GDP is an Unreliable Indicator

Unraveling the True Drivers of Economic Growth - A Comparative Analysis

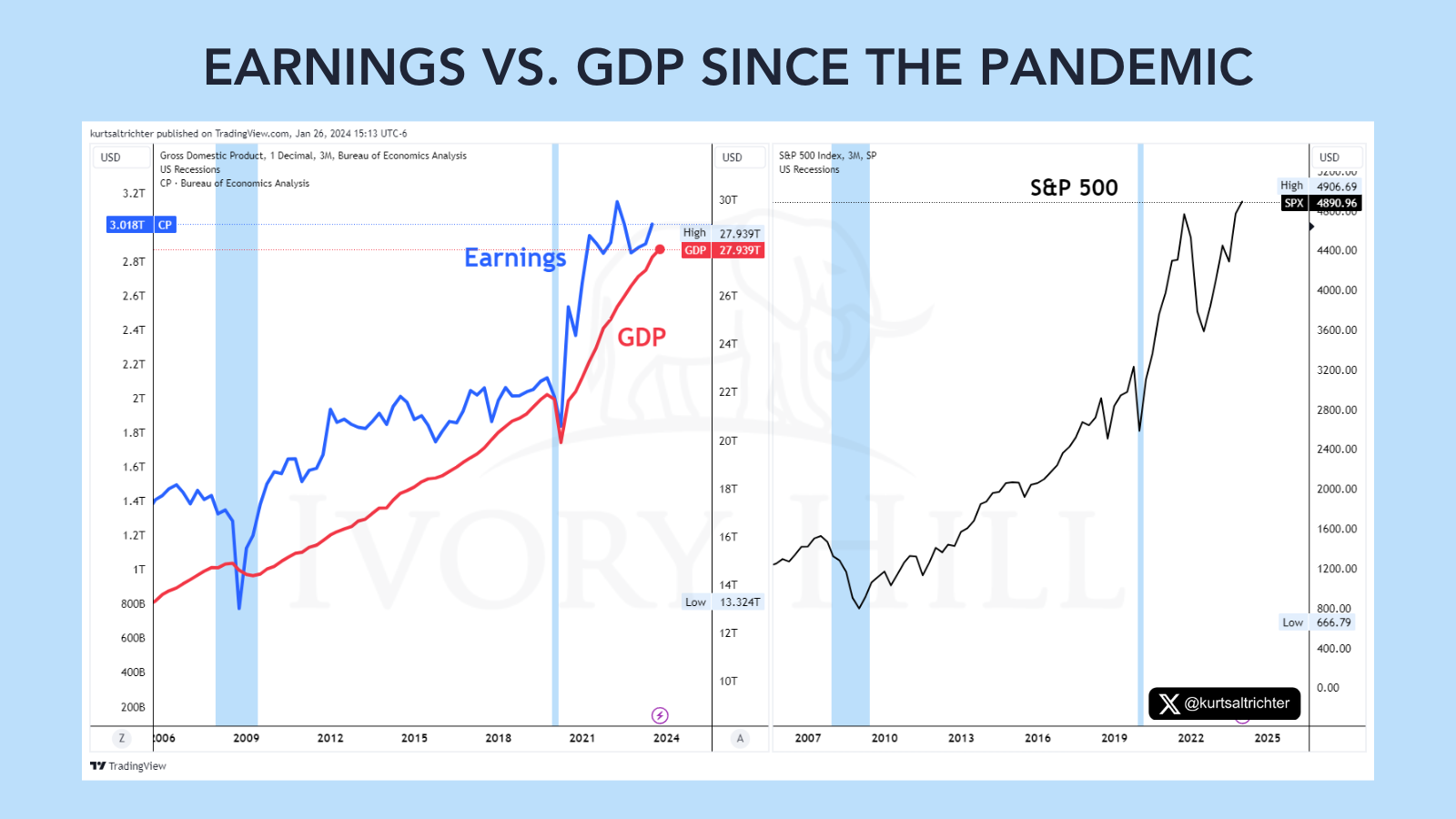

When assessing the health of the U.S. economy the debate often centers around two key indicators: earnings and GDP (Gross Domestic Product). While the consensus generally favors GDP, I firmly believe this perspective needs a much closer examination, especially in light of last week’s report showing Q4 GDP printed a strong number of 3.3%.

The talking heads on CNBC immediately graced us with their “profound” insight, declaring that this number is a surefire sign of the almighty economic strength of the United States.

Although GDP is useful for tracking total economic activity in the U.S., it provides zero insight into future economic trends.

GDP is unreliable.

The limitations of GDP as a reliable indicator are twofold. Firstly, it's important to understand that inputs like inventory levels and trade balance can influence GDP numbers. An increase in inventories can artificially inflate GDP numbers, but this doesn't necessarily equate to real economic growth. Similarly, trade balance, which includes imports and exports, can significantly impact GDP. However, these inputs can give misleading signals about the actual state of economic growth. For instance, a surge in imports might suggest a reduction in GDP, but it could also indicate strong domestic demand. Interpreting GDP data requires caution to avoid misunderstandings about the state of the economy.

Earnings are more precise.

On the other hand, earnings offer a more precise and telling insight into economic growth, and here's why: earnings provide a linear and direct reflection of financial health. Consider this scenario: if a wide range of companies across different industries report a strong start in October but a decline by December, it's a clear red flag for the economy.

On the flip side, reporting weaker numbers at the beginning of a quarter followed by a strong finish is a positive sign for the economy. This exact scenario unfolded in the Q2 ’23 earnings season. Companies started the quarter softer but gained momentum towards the end, indicating an upswing in economic activity. This progression led to an upward acceleration in stock prices.

What are earnings saying about growth now?

We're still in the early stages of the earnings season, and it's crucial not to jump to conclusions. However, the initial data from non-tech earnings give a clear message: growth is present but is losing momentum.

The banking sector's insights on consumer spending, especially charge-offs and delinquency rates, are revealing. Synchrony Financial, which primarily deals with consumer loans, has seen a significant increase in late payments.

This trend is not limited to a particular industry; it is also present in many big consumer and industrial companies, such as 3M. These observations in various sectors strengthen the idea that although the economy is growing, there are more and more signs of caution in consumer financial behavior.

While earnings season is far from over, the early reporting from non-tech corporate sectors reinforces what the broader economic data signals: growth is there, but it's moderating. This starkly contrasts the overly optimistic narrative spun by the media following Thursday’s GDP report.

Only time will tell.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President