Expect Near-Term Volatility: Strategic Capital Deployment

Allocating Capital Amidst Market Uncertainty

The Ivory Hill RiskSIGNAL™ has remained green since December 5th. Our short- and mid-term volatility signals turned red on Friday, so increased volatility should be expected in the coming days and weeks.

We are fully invested in this market and favor less risk and lower beta stocks as volatility has increased.

From a positioning standpoint, we are rotating a portion of our equity exposure from higher-beta stocks to lower-beta stocks. This allows us to lose less during a market sell-off but not completely miss a rally if it is a false signal.

Last week, the S&P 500 remained flat, defying the recent trend of near-automatic rallies in the market. Despite several positive factors at play—the Goldilocks-like jobs report, Powell's indication of a potential rate cut in June, and reassuring inflation data—the market failed to respond with the upward momentum that investors have been addicted to lately. Why? Because these developments were already factored into the current market price, hovering around 5,140 in the S&P 500.

Let's be clear: the absence of negative news doesn't equate to an absence of risks. The jobs report, while falling within the 'Just Right' zone, also revealed a rise in the unemployment rate to 3.9%, its highest since January 2022. This aligns with other indicators suggesting a loss of momentum rather than outright weakness in the economy: high continuing claims, lukewarm ISM Service and Manufacturing PMI, lackluster retail sales, and a slowdown in consumer demand across various sectors.

While these indicators don't signal an imminent recession, they do hint at a potential slowdown in economic growth—a scenario not fully accounted for in current stock prices. This presents a significant vulnerability for the market. Despite the overall strength of the economy and the low immediate risk of a slowdown, the market remains vulnerable to surprises.

With the S&P 500 SPY 0.00%↑ at 5,100, there's no room for complacency. Any signs of slowing growth could trigger a rapid correction of 5%-10%, driven by stretched sentiment and unrealistic valuations.

While the economy stands firm, the risk of an unexpected deceleration in growth looms. Investors must remain vigilant, as these market conditions leave little margin for error. Acknowledging this possibility is crucial to navigating potential drawdowns and preserving investment capital in uncertain market conditions.

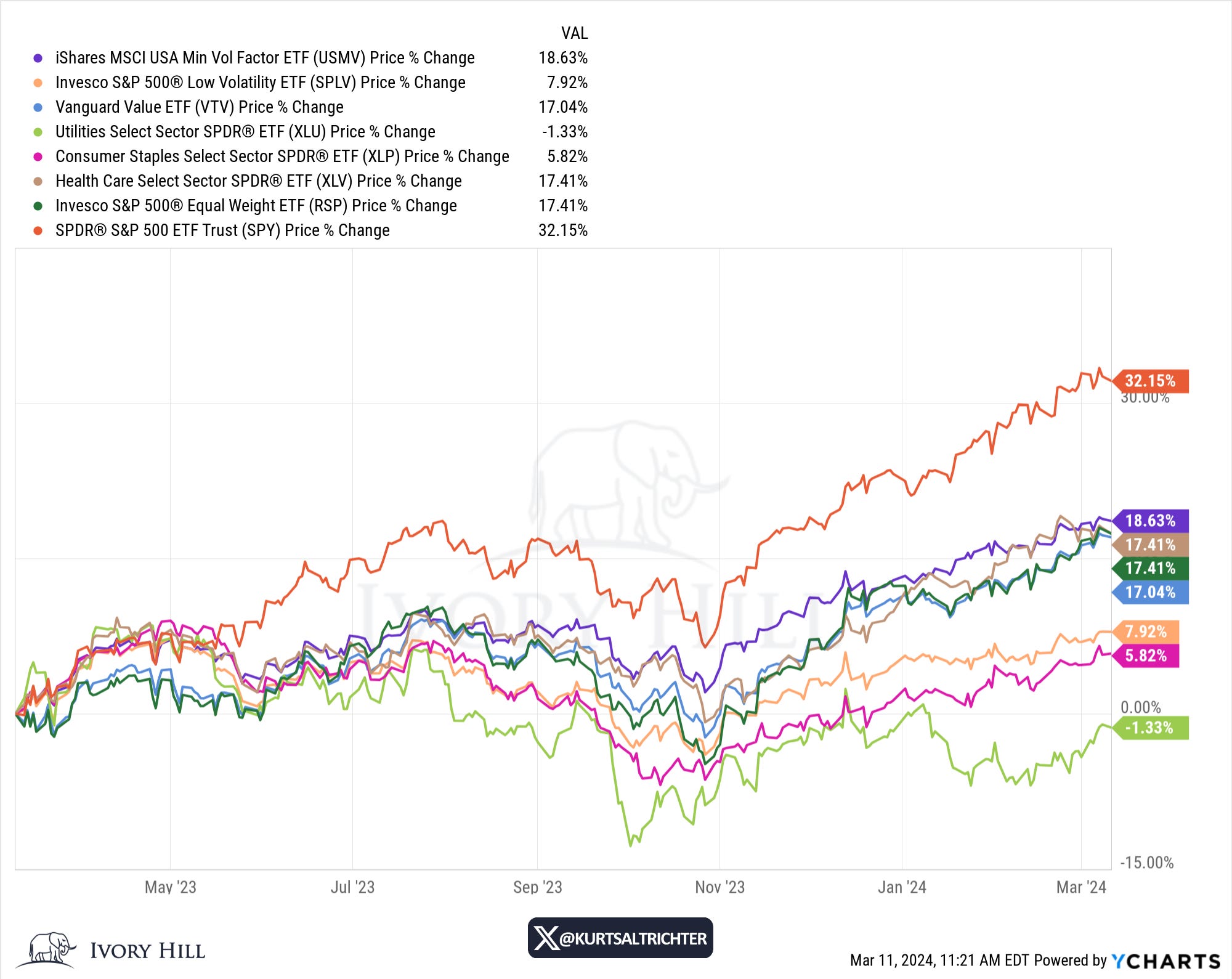

What has my attention right now is Gold, Utilities, and Treasuries.

The utilities sector XLU 0.00%↑ saw a significant surge of 3.29% last week, marking the highest weekly return among the major S&P 500 sectors. This is concerning and reinforces my view that we should anticipate increased volatility in the coming weeks.

Utilities are the most “bond like” sector in the equity markets. Therefore, observing such a robust and rapid outperformance last week suggests that traders are getting more defensive. They are selling overvalued tech stocks and reallocating capital into defensive sectors like utilities.

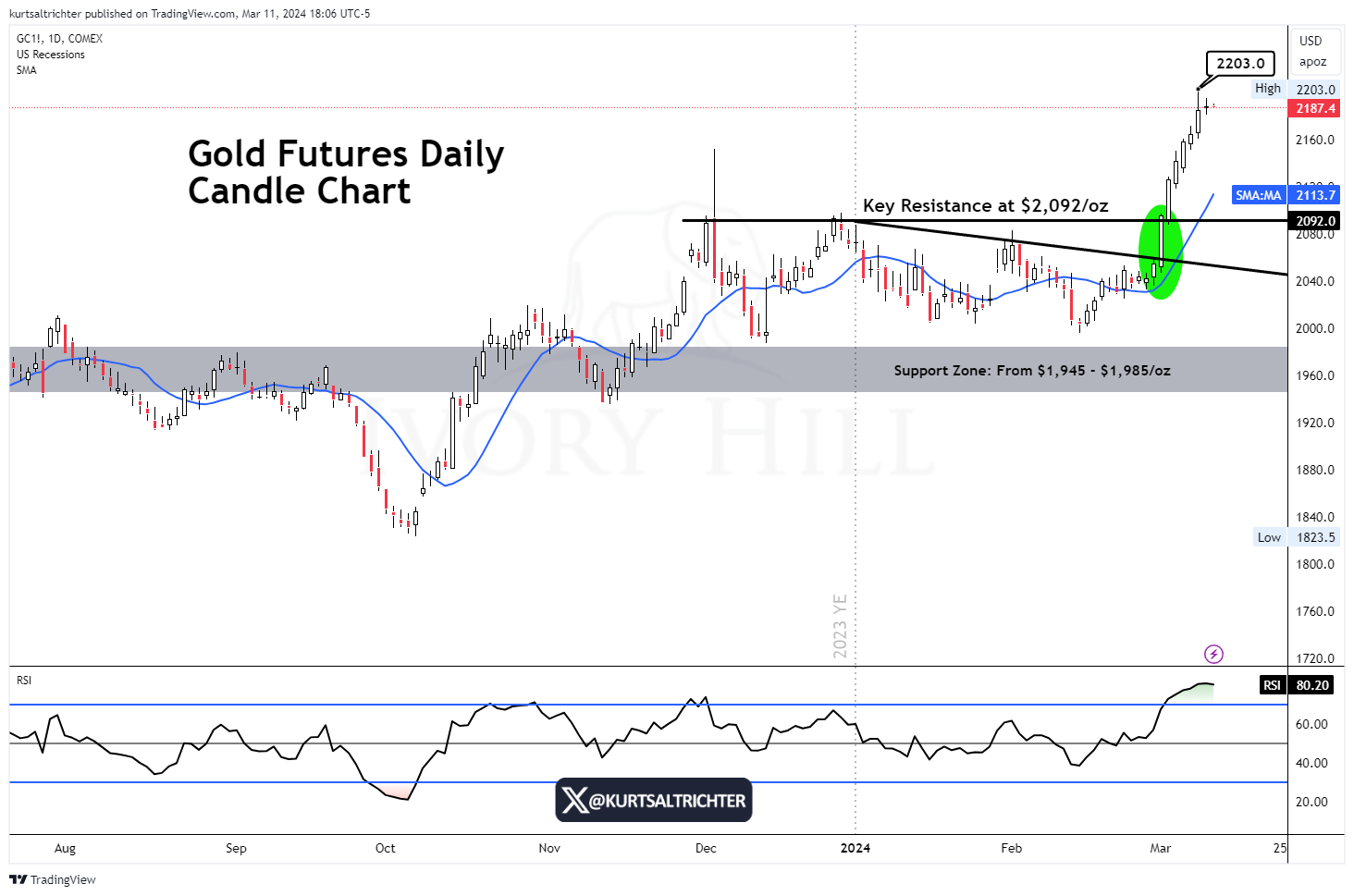

Gold surged higher last week, breaking decisively above previous records set in late 2023, and futures consistently closed at new record levels every day. While I acknowledge that gold may be overbought at this point, and a retracement towards previous highs is plausible, it's the long-term bullish trend that worries me. Similar to utilities, witnessing another defensive asset sharply outperforming indicates a parallel narrative.

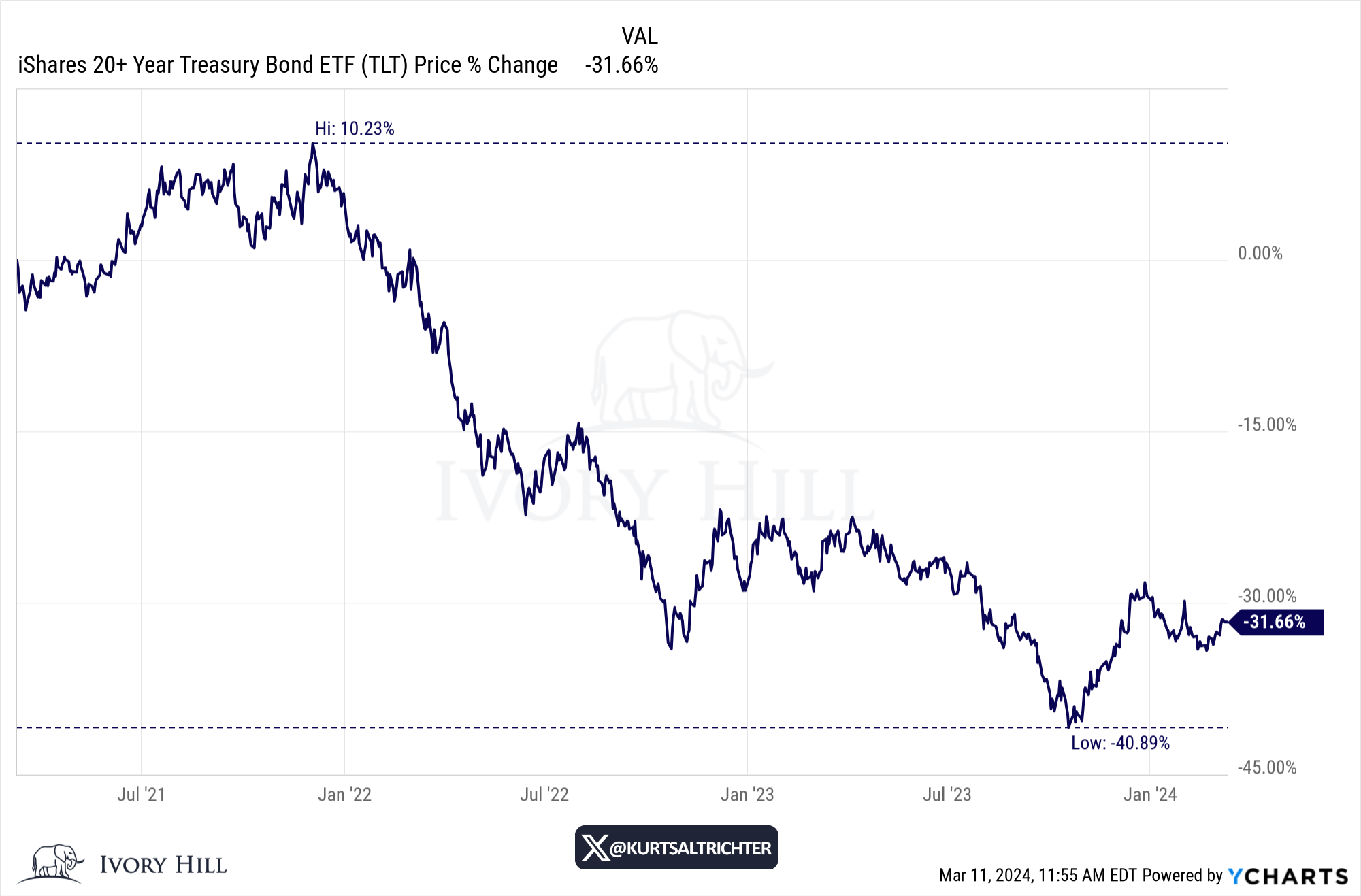

Last week, Treasuries also demonstrated strong outperformance. Notably, all three—gold, utilities, and Treasuries—exhibited significant rallies, hinting at a shift in sentiment that may be underway.

Amidst these developments, it's important to highlight that we also witnessed a substantial selling week in bubble-cap tech stocks.

Investors who have heavily relied on bubble-cap tech for performance are now confronting a potential period of prolonged underperformance, especially with the unemployment rate inching higher and the yen setting up to possibly disrupt global markets.

Is it the time to massively reduce risk? We could just be entering a phase where the tech sector is pausing for a breather while other market segments catch up, but only time will reveal the true outcome that is why I am not advocating to raise cash levels.

Small-Caps

Small-caps continue to hold a prominent position, underscoring my unwavering focus on their significance. For this to truly be a broadening stock market, rather than merely a collection of individual stocks, it's imperative for small-caps to not just break out but sustain an upward trend over months and quarters. Not days and weeks.

In terms of relative strength compared to the S&P 500, the Russell 2000 continues to hold below a long-established downtrend. However, since October, an uptrend has emerged, resulting in the Russell being confined within a narrowing range relative to the S&P 500.

In the weeks ahead, it will be crucial to closely monitor for a clear breakout in either direction, as this will offer valuable insights into the future trajectory of the Russell 2000 and by extension, the broader market.

Notably, the occurrence of new 52-week highs and lows within a short period of time creates what chart followers call a "broadening triangle" price pattern. Historically, this pattern aligns with investor uncertainty and a lack of conviction.

Here are a few stats to refresh your memory:

99.9% of businesses in the U.S. are small businesses (33.2 million)

46% of Americans are employed by a small business (62 million Americans)

Small businesses drive 43.5% of America’s GDP

Until rates come down, I expect small businesses to struggle.

Where should you deploy new capital into this market?

This is the #1 question I have been getting from clients, investors, and other advisors I consult.

Given that valuations are stretched and we are on the brink of the “euphoria” stage of this cycle, for long-term equity investors I am favoring lower volatility USMV 0.00%↑ SPLV 0.00%↑ value VTV 0.00%↑ and defensive sectors like XLU 0.00%↑ XLP 0.00%↑ XLV 0.00%↑ and for core equity exposure, the equally weighted RSP 0.00%↑ .

If we get any hint of slowing growth backed by hard evidence, these sectors and styles should outperform or, at the very least, go down less than the rest of the market. On the flip side, if this rally stalls and churns sideways, there is much room for these sectors to play catch-up in a generally rising macroeconomic environment.

If the AI bubble-cap tech rally continues to push the market higher, these sectors and ETFs will ride the wave. They won’t outperform tech, but you won’t be left behind. This is all about how you risk-manage your portfolio and set expectations for yourself.

As I have been saying for some time now, long-term bonds, like TLT 0.00%↑ , are still a generational buying opportunity for more patient investors. When we inevitably have a credit event or a spike in the VIX, this is where you will see outperformance.

We will likely see Powell continue to kick the can down the road on rate cuts, and between now and a credit event, I would expect long-term Treasuries to go sideways until we get an actual sell-off. For investors looking to speculate on long-term Treasury prices, TMF 0.00%↑ or UBT 0.00%↑ could be an option as well.

As an investor aiming to achieve retirement plan goals, where most individuals seek a net annual return on capital of approximately 5%-6%, extending Treasury duration could prove beneficial at this juncture. Put plainly, if your retirement plan only requires a 5%-6% net return on capital, it's prudent to secure 4%-5% through long-duration Treasuries. However, if you're comfortable with higher risk and aim for equity-like returns over the long term, this strategy may not align with your objectives.

Keep in mind that FOMO is real. I have dealt with clients who consider themselves conservative investors (who can’t stomach a 20% downside) and are now concerned about missing out on this parabolic move in equities, so ensure that you have expectations set if you go this route.

If you can’t stomach a 20% drawdown in your portfolio, you should not invest in equities, especially in this market. The price you pay for long-term gains is volatility. So, being down 20% should not be surprising (should be expected at some point) because no one can control the market.

As advisors, our role is to consistently guide clients through navigating their emotions in the market. During periods of euphoria when the market is surging and speculative assets are on the rise, investors often feel compelled to take on more risk, fearing they'll miss out on potential gains. Conversely, during market downturns of 30%-50%, the instinct is to liquidate holdings out of fear of losing accumulated wealth, when in reality, it may be an opportune time to purchase equities. The clients who avoid fixating on their portfolios that achieve the best long-term returns. However, maintaining this discipline is easier said than done, particularly given studies that connect the fear of missing out (FOMO) with physical pain.

This is why sticking to your investment strategy is more important than what you are investing in. Said differently: if your goal is to lose weight, I don’t care what diet you follow; as long as you stick to it, you will eventually lose weight over time. You will not get the desired results if you change your diet every 30-60 days. The same goes for investing.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President