Global Rebalancing Away From the United States

From concentration risk to capital rotation in a changing regime

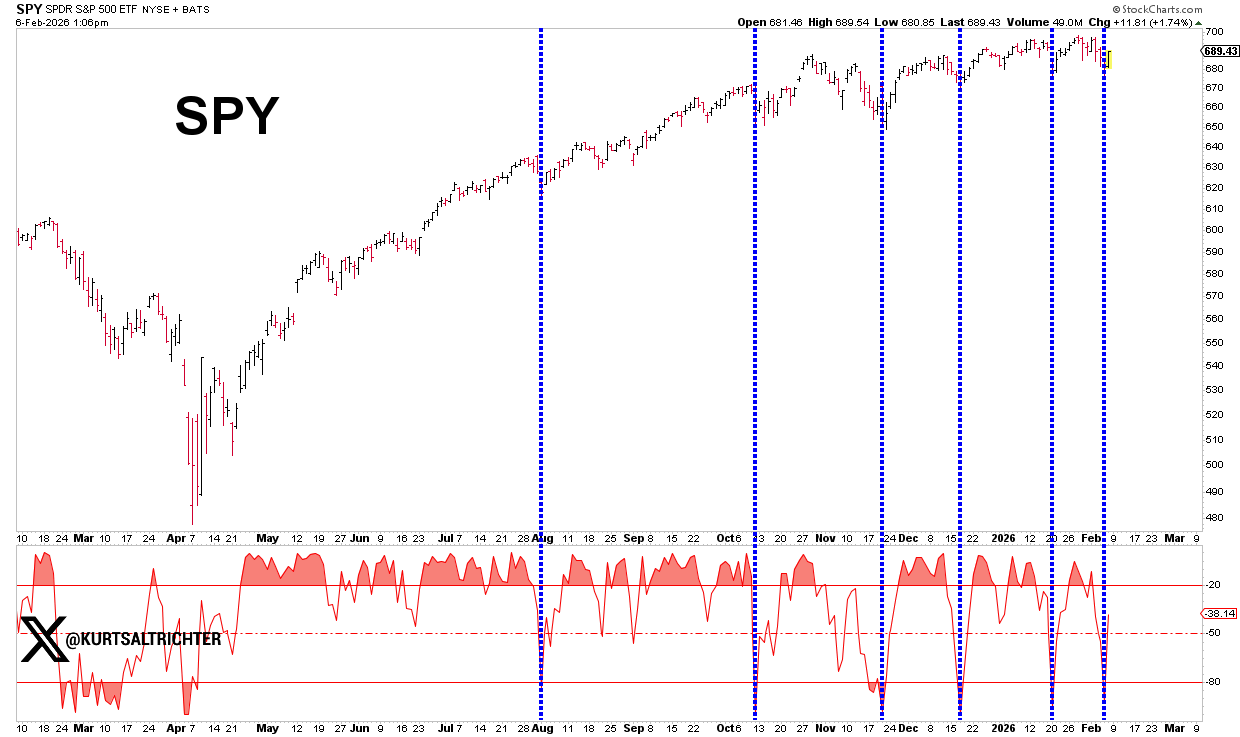

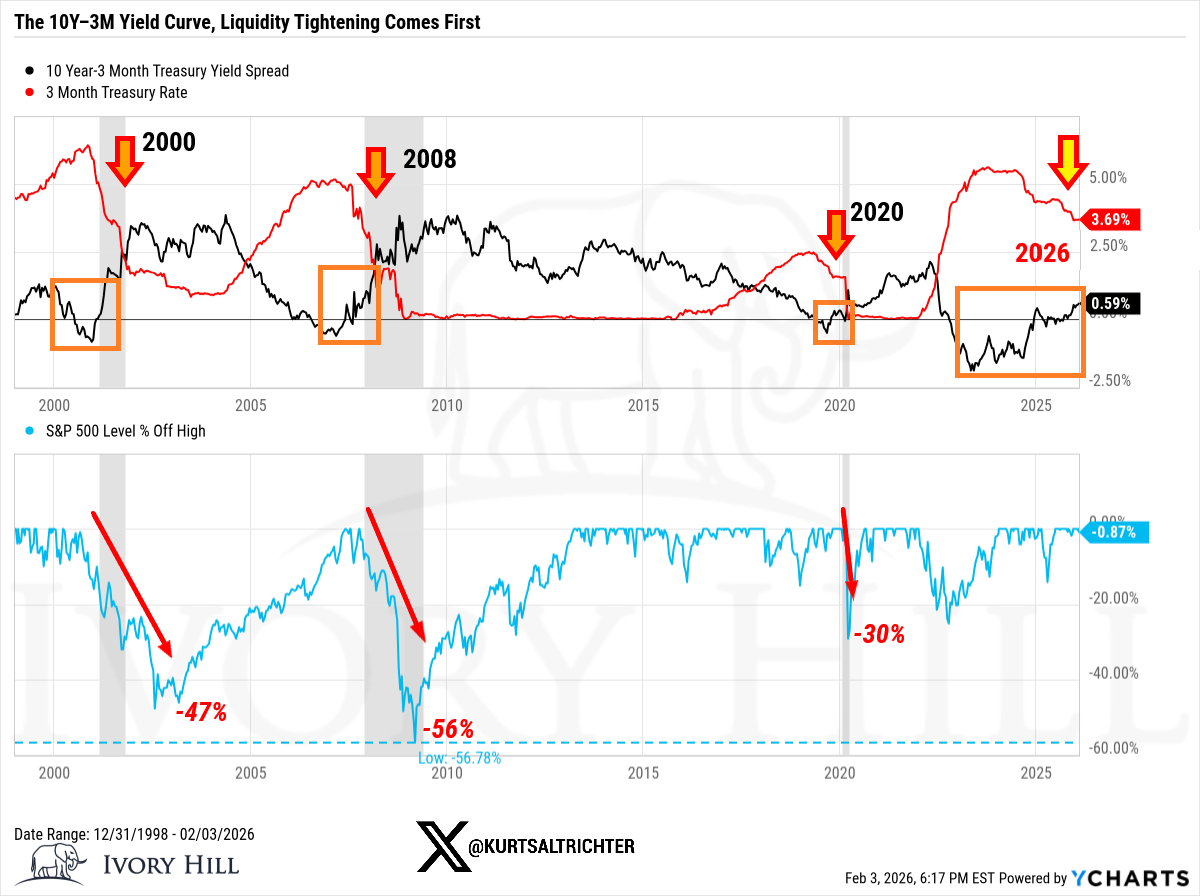

The Ivory Hill RiskSIGNAL™ remains green. Pullbacks are getting absorbed quickly because buyers keep stepping in at the same structural levels, confirming demand is still in control where it matters.

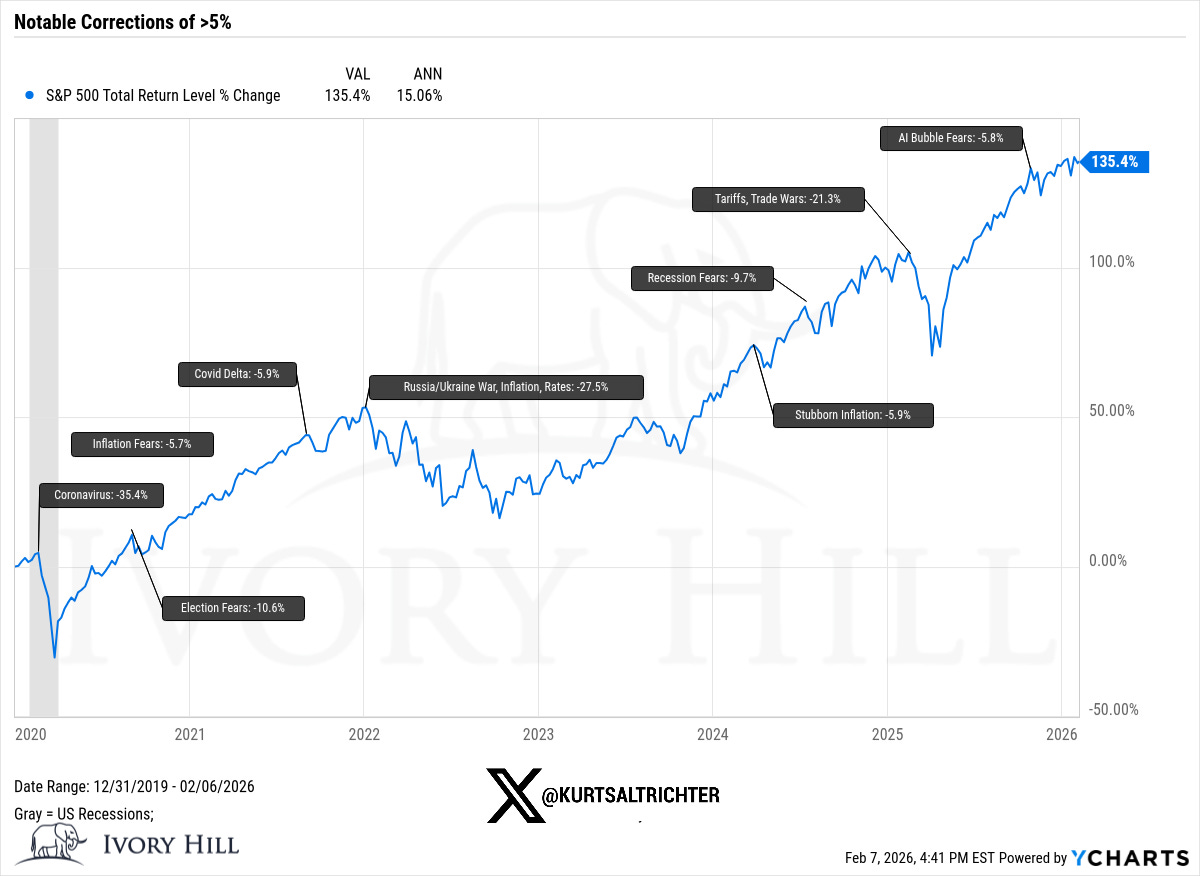

Markets are doing what they always do late cycle. They stop rewarding consensus and start punishing concentration. The market does not care how good last year felt. It only cares where money is rotating next.

Why Capital Is Rotating Away From the U.S.

Since the Global Financial Crisis, U.S. equities delivered returns far faster than the real economy. Stocks compounded at multiples of GDP growth, and markets were rewarded for ignoring economic gravity.

Over that period, the entire planet invested large amounts of capital in US markets.

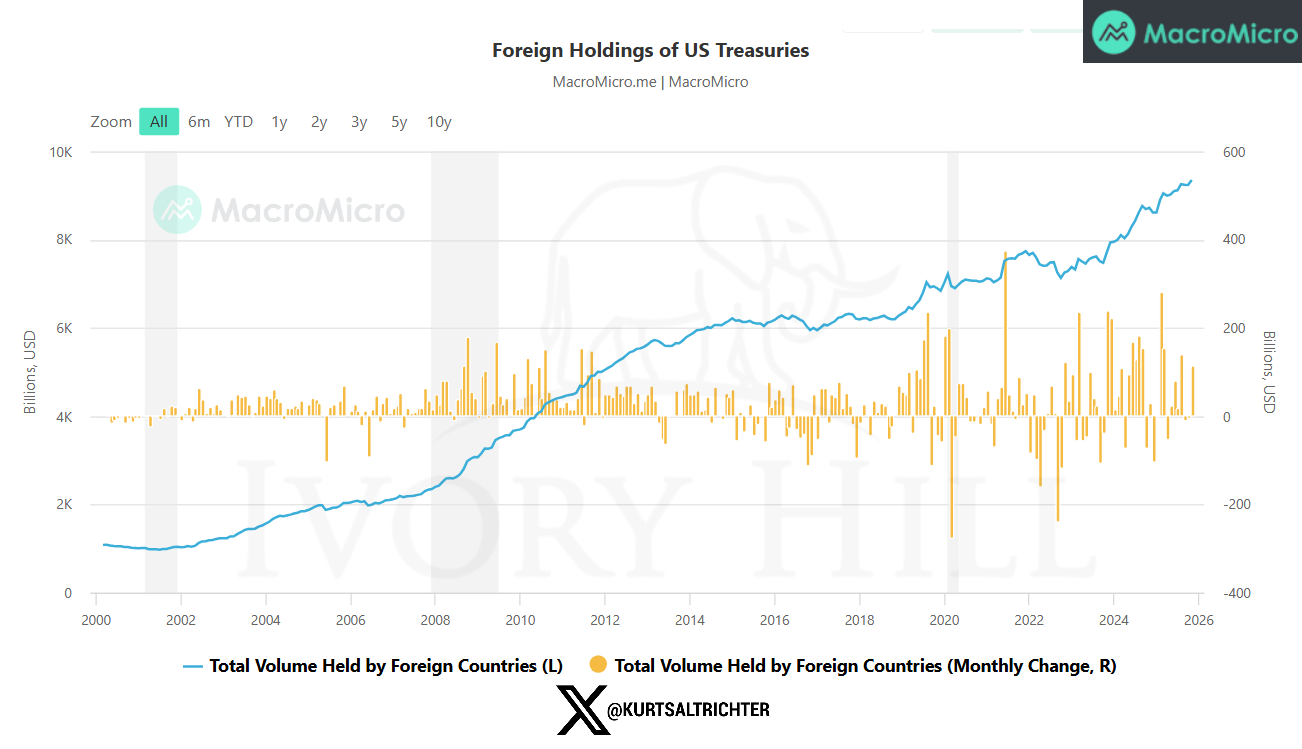

Foreign investors more than tripled their exposure to U.S. stocks over the past decade, pushing total US holdings above $20 trillion, mostly unhedged. As capital flowed in, valuations rose. As valuations rose, the dollar strengthened. A stronger dollar amplified returns for foreign investors. The cycle fed on itself.

That regime depended on a very specific set of tailwinds.

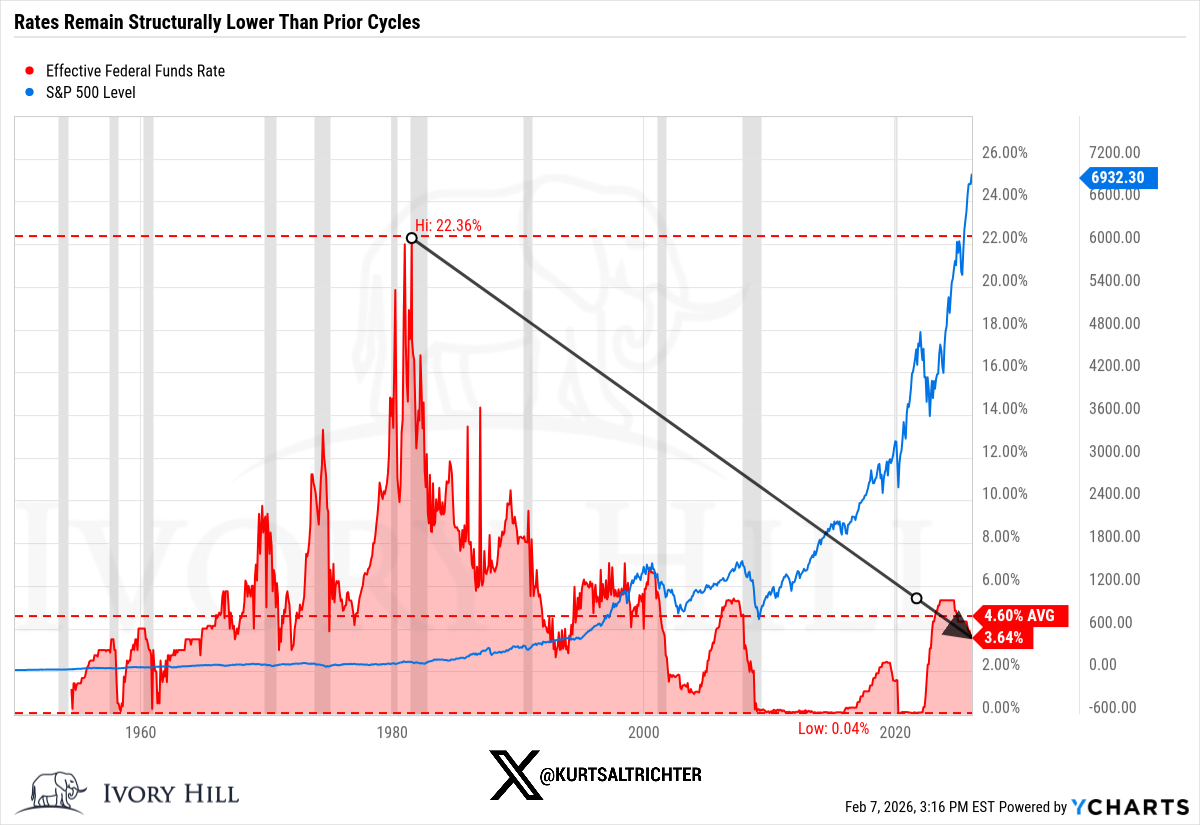

First, interest rates trended lower for nearly 40 years. Rates are expected to keep coming down from here, but they remain well above where they were a decade ago. The long, steady decline that boosted valuations is over. Lower future rates are not the same tailwind as falling rates from much higher levels.

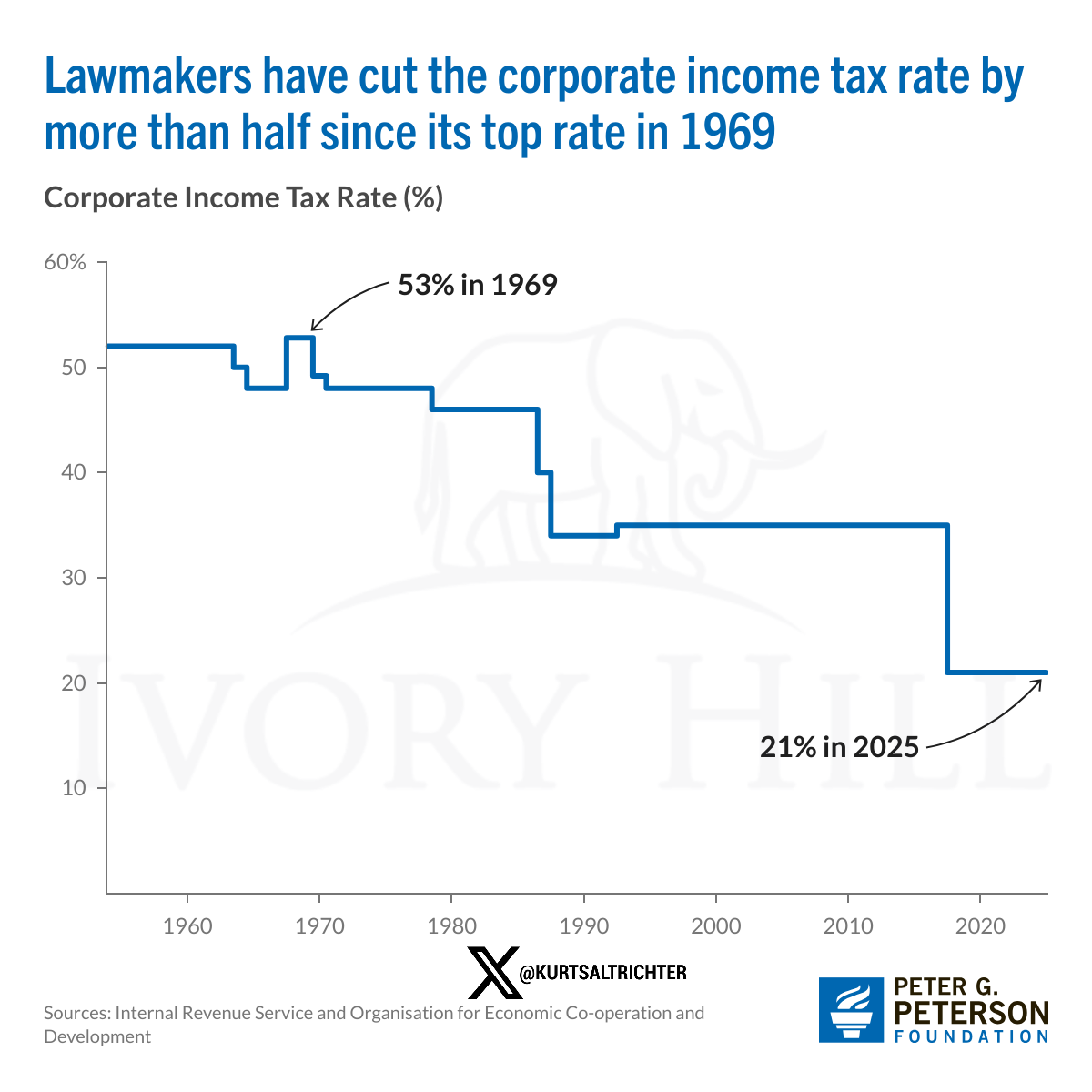

Second, corporate tax cuts materially boosted after-tax profits. That was a one-time reset. Those gains are now fully reflected in earnings and valuations.

Third, central banks flooded markets with liquidity after the financial crisis. By buying massive amounts of bonds, they pushed yields down and forced investors into stocks and other risk assets. That drove asset prices higher even without equivalent economic growth. That process has slowed materially and, in some cases, reversed.

Fourth, corporate profits captured a larger share of the economy than wages. Companies benefited from globalization, automation, and cost control, which lifted margins. That shift raised earnings for years, but it is no longer accelerating the way it once did.

Lower interest rates and lower corporate taxes alone accounted for nearly half of U.S. profit growth over the past 30 years. This explains most of the rise in US valuation multiples.

Those tailwinds are now fading.

Rates may decline modestly, but they are not collapsing. Liquidity is no longer expanding the way it did in the 2010s. Rates are coming down, and tax cuts already happened, but neither provides the same lift they once did, meaning profits will rely more on real growth than on financial tailwinds.

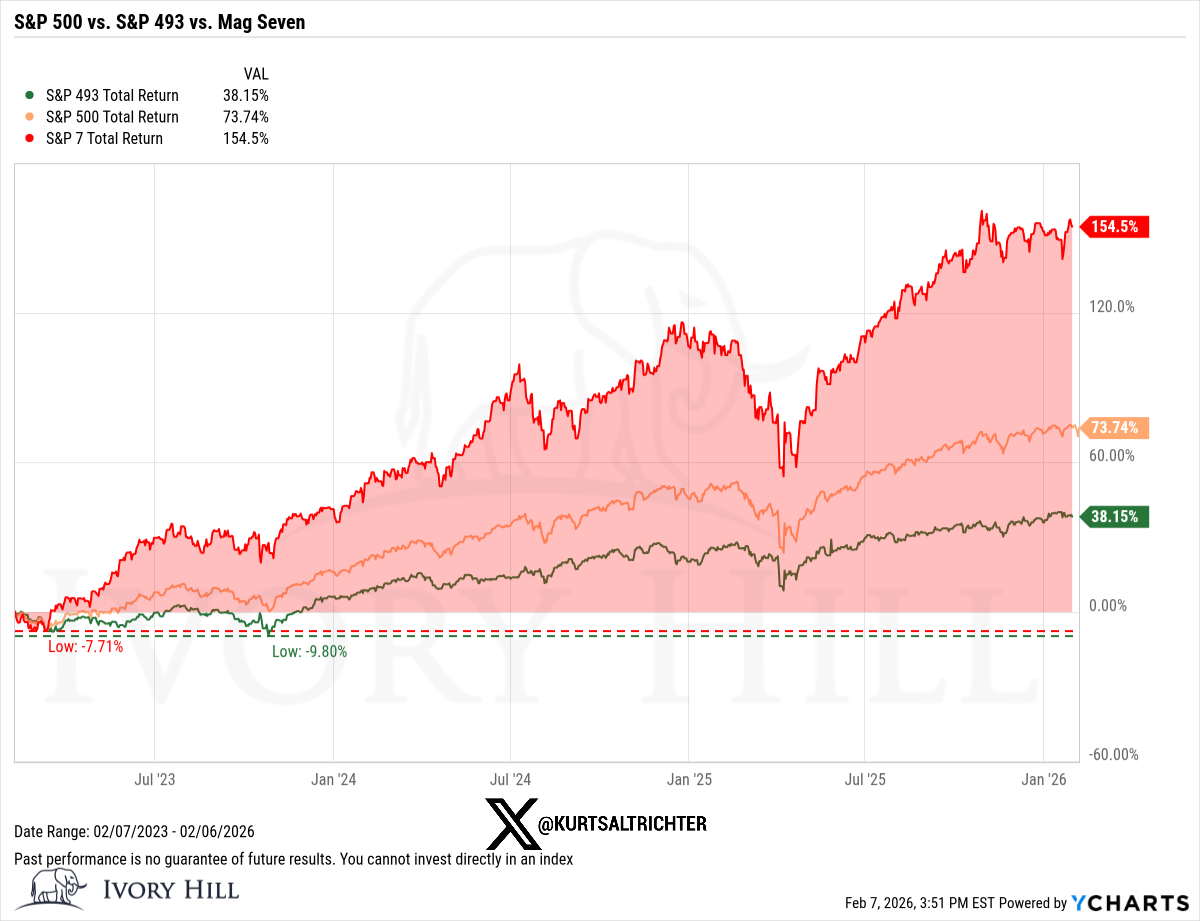

At the same time, risk has become highly concentrated. Roughly 55% of S&P 500 returns over the last three years came from just seven stocks. The top ten now make up about 40% of the index.

The currency tailwind has also reversed. A 10% decline in the U.S. dollar means foreign investors now earn fewer returns when U.S. assets are converted back into their home currencies, reducing the appeal of adding new U.S. exposure. In other words, a weaker dollar now subtracts from foreign investors’ returns, turning what was once a powerful performance boost into a reason to look elsewhere.

Because much of this foreign exposure is unhedged, a weaker dollar reduces returns or forces investors to hedge currency risk, neither of which supports additional investment in U.S. assets.

As expected returns fall and concentration risk rises, making a change becomes more rational, especially for fiduciaries focused on risk-adjusted outcomes.

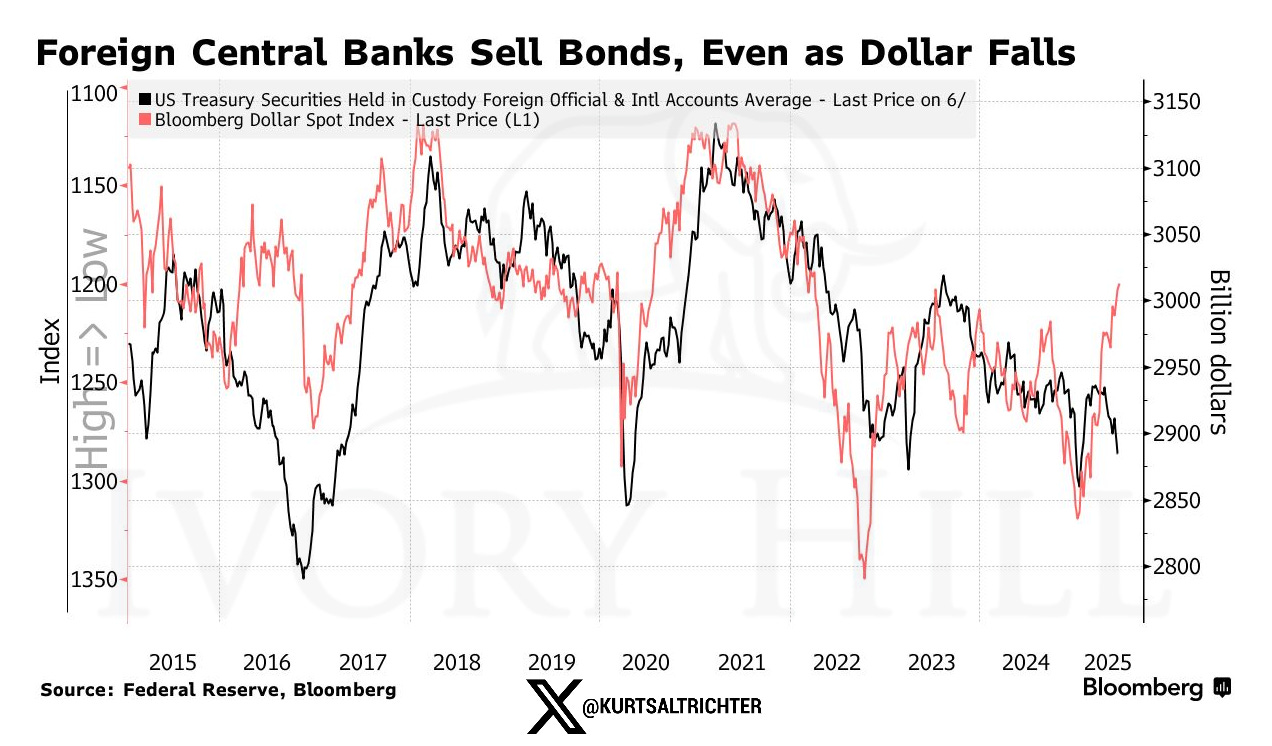

Even Treasuries are being questioned by the rest of the world. Central banks have been net sellers over the past year, which is unusual given a weaker dollar. Rising U.S. debt levels, repeated government shutdowns, and growing scrutiny of institutional independence have added a policy risk premium that simply did not exist in prior cycles.

Central banks are reducing Treasury holdings to diversify reserves and increase gold exposure. They are responding to rising U.S. deficits and policy risk, not short-term market moves. Demand would return only if fiscal discipline improved and Treasuries again offered a clear long-term advantage over gold as a reserve asset.

Before the emails start rolling in, I’m not saying U.S. markets are broken. I’m not even bearish on U.S. stocks. I’m acknowledging that the conditions that powered U.S. dominance for more than a decade are now giving foreign investors a reason to look elsewhere, and they are. That matters because foreign investors own roughly 20% of the U.S. equity market, about $20 trillion, and roughly 33% of the U.S. Treasury market. I’m not arguing that this capital disappears overnight, but it doesn’t have to. Even a small reallocation is enough to drive the rotations we’re seeing now.

That isn’t a problem for us, because our strategies are not constrained by geography or by Old Wall Street asset-allocation frameworks that have failed investors for years.

That is why, since the first trading day of the year, our core equity model has maintained the lowest exposure to U.S. stocks in five years.

Not because the U.S. is failing. I do not see a recession.

But because the math has changed, the cycle has shifted, and the risk profile looks different (worse) from what it did for most of the last decade. Concentration risk is elevated and has been for a while, correlations are unstable, and the opportunity set outside the U.S. is simply better right now.

We’re getting closer to the point where the big macro picture actually matters, and when it does, ignoring it becomes the bigger risk.

Let’s dive into what we have owned since the start of the year.

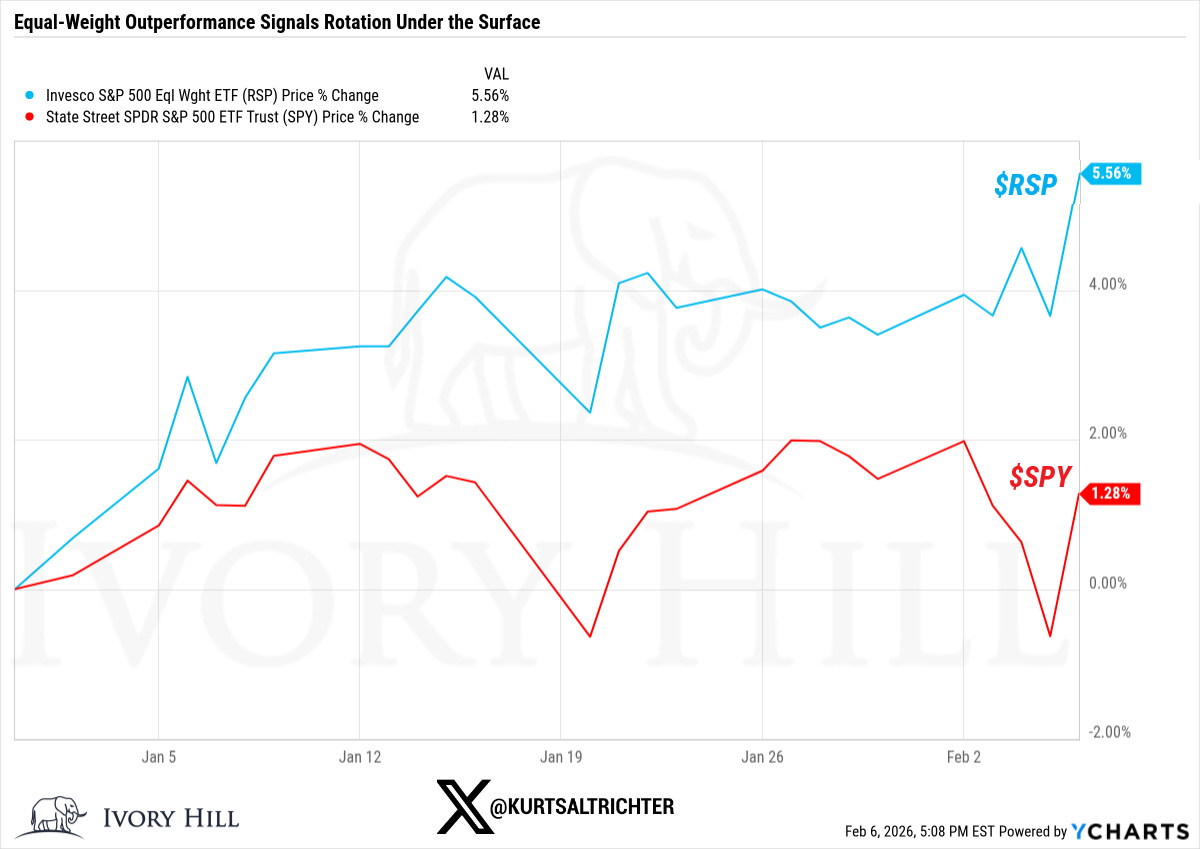

RSP Over SPY

When leadership narrows, cap-weighted benchmarks stop telling the full story. They look healthy right up until the moment they don’t.

That is exactly why, since the start of the year, we are long equal-weight U.S. exposure over cap-weighted exposure. Equal weight captures what is actually happening beneath the surface, not what a handful of mega-cap names want you to believe. Leadership is broadening, and mega-cap dominance is no longer doing the heavy lifting.

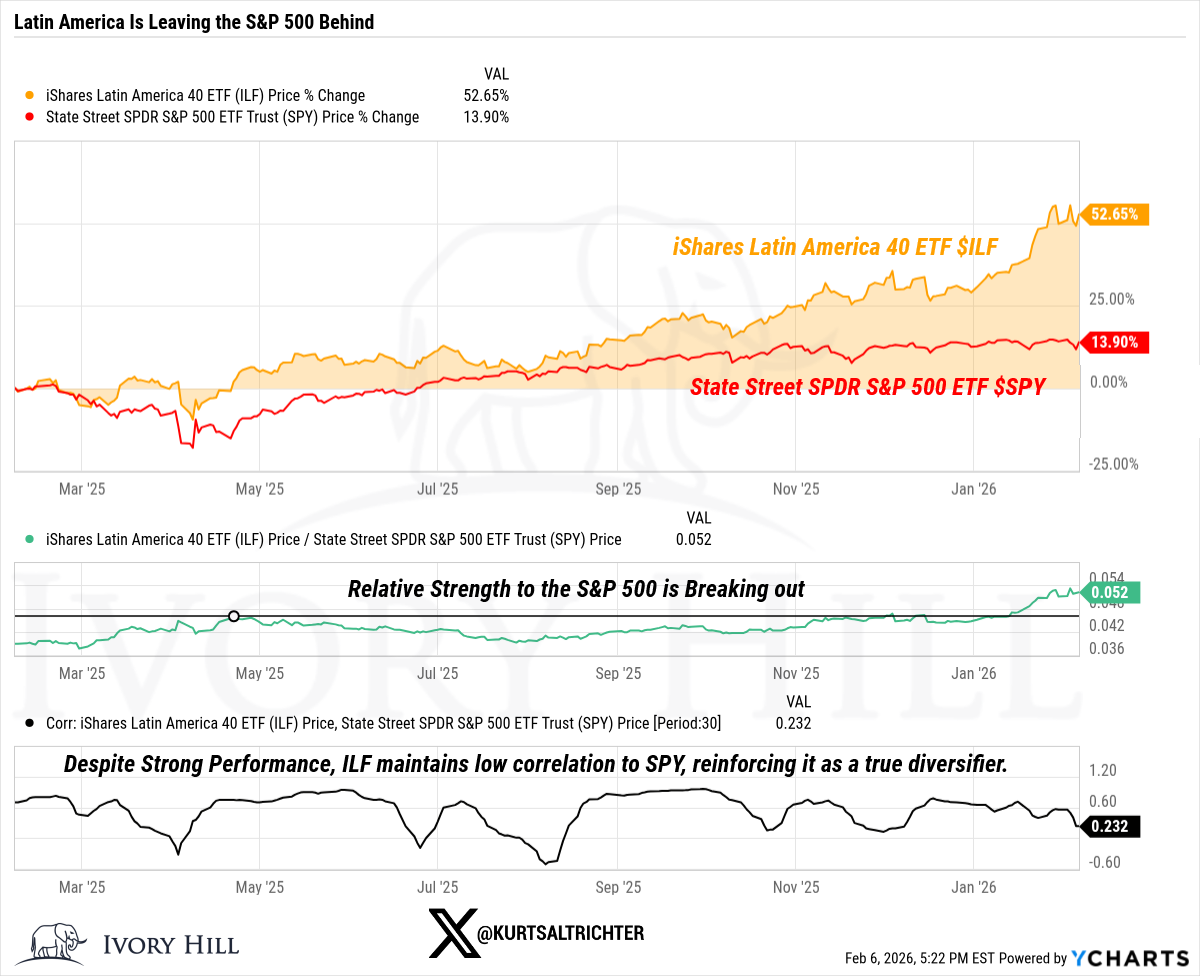

Latin America

We remain long Latin American equities via ILF because macro, geopolitical, and market-structure signals all point to the same conclusion. The region is up roughly +19% YTD and more than +50% over the last year, decisively outperforming the S&P 500. That outperformance is not coming with higher correlation. Relative strength versus U.S. equities is breaking out while correlation to SPY remains low, confirming this as true diversification, not leveraged beta.

Fundamentally, Latin America is benefiting from improving terms of trade, direct commodity and metals leverage across Brazil, Chile, and Peru, and meaningful distance from U.S. political and policy noise. On the geopolitical front, the January removal of Nicolás Maduro in Venezuela eliminated a long-standing regional risk premium that had suppressed capital flows for years, while the finalized EU–Mercosur trade agreement materially improves export access for Brazil and Argentina. Growth north of 4%, still-reasonable valuations, and accelerating capital inflows have turned what began as a commodity-led trade into a structurally bullish regional regime.

When investors want growth without U.S. concentration risk, this is one of the areas you want to consider.

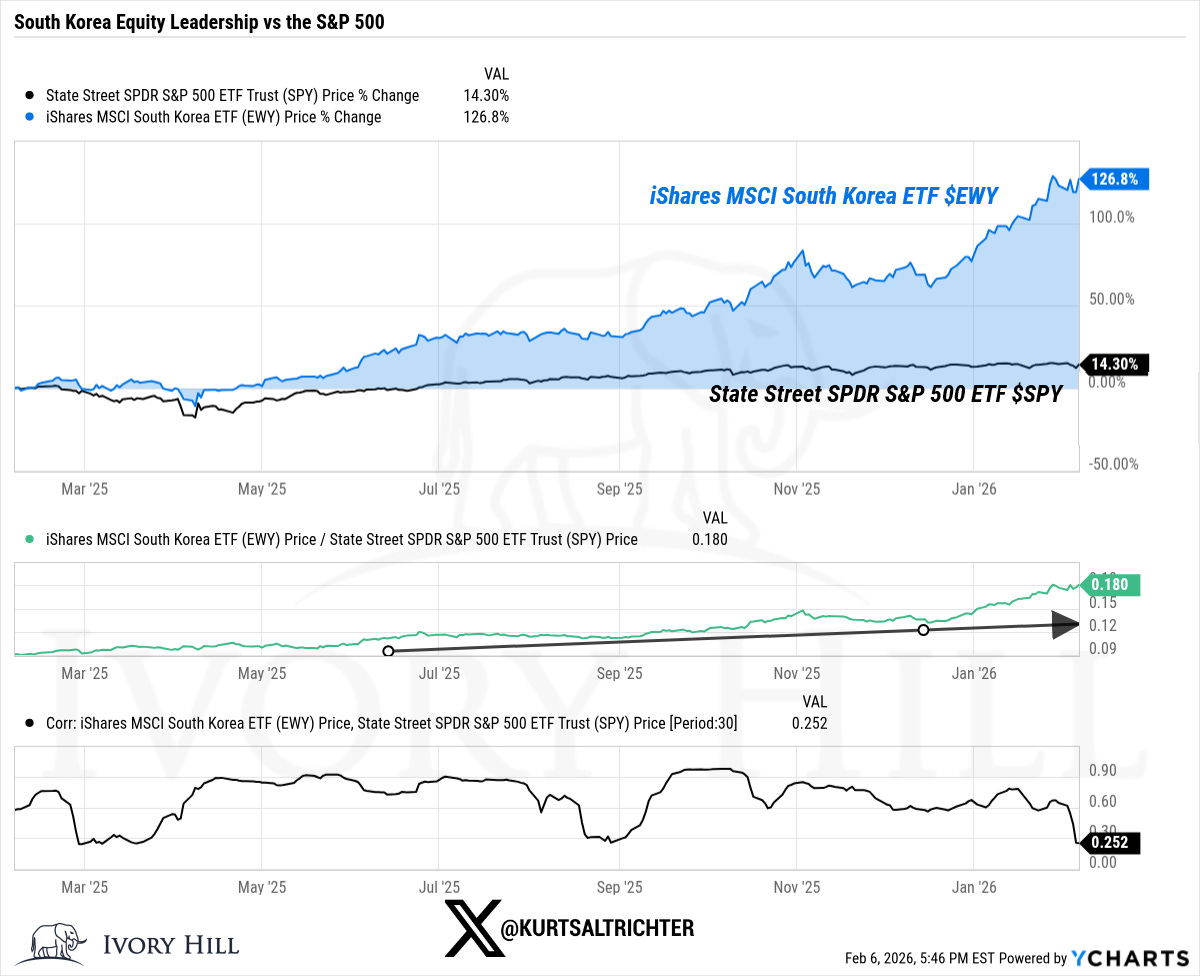

South Korea

We remain long South Korea equities via EWY because the macro, earnings, and market structure signals are aligned. South Korea sits at the intersection of global manufacturing, semiconductors, and cyclical demand. When global PMIs stabilize and tech capex stops contracting, Korea responds early and aggressively. EWY is up roughly 28% YTD, following a ~90–100% gain in 2025, decisively outperforming the S&P 500 while maintaining low correlation. Relative strength versus U.S. equities continues to trend higher, confirming this as leadership, not a late-cycle chase.

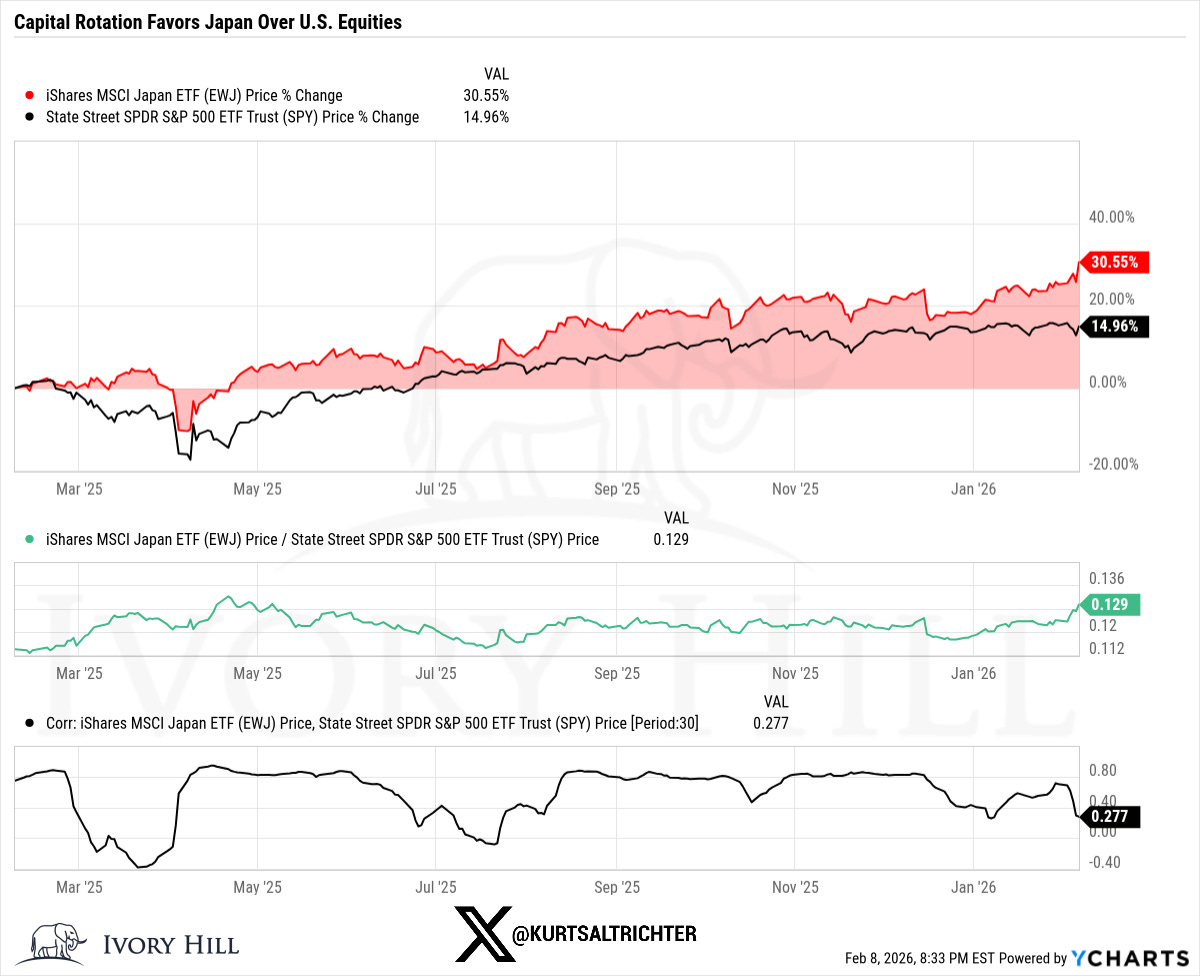

Japan

Japan remains a long. Corporate governance reform is translating into higher buybacks, rising dividends, and improved capital discipline, while a weaker yen continues to support earnings. Just as important, Japan is a critical node in global supply chains, semiconductors, defense, energy security, and practical AI and manufacturing, positioning it as a preferred long-term alternative to China.

You want to be long Japanese equities but short the yen and Japanese bonds, as ultra-loose monetary policy and yield suppression continue to debase the currency and distort the fixed-income market. Relative strength versus the S&P 500 continues to trend higher with low correlation, confirming this is a capital-flow story, not just a valuation trade.

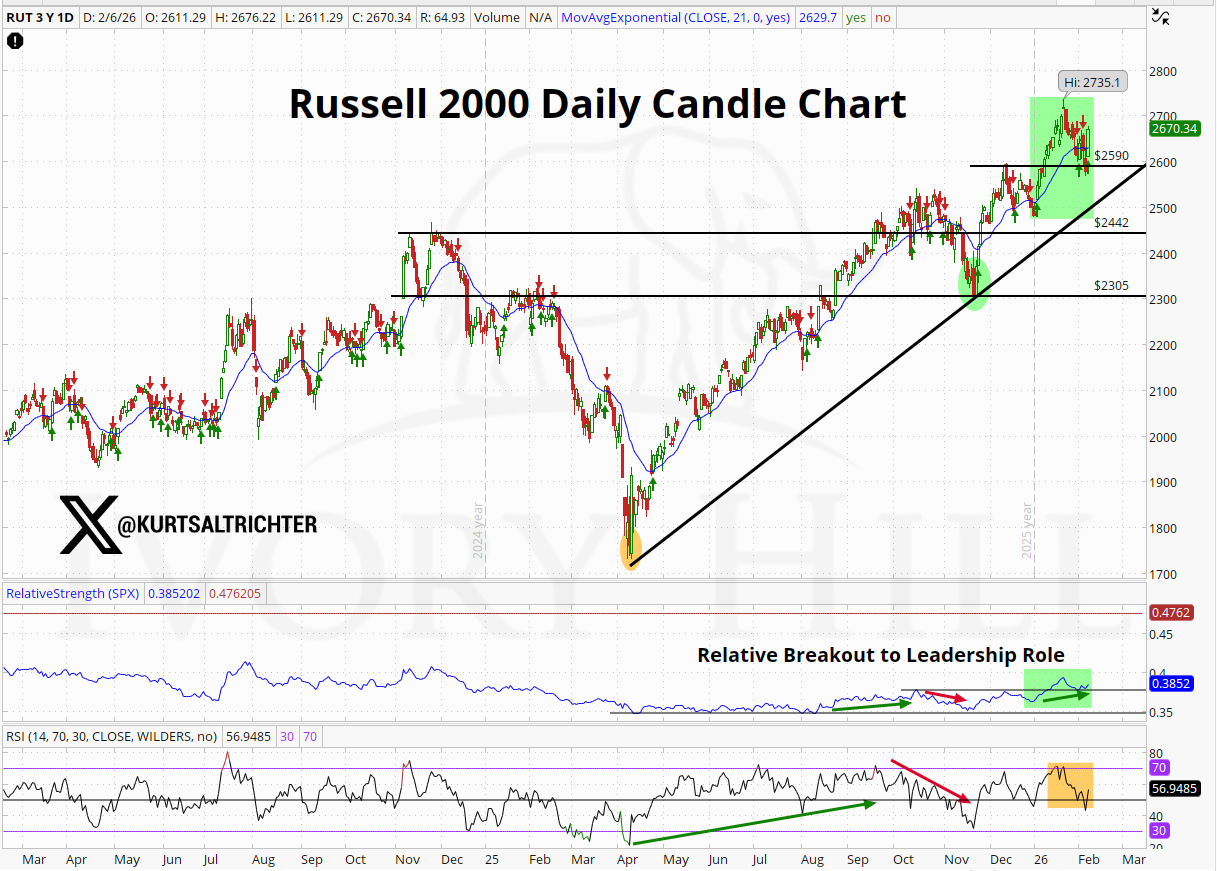

Small-Caps

Small caps tend to move early when breadth improves. That process has already started. We remain long small-caps.

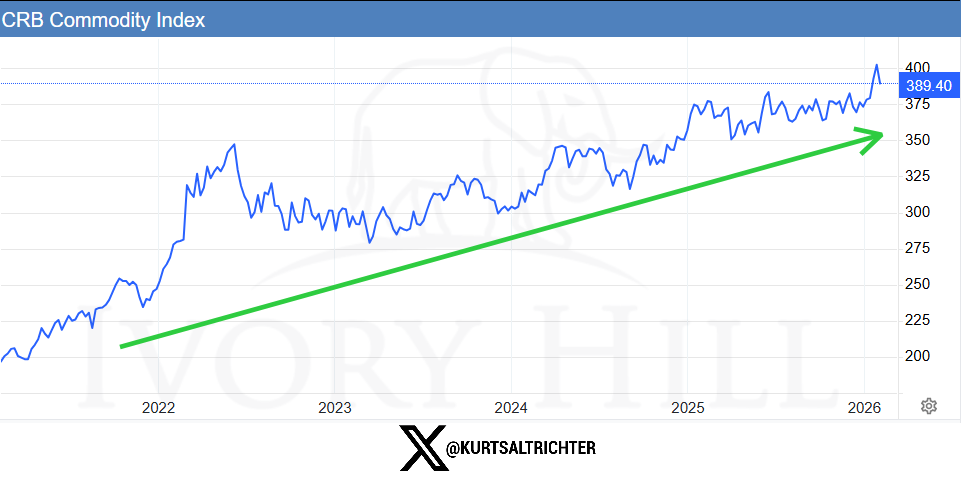

Commodities

Commodities tend to perform best when inflation cools slowly, growth remains intact, and geopolitical risk stays elevated. After a decade of underinvestment, supply constraints in energy and critical metals remain unresolved, new capacity takes years to bring online, and rising demand from electrification, defense spending, and data-center expansion continues to tighten physical markets. That is why our exposure to commodities also increased. The macro backdrop supports it.

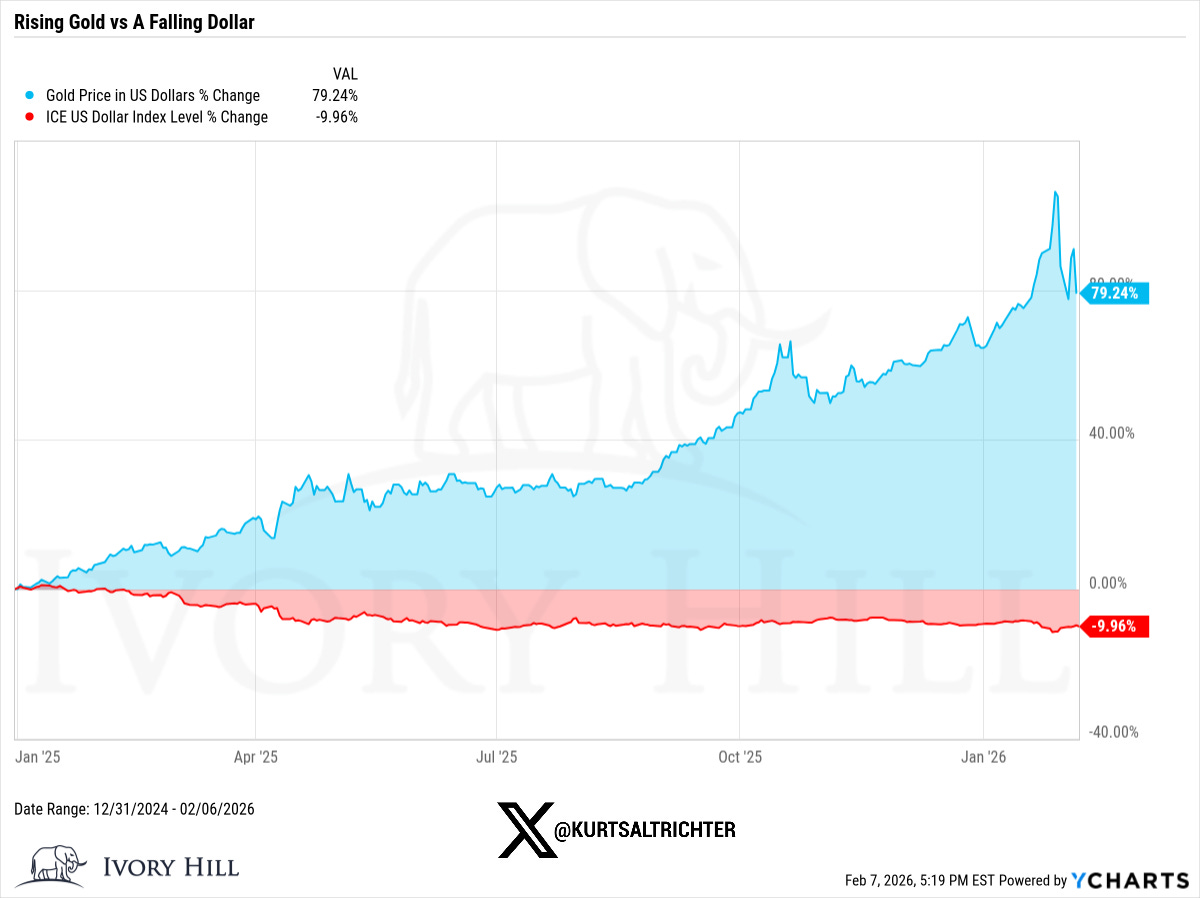

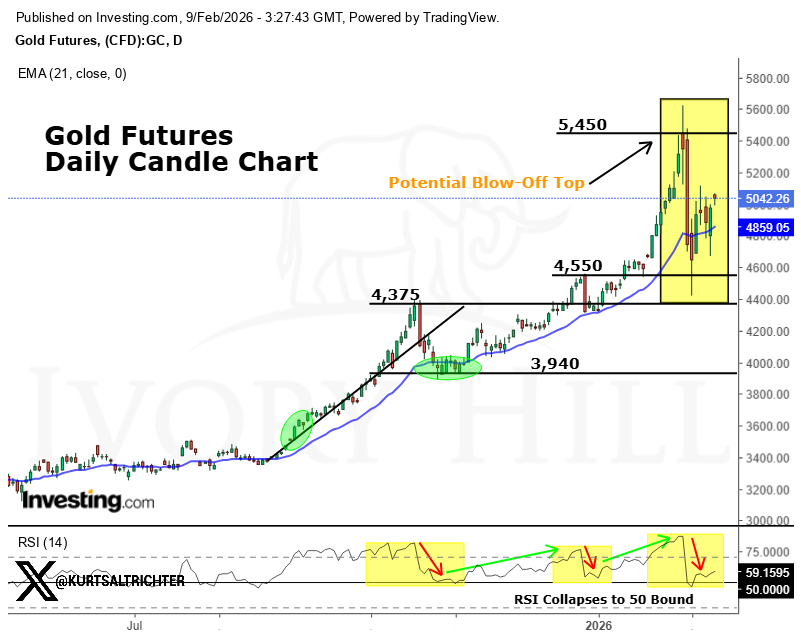

Gold

When investors see central banks sell Treasury holdings while bond markets struggle to absorb rising government issuance, investors lose confidence in Treasuries as a reliable safe-haven asset. Persistent deficits and expanding debt weaken confidence in the dollar’s long-term purchasing power. In this environment, investors don’t move into gold out of fear; they move because it sits outside the bond–currency system entirely. That move is clearly showing up in price behavior.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.