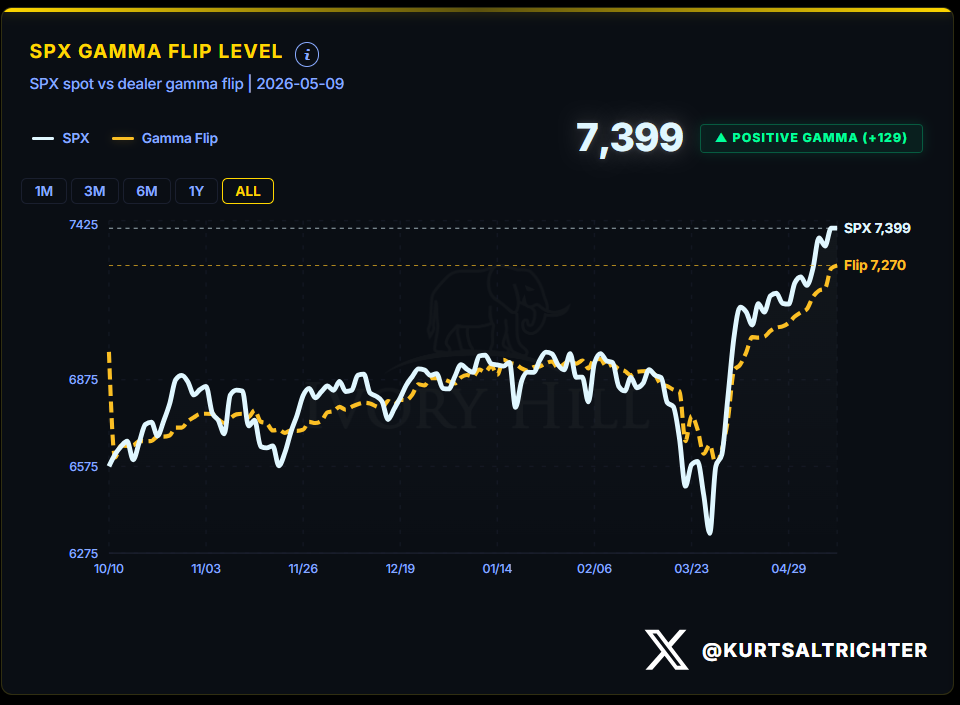

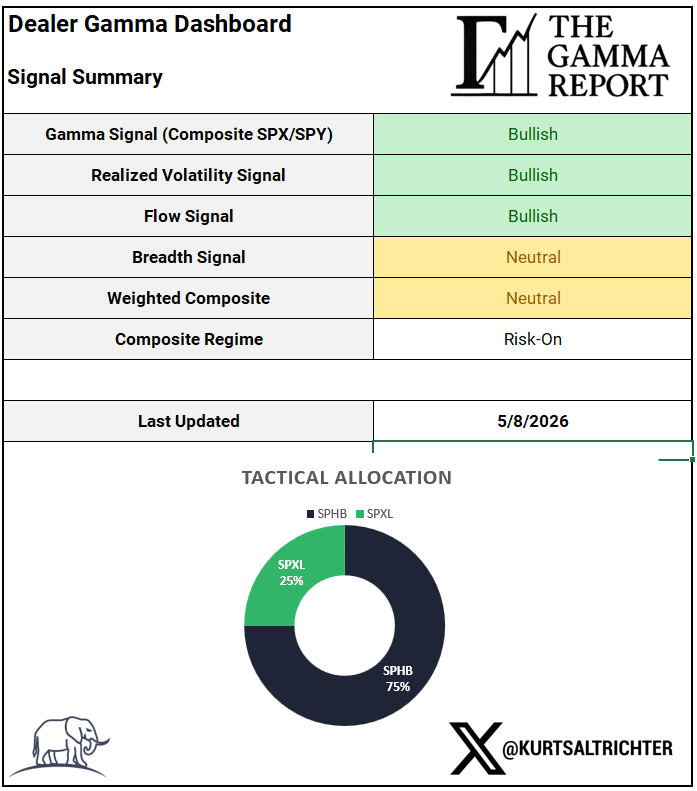

The model has held Risk-On for five consecutive weeks. The structure is clean. Realized volatility is in a low-vol regime. Systematic funds are adding. The gamma flip is rising with the price above it.

CPI drops on Tuesday. The options market is pricing a ±1.05% move. That is the event that can either confirm the bull case or reintroduce volatility that the market is not pricing. Everything else this week fills in around it.

THIS WEEK’S GAME PLAN

Risk-On for the fifth consecutive week. The allocation stays 75% SPHB / 25% SPXL.

The S&P 500 closed Friday, May 8 at 7,399. The gamma flip sits at 7,270. Dealers are operating in positive gamma territory, 129 points above the flip. That cushion keeps dealer hedging flows stabilizing rather than amplifying price moves. Realized volatility has collapsed. The 1-month RV printed 10.61. The 3-month is 14.76. Both readings place us firmly in a low-vol regime. Systematic funds added to long exposure all week. Breadth sits at 55% of S&P 500 members above their 200-day moving average. Neutral territory, but trending in the right direction.

The composite regime is Risk-On. The tactical allocation is unchanged.

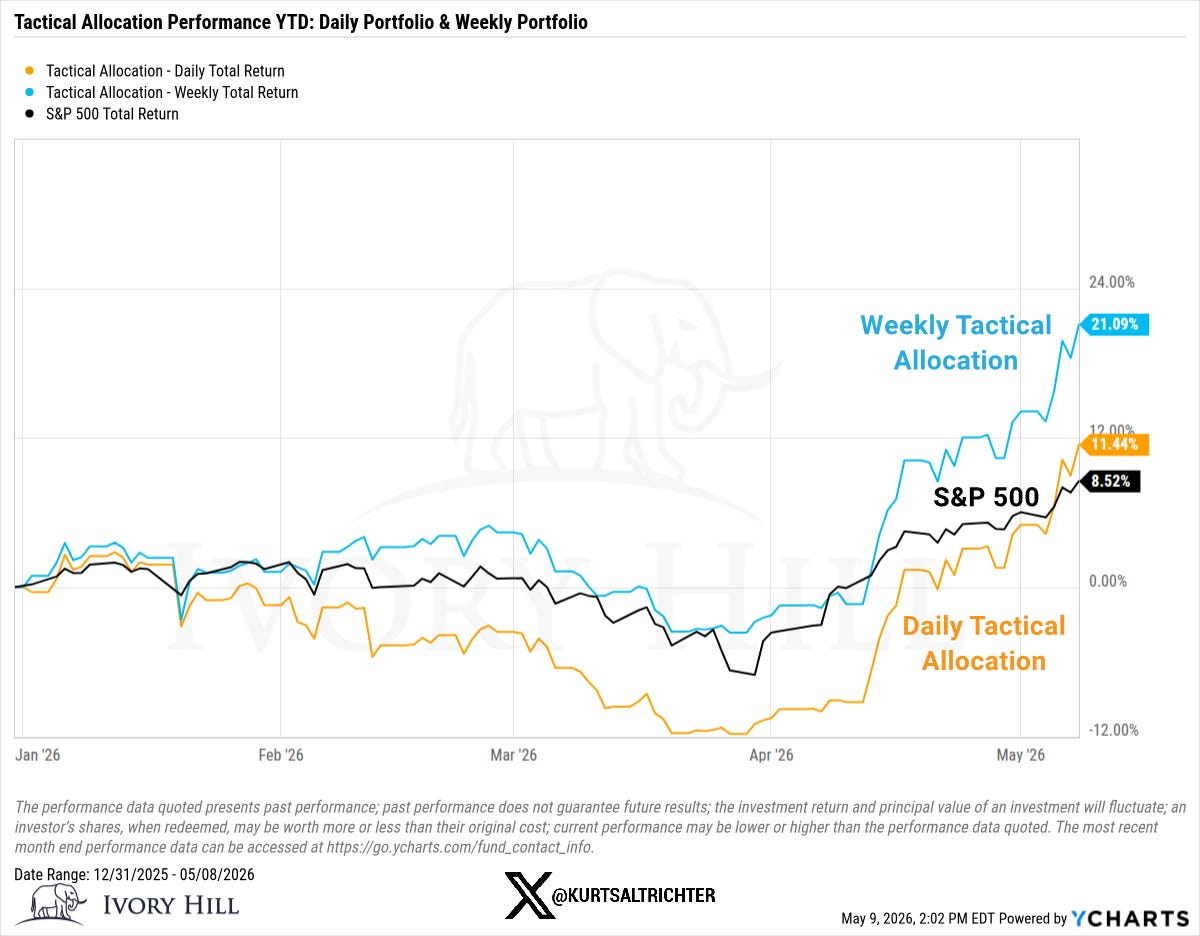

TACTICAL ALLOCATION PERFORMANCE

Year-to-date through May 8, 2026:

Weekly Tactical Allocation: +21.09%

Daily Tactical Allocation: +11.44%

S&P 500 Total Return: +8.52%

The weekly strategy is leaving both the daily strategy and the S&P 500 in the dust since the April low. The alpha gap between the weekly allocation and the S&P 500 TR now stands at 12.57%. The daily portfolio, which weathered deeper drawdowns during the February through March volatility period, has recovered to 2.92% above the index.

Both portfolios were positioned defensively as the market deteriorated. Both rotated into risk when the regime was confirmed. The performance difference is the output of that process.

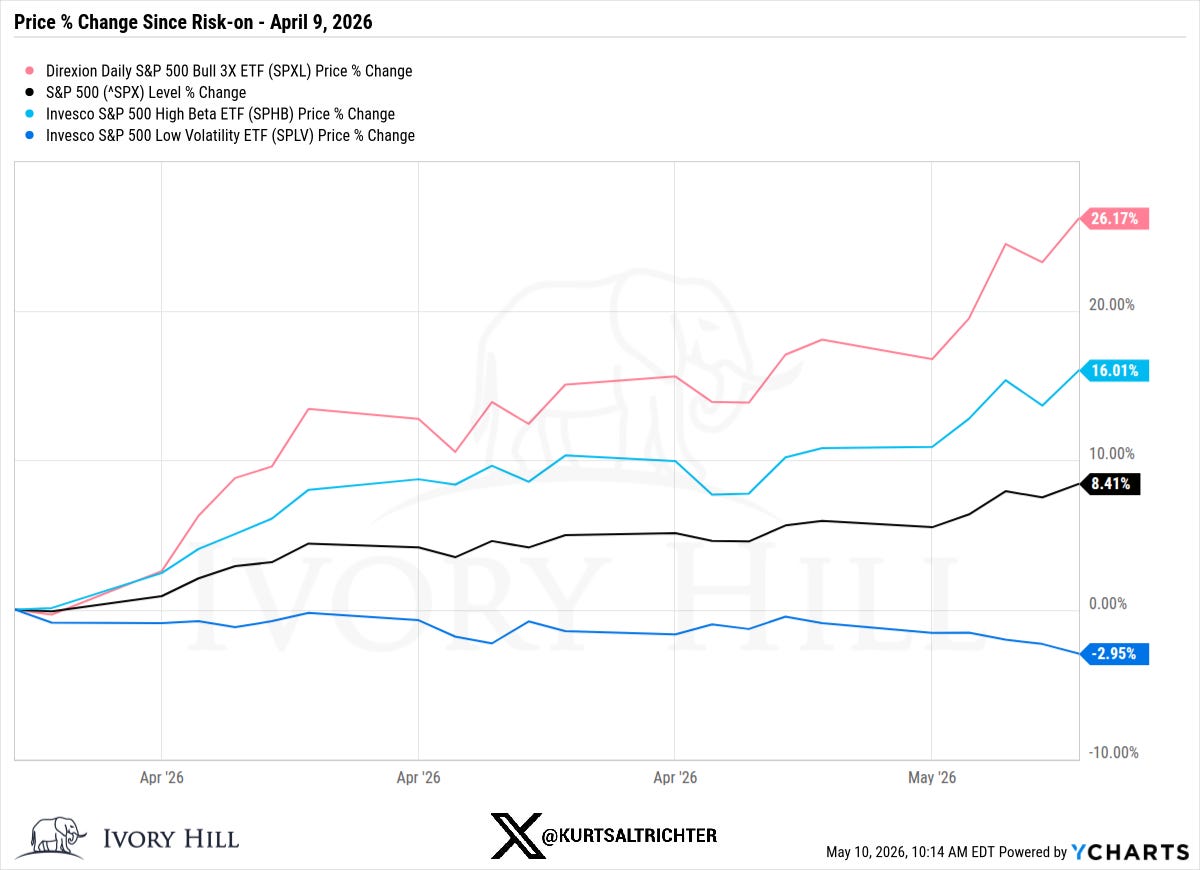

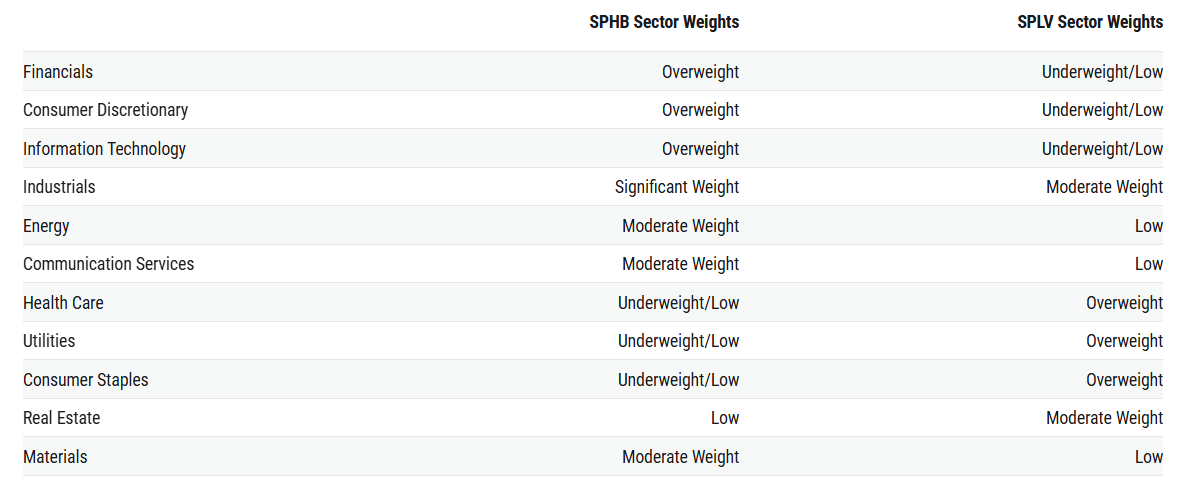

The other reason this model has moved so quickly is that the macro environment has been playing directly in favor of SPHB. Look at the chart. SPLV has actually declined since the signal stack flipped Risk-On. SPHB has fit the macro picture better and outperformed SPLV recently due to a risk-on environment, strength in cyclical and growth stocks, and a broad rotation out of defensive equities.

The macro has not favored low volatility at all. The dominance of AI-related names is evidence. Getting the regime signal right is only part of the work. What you deploy capital into matters more. You can have a perfect signal and still underperform if you are not investing it properly. Even within a universe of index ETFs like SPHB and SPLV, the difference in outcome over a five-week Risk-On streak is nearly 19 percentage points. Same signal, different instrument. If the model had been sitting in a neutral allocation through this period, it would be roughly in line with the S&P 500, not ahead of it like it is today. The position selection has mattered as much as the regime signal itself.

I built this live from Issue 1. I got a few emails from advisors and clients asking about the process, which pushed me to start publishing the report. I wrote the signals into a spreadsheet, expecting to completely overhaul it after the first month. No backtesting. The fact that regime consistency has held gives me confidence to start refining it now.

Two improvements are coming in the weeks ahead.

First, a macro overlay on position selection. The regime tells us how much risk to carry. The macro overlay will tell us which positions most efficiently express that risk. Just because the model is Risk-On does not mean SPHB is always the right expression of that risk.

Second, a front-running signal. Right now, the model matches the market structure. It actually lags by at least a day by design. What the model needs is a dimmer switch, a fifth signal that begins shifting exposure before the regime fully confirms. Stay tuned.

MARKET STRUCTURE: THE ANCHOR POINT

SPX closed Friday at 7,399. The gamma flip is at 7,270. Dealers sit in positive gamma. When dealers are net long gamma, they sell strength and buy weakness. That mechanical behavior suppresses intraday swings and creates the low-volatility, grinding price action we have seen throughout this recovery.

The weekly expected move, defines the trading range for the week of May 11: upside to 7,511 (+1.54%), downside to 7,287 (-1.48%). The -1σ downside level and the gamma flip are sitting nearly on top of each other. A breach of 7,287 on a closing basis would put the market back near the flip and shift dealer hedging dynamics from stabilizing to amplifying. Watch that level.

Dealers are positioned in a way that naturally keeps volatility low and price swings contained. As long as SPX holds above 7,270, that buffer stays intact.

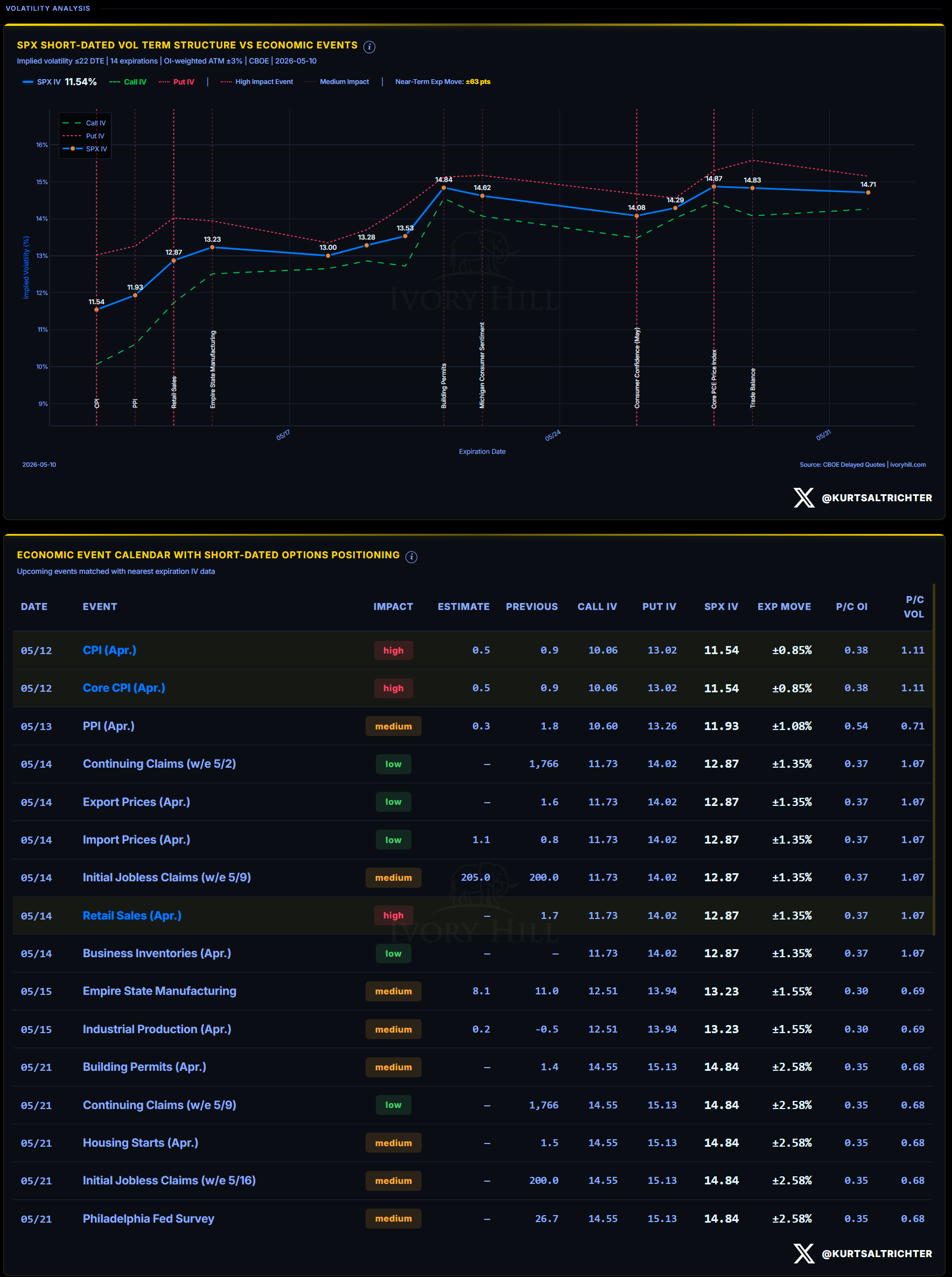

THE ECONOMIC EVENT CALENDAR AND VOL TERM STRUCTURE

Spot SPX IV is 9.97% as of May 10th. The term structure steps up sharply from there. The market is pricing risk into specific event dates rather than distributing it evenly over time.

The key events this week:

Tuesday, May 12, CPI (April) and Core CPI (April): Both carry high-impact classifications. The estimate is 0.5% month-over-month, against a prior reading of 0.9%. The options market is pricing a ±1.05% SPX move for the CPI expiration. Put IV at 13.02 is running notably above call IV at 10.06. The skew tells you the market is paying more for downside protection into this print than upside participation. CPI is the linchpin. A hot number reintroduces the stagflation narrative and pushes vol higher across the curve. A cool number confirms disinflation and gives the bull case room to breathe.

The market consensus has shifted toward a 3.0%-3.5% year-over-year range for April CPI, with the prior consensus of 2.8% largely abandoned after the energy and geopolitical repricing earlier this spring.

The options market is pricing a ±1.05% move on CPI Tuesday. I think that is underpricing the risk.

Our models are putting the headline year-over-year CPI floor at 3.5%, with the high end of the range closer to 3.8%. Base case is approximately 3.65%. The consensus estimate is 3.0% to 3.5%. If our read is right, the market is going to be caught offside.

A hot print at this stage of the rally, after the run we have had off the April lows, is a risk to the narrative. It was one of several factors that prompted us to trim some winners Thursday and Friday (in our core equity models, not the tactical allocation). The cash is positioned for what we think is a very buyable dip, potentially, on the other side of this CPI print.

Wednesday, May 13, PPI (April): Medium impact. The SPX IV for that expiration is 11.93, implying a ±1.25% expected move. Put IV is running above call IV (13.25 vs 10.60), same as CPI the day before. Two consecutive high-impact expirations with the same skew is the options market telling you it is more worried about a downside surprise than excited about an upside one.

Thursday, May 14, Retail Sales (April): High impact. SPX IV steps up to 12.87 at that expiration, implying ±1.51%. Retail sales measures consumer spending directly. Weak spending means slower growth expectations, the Fed has room to cut, and bonds and equities potentially rally. Strong spending means the consumer is holding up, less urgency to cut rates, and higher-for-longer risk remains. The chain reaction runs through rate expectations, dollar direction, and risk appetite simultaneously.

Options traders are pricing more risk into this week’s economic calendar than current spot vol suggests. CPI on Tuesday is the market-structure event of the week.

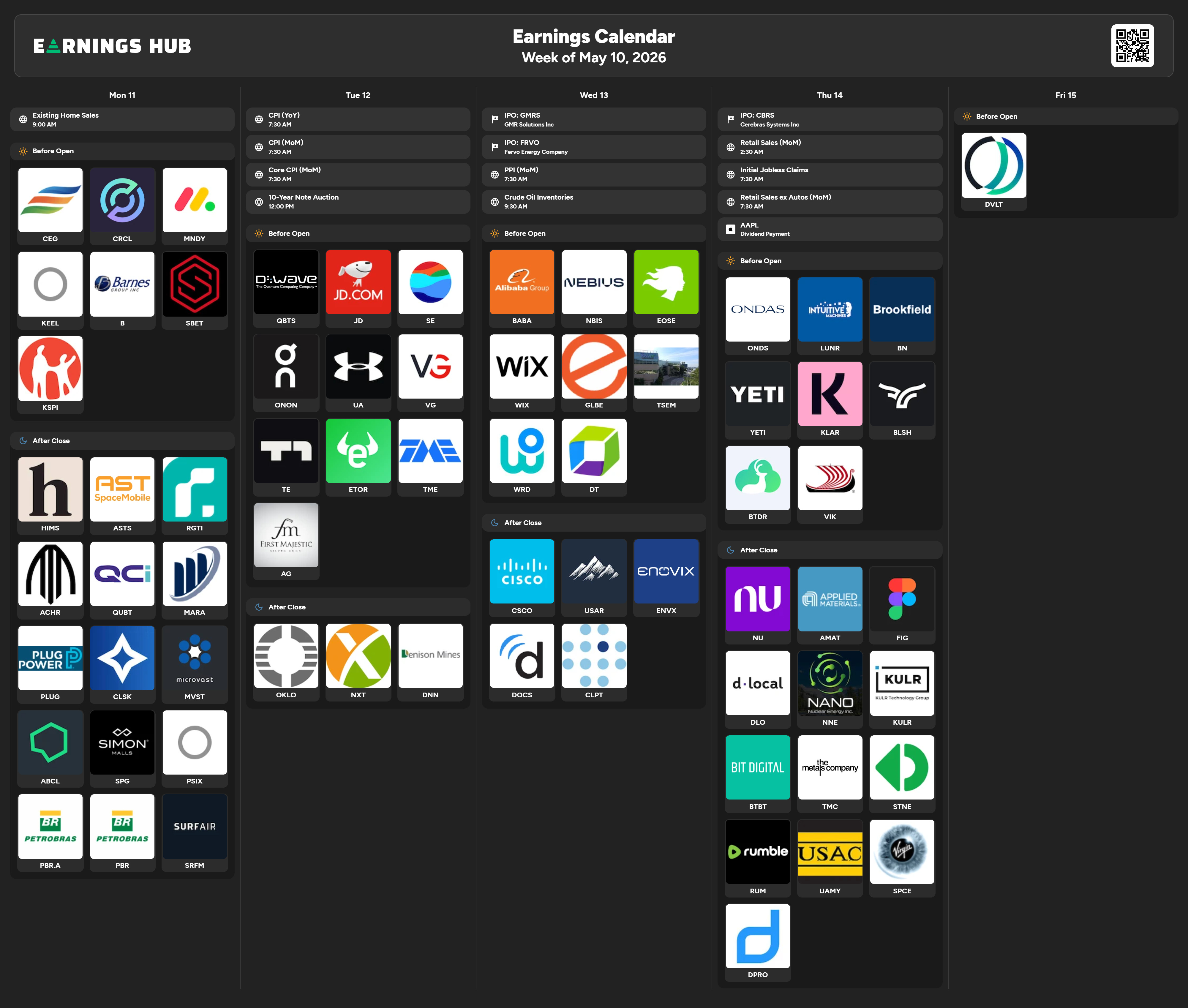

EARNINGS: WEEK OF MAY 11

The earnings calendar is active this week. Key names by day:

Monday, May 11: Lighter slate. HIMS, ASTS, ACHR, MARA after the close. SPG and ABCL also report. Existing Home Sales at 9:00 AM.

Tuesday, May 12: CPI day dominates the macro tape. Pre-market earnings include QBTS (D-Wave Quantum), JD.com, Under Armour (UA), and TME. After the close: OKLO, NXT, DNN.

Wednesday, May 13: PPI in the morning. Before the open: Alibaba (BABA), WIX, and GLBE. After the close: Cisco (CSCO). Cisco is the notable one. A large-cap bellwether with enterprise IT spending exposure that matters for the XLK narrative heading into the back half of the week.

Thursday, May 14: Retail Sales, Initial Jobless Claims, and Import/Export Prices all drop before the open at 7:30 AM. Earnings before the open include Intuitive Machines (LUNR), YETI, Brookfield (BN), and BTDR. After the close: Applied Materials (AMAT). AMAT reports semiconductor equipment demand. Given the XLK leadership this week, the AMAT print is a late-session risk event with the potential to move the sector Friday morning.

Friday, May 15: Light on earnings. DVLT before the open.

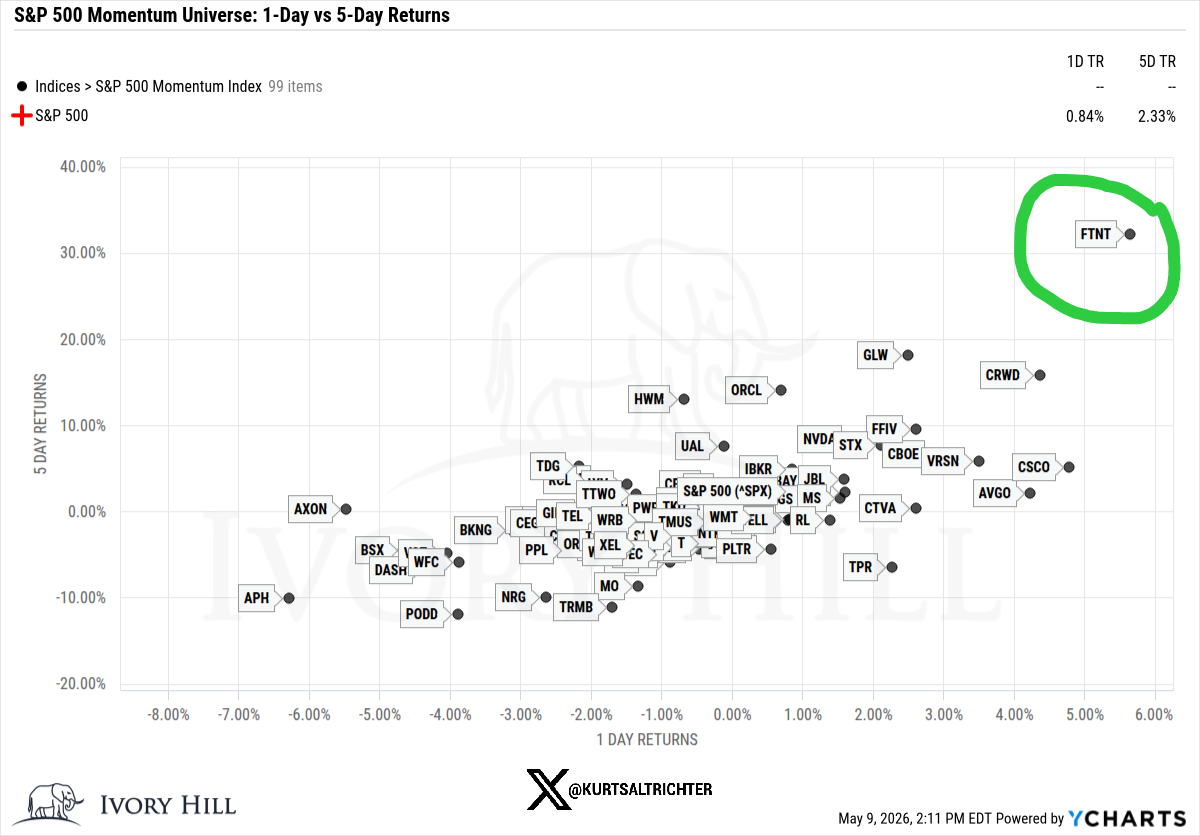

MOMENTUM PULSE CHECK

The momentum universe shows a well-dispersed field with a clear leadership cluster. FTNT led the 5-day return at +32%, followed by GLW and CRWD. The technology and cybersecurity names are dominating the right side of the chart. CSCO and AVGO also showed strong 5-day momentum with solid 1-day follow-through. On the weak side, APH, PODD, and AXON lagged on both timeframes.

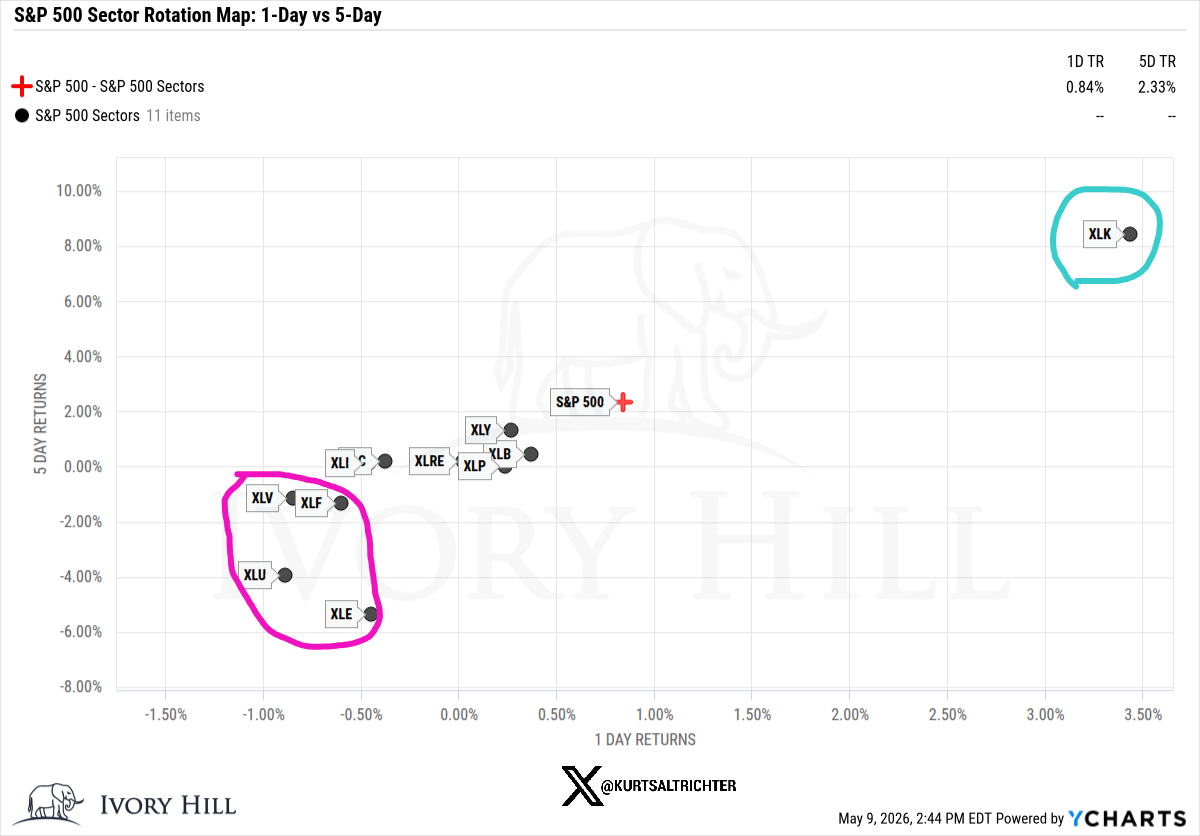

The sector rotation map tells the same story at the macro level. XLK (Technology) is the clear outlier, up roughly 8.3% on a 5-day basis and adding another 3.5% on Friday alone. Every other sector sits in a tighter cluster near flat to slightly negative on the 5-day window. The S&P 500 itself printed +0.84% Friday and +2.33% on the week. Notably, defensives like healthcare, financials, and utilities are lagging on the week.

The breadth of sector participation is getting narrower. Technology is doing the work. That is a concentration risk worth monitoring. If XLK pauses or pulls back, the market will drop.

VOLATILITY REGIME

The 1-month realized vol printed 10.61. The 3-month is 14.76. Short-dated vol has collapsed faster than the longer window can catch up, which is what you see after a sharp dislocation event transitions into a trending low-vol recovery. The regime tag is LOW-VOL.

Vol-control funds care about this directly. Their equity allocation formula is driven by realized vol. When RV is low, the formula pushes them toward higher equity exposure. When RV rises, they de-risk mechanically. At 10.61 on the 1-month, the math is pointing them toward maximum allocation territory. That is a structural tailwind for equities until the vol regime shifts.

SYSTEMATIC FUND FLOWS

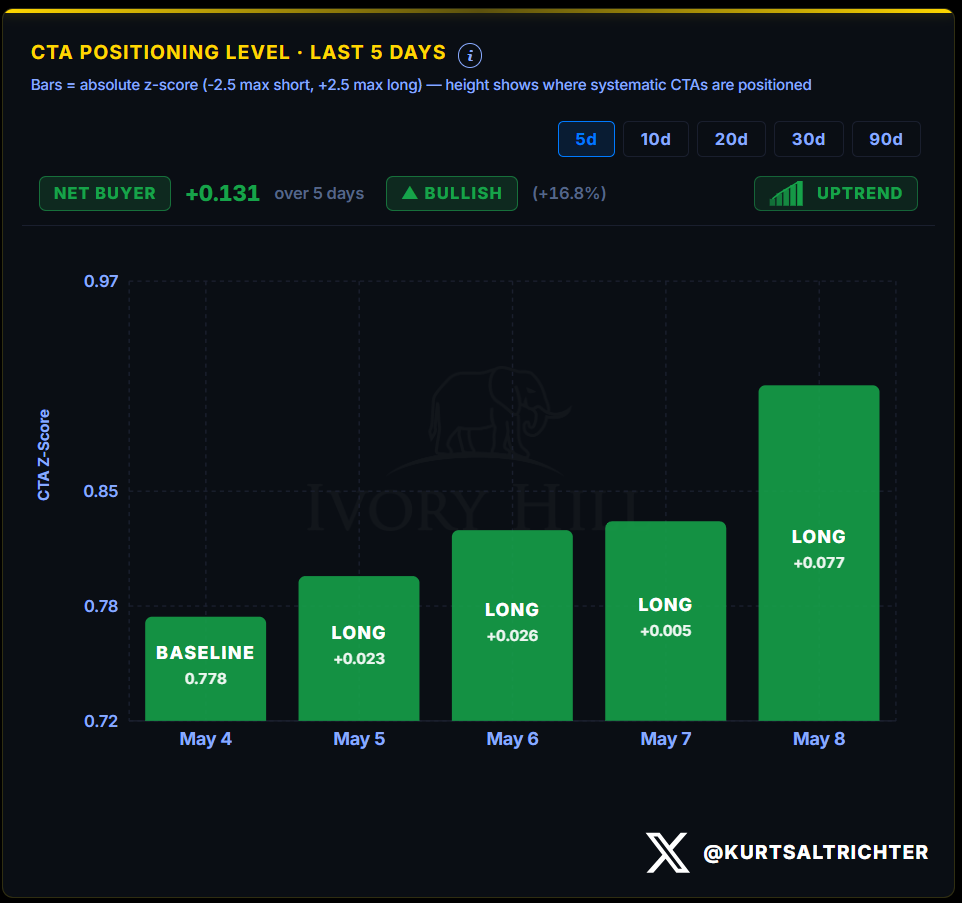

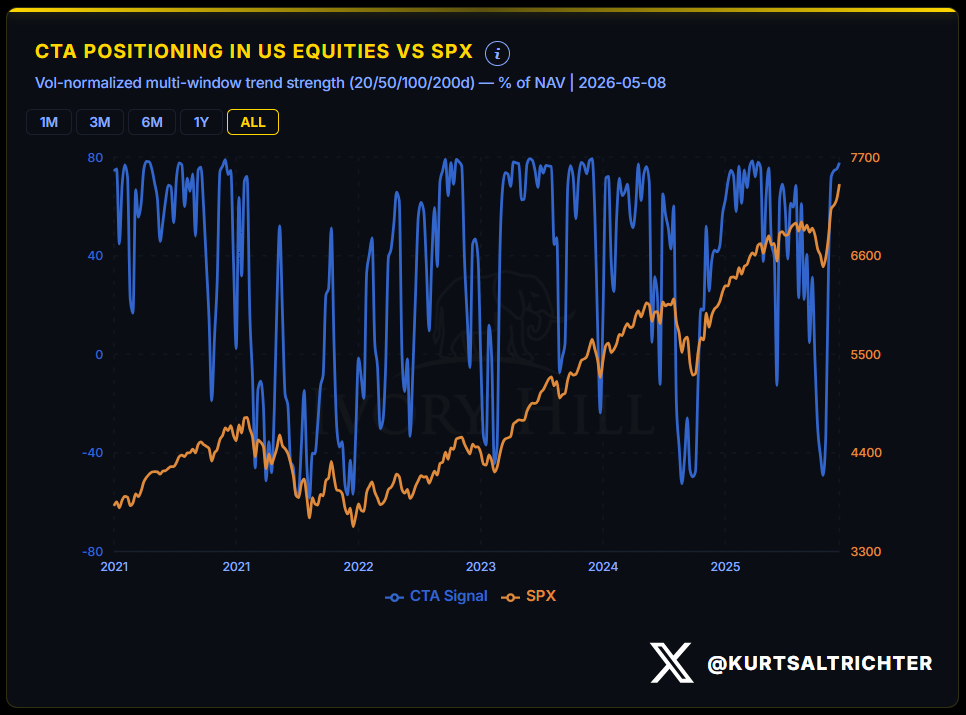

CTA Positioning

CTAs were net buyers over the past five days, adding +0.131 to their z-score. The baseline on May 4 was 0.778. By May 8, the score had climbed to approximately 0.909, with the largest single-day addition coming Friday (+0.077). The trend is classified as Bullish and Uptrend.

The longer-term picture confirms the shift. CTAs went from deeply negative positioning in late March and early April, levels not seen since the 2022 bear market, to aggressively rebuilding long exposure. The speed of that rotation, paired with a rising SPX, is the textbook pattern for a systematic-driven momentum rally. CTAs are not chasing reluctantly. They are adding what little cash they have left into strength.

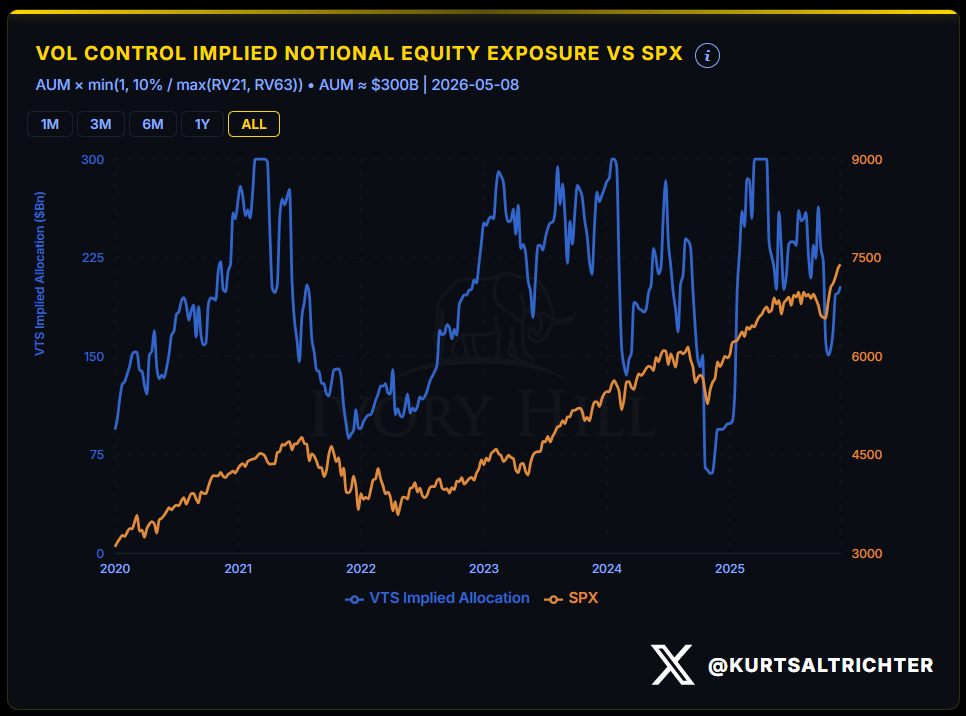

Vol-Control Positioning

Vol-control funds were net buyers of $4.9 billion over the past five days. The week was not linear. May 6 saw a $3.1 billion sell. May 7 followed with a $2.3 billion buy. May 8 posted the largest single-day addition at $5.6 billion. The net result is an allocation level near $204 billion against the estimated $300 billion AUM cap, roughly 68% of cash has been deployed.

The longer view shows that vol-control exposure remains well below peak levels seen in 2021 and again in early 2024. There is structural room to add if volatility continues to fall. That dry powder is a latent tailwind.

Systematic Positioning Index

The combined CTA + vol-control z-score sits between +1σ (Bullish) and +2σ (Extreme Long) on the 20-day rolling basis. The index bottomed near -3σ (Capitulation) around April 1, which aligned almost exactly with the S&P 500’s intraday low during that period. The subsequent rebound in systematic positioning has tracked the SPX recovery step for step. We are not at crowded extremes anymore, but we are approaching the zone where incremental buying pressure from this cohort begins to slow.

MARKET BREADTH

55% of S&P 500 members trade above their 200-day moving average. The signal reads Neutral. The 60% threshold is the dividing line between neutral and optimism. The 40% line is pessimism.

We were well below 40% at the April lows. A recovery from deep pessimism to the neutral zone in five weeks is meaningful. But 55% also means that 45% of the index has not yet reclaimed its long-term trend line. The breadth recovery is not yet complete. All the soldiers need to march with the generals.

The composite signal remains Neutral on breadth, which is why the weighted composite scores Neutral even as three of four inputs (gamma, RV, flows) score Bullish. The regime stays Risk-On because the composite framework allows it, but breadth is the variable to watch as the week progresses.

DEALER GAMMA DASHBOARD

Tactical Allocation: 75% SPHB / 25% SPXL

Three of four inputs are Bullish. Breadth is the lone Neutral. The weighted composite lands Neutral, but the regime framework reads Risk-On. This is the fifth consecutive week at Risk-On. The allocation remains unchanged.

The conditions that would shift the regime: a sustained breadth deterioration back below 40%, a vol spike that breaks the 1-month RV above the 3-month, a gamma flip breach on a closing basis, or systematic fund flows reversing to net selling. None of those are present today.

Watch CPI Tuesday. The rest follows from there.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Follow me on X for more updates.

Best regards,

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Wealth Advisor | President

Disclosure

The Gamma Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hill, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.

Information Technology is doing the heavy lifting here, up 8.3% in five days, and the TAA consensus fully supports that leadership: 64.3% of managers are overweight IT (ranked 2nd, stable trend), with only 14.3% underweight. The regime signal is clean, but the breadth gap is the structural tension worth naming.

Only 55% of S&P 500 members trade above their 200-day moving average, while IT carries roughly a quarter of global market cap.

Invesco, Asset Allocation Award winner 2026, flags this directly: "there is a rotating selection of a handful of sectors pushing the market higher each quarter," with technology valuations remaining the second most expensive in their model.

A hot CPI print Tuesday that reprices Fed expectations would hit high-multiple growth names hardest, precisely where this rally is most concentrated. Is the gamma cushion thick enough to absorb that scenario without a breadth breakdown?