Evidence of Cyclical Progression

What's Next?

I will be out of the office from September 16-24 for my wedding and honeymoon in Italy. Like many business owners, I won’t be completely disconnected and will be monitoring market conditions, but my response time will be slower during this period.

The Ivory Hill RiskSIGNAL™ has remained green since December 5, 2023, but is now showing significant signs of deterioration.

While the longer-term trend remains intact, each pullback brings us closer to a red signal. Further downside price action will be needed to trigger a red signal, prompting a more definitive reduction in equity exposure.

Last week, the Ivory Hill Pivot Point™ signaled a sell during the pullback. We reduced exposure to high-beta and leveraged equities by about 20%, which was then put back on today when the Ivory Hill Pivot Point™ turned back up.

Our pivot point trading system is specifically designed to risk-manage high-beta and leveraged equity positions. Keep in mind: when volatility is trending lower, we want a higher concentration in risk assets. Our investment strategy performs best in low-volatility, steady (boring) market conditions and seeks to protect capital on the downside during higher volatility conditions.

Lessons From Past Recessions - Four Technical Indicators to Watch

As I've been pointing out for some time now, this market has an 85% correlation with the summer of 2007. After analyzing the strongest correlations, I've narrowed it down to four key technical indicators that are critical to watch closely. You will see these charts in every report until these conditions change.

The VIX

During late-cycle phases, the VIX typically stays low, forming a pattern of lower highs as investor complacency sets in, with a growing number of short-volatility trades in response to resilient equity markets. Notably, each recent recessionary bear market has been preceded by the VIX reaching a 52-week high.

Recession Signal Triggered August 2nd, 2024

The Yield Curve

An inverted yield curve during an equity bull market should not be overlooked, but it’s also not an immediate reason to sell, as significant cyclical bull market gains often happen during these inversions. The key recession signal to focus on is rapid bull steepening in the 10Y-3M spread.

Recession Signal Not Yet Triggered

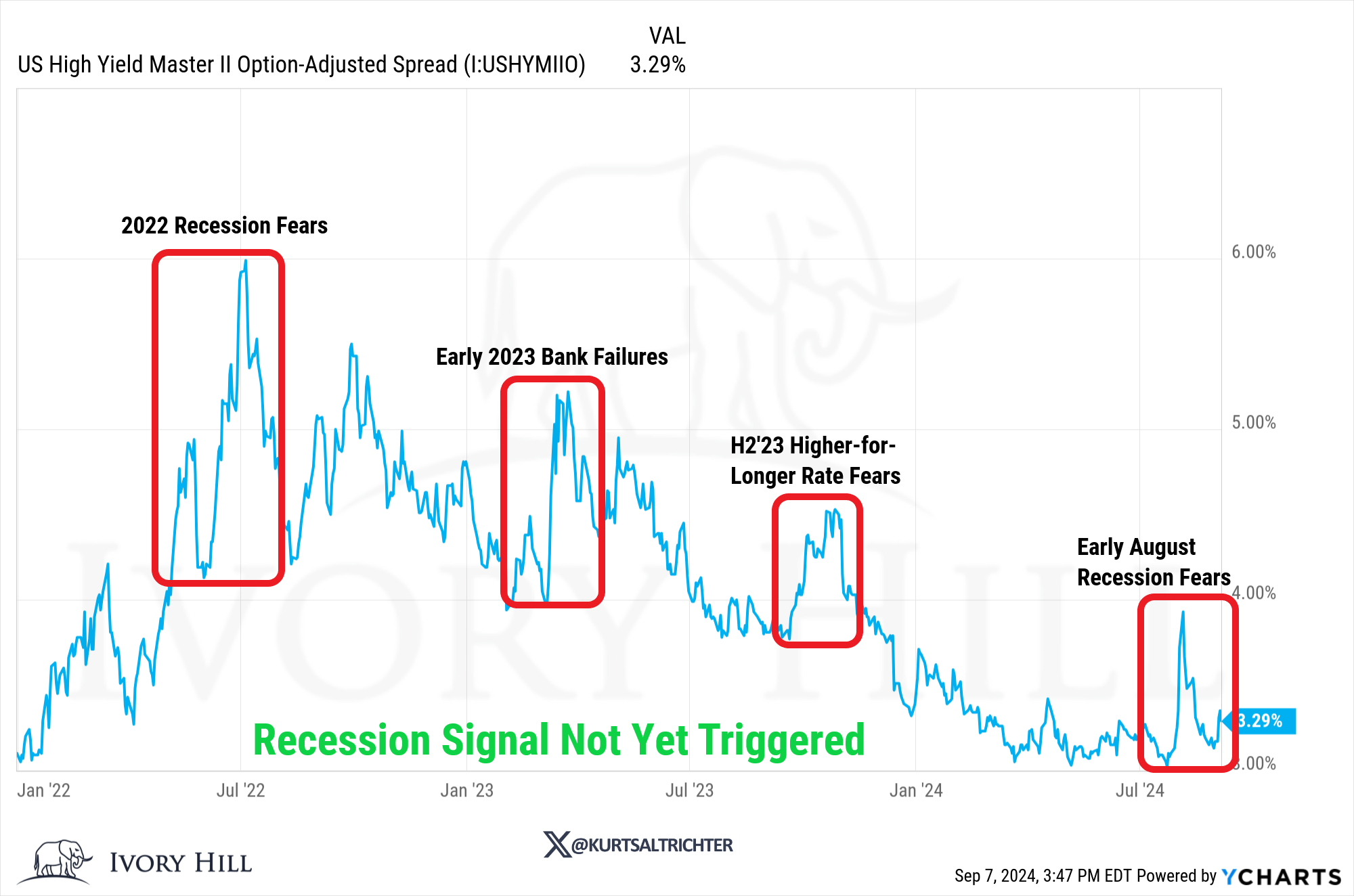

Credit Spreads

Historically, credit spreads have been a valuable indicator for equity investors, as tightening often reflects strong risk-on flows into stocks and high-yield corporate bonds. However, a sharp widening to 52-week highs in credit spreads serves as a key warning sign of a potential recession.

Recession Signal Not Yet Triggered

S&P 500 Price Pattern

The S&P 500’s price movements can provide valuable insights into whether the market is approaching a cycle peak. As the last "domino to fall," a pullback in the index, followed by an unsuccessful attempt to reclaim recently set record highs, often signals a recessionary pattern seen at market tops.

Recession Signal Potentially in Progress

Bottom line: Currently, 1 out of 4 recession signals have been triggered, with a second on the horizon if the S&P 500 continues its decline. If all 4 signals activate, even investors with a very long-term time horizon should seriously consider reducing their equity exposure, as it could take years to recover losses and reach break-even levels.

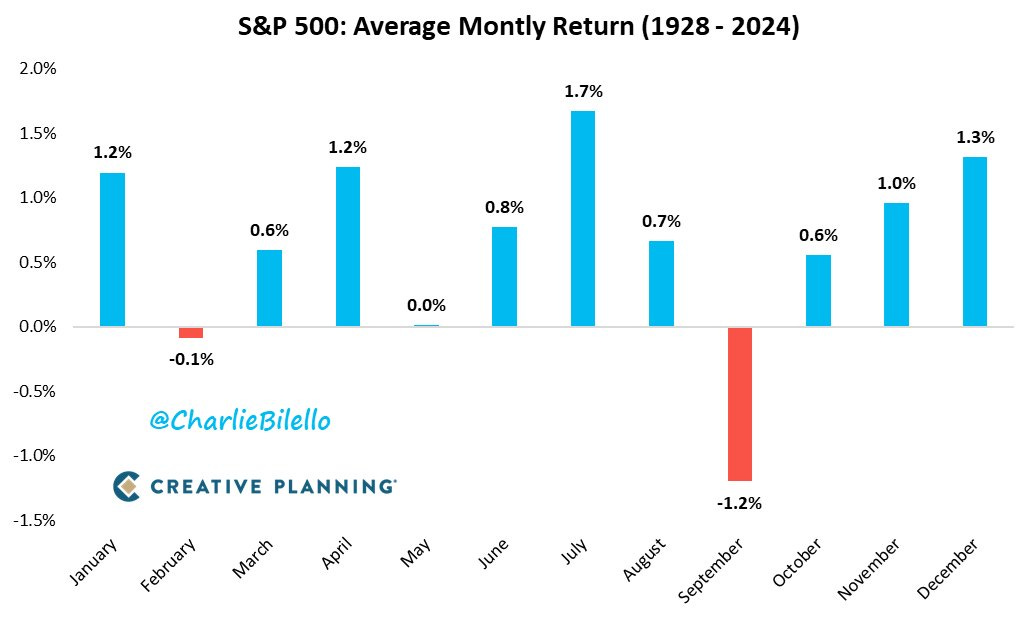

Historically, September has been the toughest month for the U.S. stock market, averaging a -1.2% return since 1928. This year is no exception, as the S&P 500 has already dropped more than 4% so far this month.

The 10Y-2Y Yield Curve Turns Positive: Is It Time to Panic Sell Stocks?

Last week, the 10Y-2Y yield curve spread moved back into positive territory, climbing from a flat 0.00 in the previous week to +6 basis points by Friday's close. This upward move was driven by bull steepening, contrasting with the bear steepening from the week before—a pattern that tends to be less favorable for equity investors during this stage of the economic cycle.

Historically, the 10Y-2Y spread has been a leading indicator for faster-moving spreads like the 10Y-1Y and 10Y-3M. Despite the 10Y-2Y spread’s rise, the 10Y-3M spread dropped by 11 basis points, remaining deeply inverted at -141 basis points. While the shift in the 10Y-2Y spread is concerning and shouldn't be written off as an “it's different this time” situation, the ongoing inversion of the 10Y-3M spread indicates that the economic cycle may prove more resilient than many, including myself, have expected.

It’s important to note that in the 2000 cycle, the 10Y-3M spread hit its lowest point in December, about nine months after the stock market peak in March, indicating that the market can top out even with a still-inverted 10Y-3M spread.

Bottom line: Take note of this, but there's no need for immediate action. Stocks can still post significant gains from here, even after yield curves turn positive, so there's currently no reason to shy away from equities (yet).

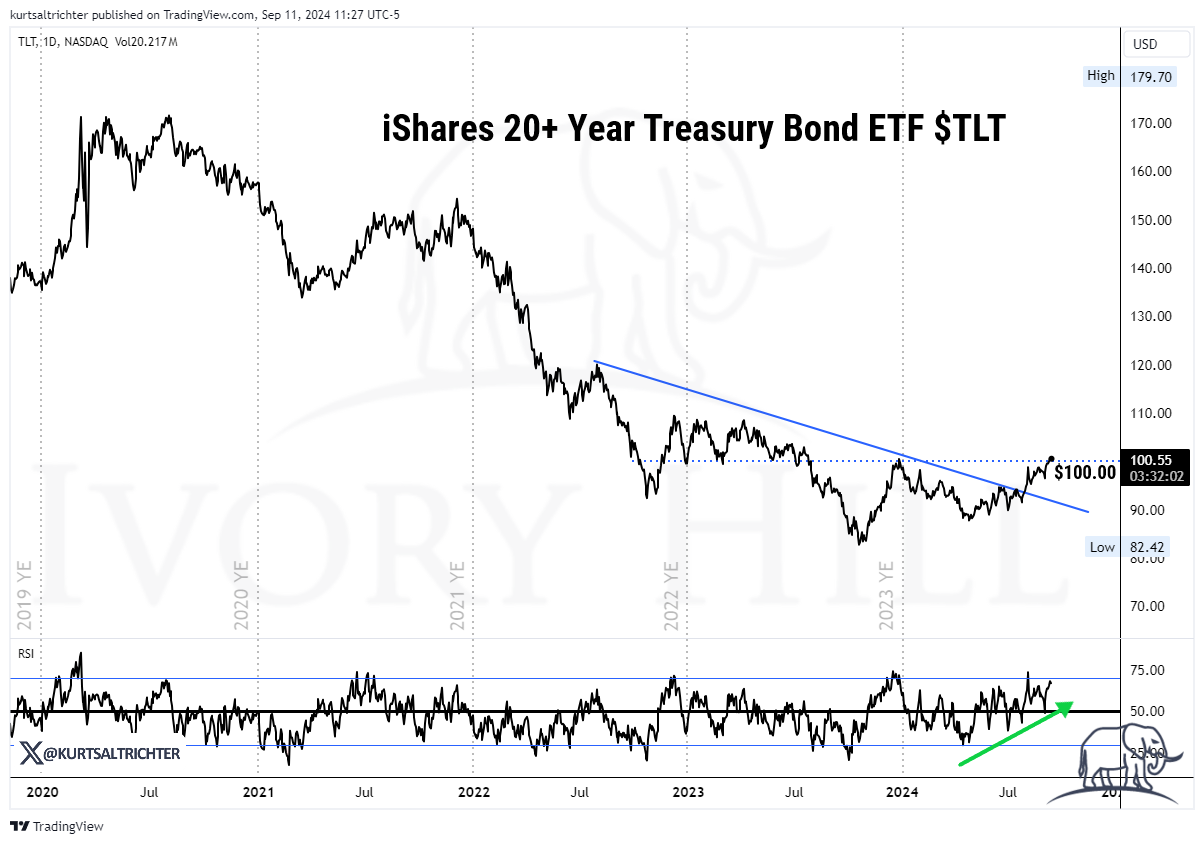

The Time is Now For Treasuries

Long-term Treasuries are steadily climbing, fueled by renewed recession fears. At this stage, the market has already priced in about 100 basis points in rate cuts by year-end, a sentiment that has been holding for several weeks. The rally is becoming more driven by a shift towards safety, with last week's labor market data acting as the catalyst. We'll see if this week's inflation numbers trigger a similar reaction.

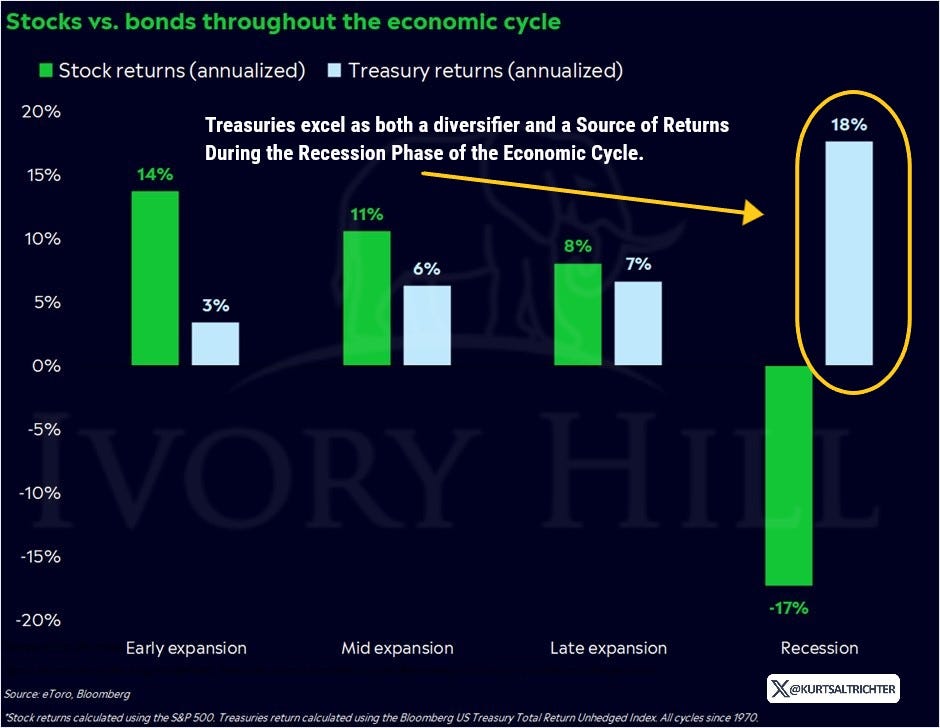

Here’s a chart illustrating the varying, yet consistently positive, correlation between stock and bond market returns across three of the four major phases of the market cycle—early expansion, mid-expansion, and late expansion. During these phases, the largest difference in returns is 11%, seen in the early expansion phase, though bonds still managed a positive 3% return, even in their weakest phase. However, during the final recession phase, a significant divergence occurs, with stocks and bonds showing an inverse correlation. Stock returns typically fall by 17% on an annualized basis during recessions, while Treasuries deliver a robust 18% return in these periods.

We're positioned in long-term Treasuries through ETFs like TLT, UBT, and TMF as we near the end of this economic cycle, where this strategy should pay off. The iShares 20+ Year Treasury Bond ETF is currently down 40% from its March 2020 peak. I like this trade because, as interest rates fall, bond prices will inevitably rise. In a true flight-to-safety scenario, where panicked investors are selling everything, Treasuries won’t behave like traditional bonds—they’ll trade more like stocks. This could lead to a significant rally in TLT as equities decline.

If inflation continues to decline, we can expect TLT to maintain its upward trend. However, if inflation expectations rise in the coming months and quarters, TLT will face another selloff. This is a strong possibility, especially considering that inflation remains significantly higher for many essential goods.

Is the Magnificent 7 Trade Over?

Concentration remains exceptionally high in this market. Despite Nvidia being down over 20% since its June all-time high, the overall strength of mega-cap tech stocks is under pressure.

The tech sector is now at a one-year low relative to the broader market, signaling that the era of the "Magnificent 7" trade could be nearing its end. Although mega-cap stocks may still shine in certain scenarios, the market is clearly worried about the global economy slowing too fast. When that happens, growth stocks lose appeal, and valuations contract. It’s highly likely that this trend will continue as we approach an impending credit event.

To make matters worse for the AI trade, the SOX plunged 12.22% last week, decisively breaking below its 200-day moving average. The daily RSI indicator sharply declined, and its relative strength against the S&P 500 fell to levels not seen since early January. The SOX is now at a critical juncture.

Critical Trends Shaping the Economy

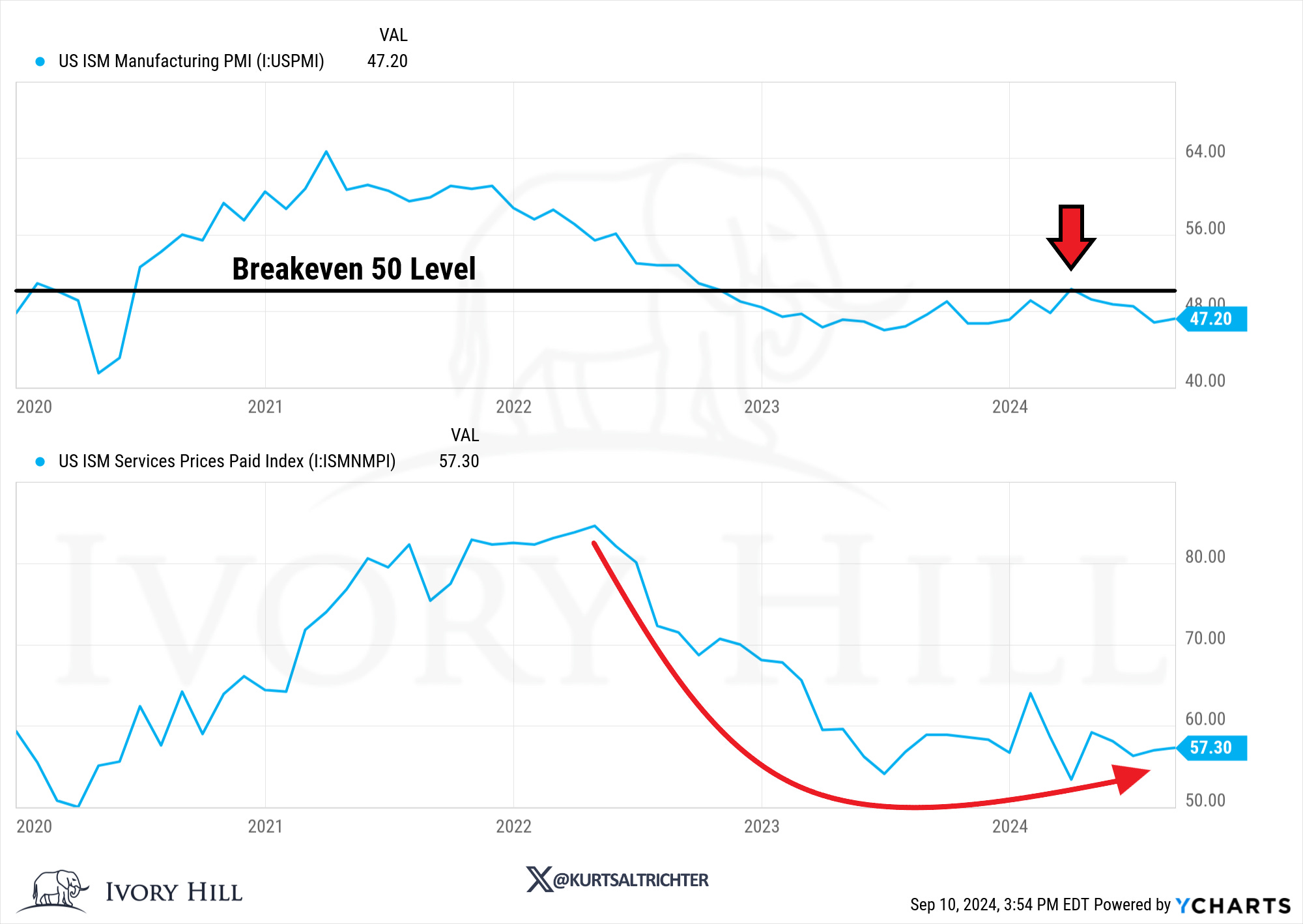

Last week’s economic data painted a clear picture of stagflationary pressure. The ISM Manufacturing Index, a widely trusted leading indicator for economic cycles, fell short of expectations and remained significantly below the breakeven level of 50, which marks the divide between expansion and contraction. Sitting just below 48, the ISM reading for the manufacturing sector confirms that contraction continues into the second half of 2024.

Jobs data further highlighted economic stress, with the July JOLTS report revealing fewer available positions than anticipated. While the August BLS report showed a slight drop in the Unemployment Rate from July’s peak, the three-month average continues its rise and now sits above 0.5%—a recession signal with a flawless historical accuracy of 100%. On top of that, the ISM Services Index delivered a seemingly positive headline, but underlying details were less encouraging, particularly the Prices sub-index, which ticked upward and may signal renewed inflationary pressure.

In summary, deteriorating employment figures coupled with persistent inflation suggest that the economy is edging closer to stagflation—a scenario that would be particularly challenging for investors if it fully materializes.

As I’ve been emphasizing all year, the second half is shaping up to be particularly challenging to navigate. I continue to anticipate significantly higher volatility as we approach the election. As the chart below shows, we could be on the brink of experiencing some serious market turbulence ahead. We will continue to stick to our rules-based approach.

The bond market, known for its agility and responsiveness to real-time economic indicators, often anticipates the Federal Reserve's next move. Unlike the Fed, which is constrained by institutional processes and cautious decision-making, the bond market reacts quickly to shifts in economic data like unemployment, growth, and inflation. This forward-looking nature allows bond prices and yields to adjust rapidly based on the collective expectations of market participants. In contrast, the Fed operates with an intentional delay, making policy decisions based on past data. As a result, the Fed is inherently slower to raise or cut rates, always reacting to what has already occurred rather than being proactive.

In conclusion, our latest cross-asset analysis indicates that, despite the current rally off late 2022 lows being extended and economic cycle risks at their highest since 2007, the equity bulls still have the upper hand. As highlighted in the chart above, the average performance gap between Treasuries and stocks widens by 35% in the next economic phase. Therefore, taking advantage of equity rallies to adopt a more defensive stance in portfolios is likely to prove beneficial as the cycle unfolds.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Email: kurt@ivoryhill.com | ivoryhill.com