cash levels.

Looking ahead

I still think that slowing economic growth will ultimately kill this rally, which is not priced in at all.

An economic slowdown would bring the current multiple of 19.5X down to roughly 15.5X, so with 2025 earnings at $240/share, it would not be surprising to see a 1400-point selloff (27% downside on the SPX from today's level).

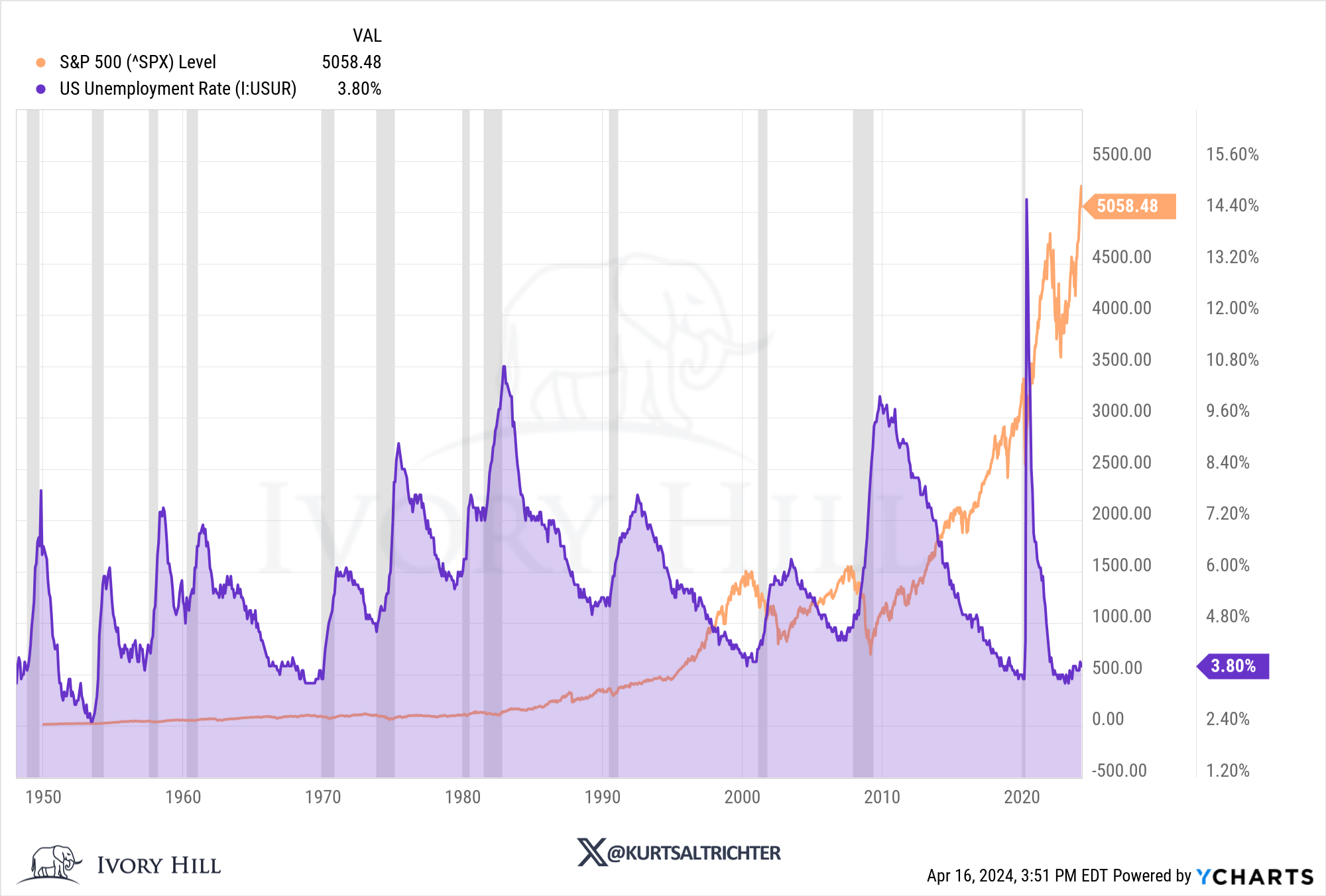

The unemployment rate is the best indicator of slowing economic growth right now.

If unemployment rises above 4% and approaches 5%, this would kill all economic growth momentum. If/when this happens, you will want to exit this market.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President