New Era at the Federal Reserve

What Kevin Warsh's Confirmation Means for Markets, Monetary Policy, and Your Portfolio

The Handoff

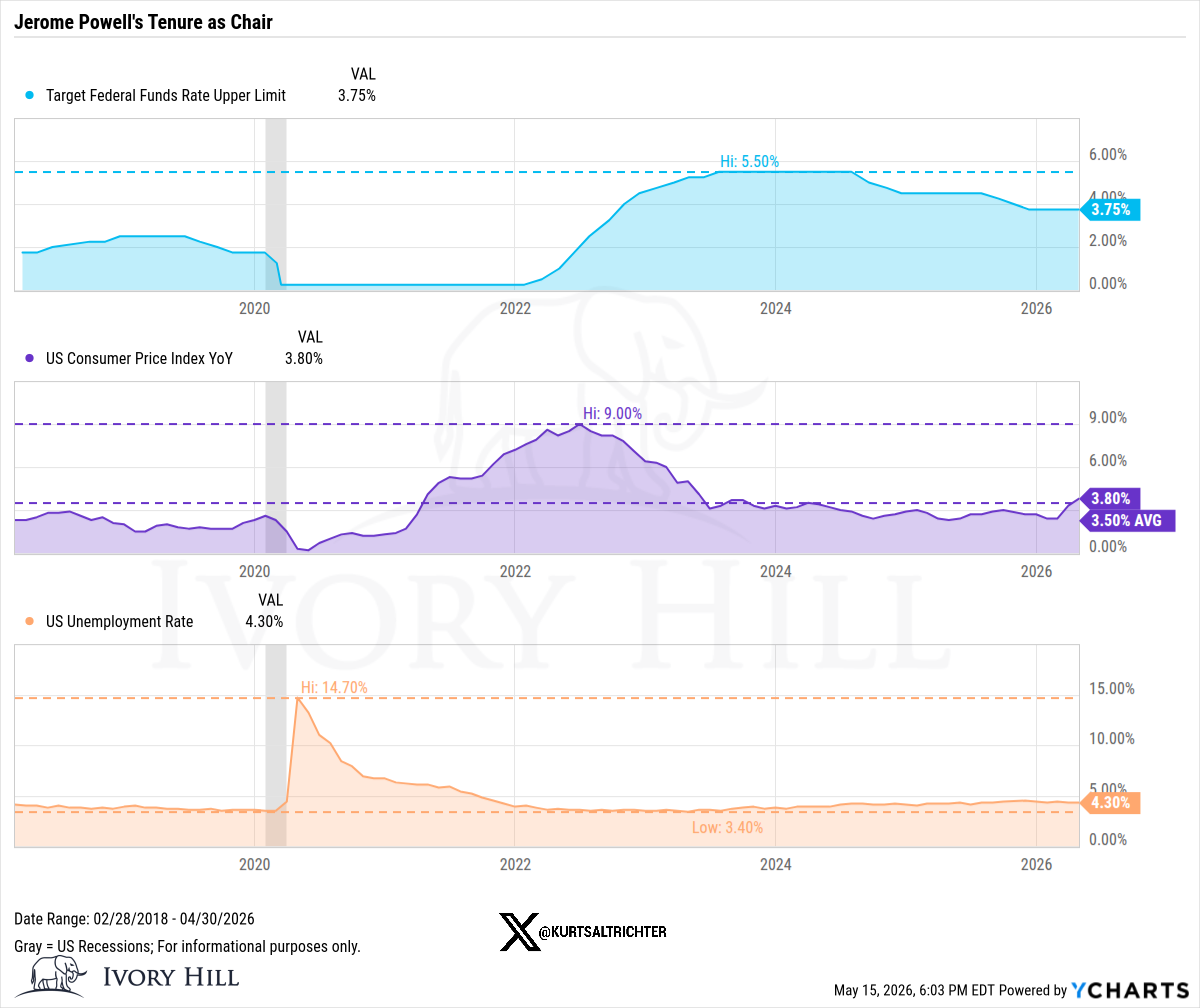

Jerome Powell’s tenure as Federal Reserve Chair ended today. Eight years. A pandemic. The fastest hiking cycle in four decades. And a policy error that will be debated for a generation.

When COVID hit in March 2020, the Fed panicked. Rates went to zero. Asset purchases hit $120 billion a month. By the time that program finally ended in spring 2022, the balance sheet had nearly doubled from $4.2 trillion to almost $9 trillion. The M2 money supply grew by $6.4 trillion in just 22 months, a 42% expansion that was the largest in American history, bigger than the response to World War II and bigger than anything the Fed did after 2008. When inflation started climbing in spring 2021, the Fed called it transitory and kept the foot on the gas. They did not hike until March 2022, by which point CPI was already at 7.9%, and inflation had been running above target for over a year. It peaked at 9.1% in June 2022, three months after the first hike. Late by a mile. From there, Powell did what had to be done: 525 basis points in 16 months, the most aggressive tightening cycle since Volcker. He got inflation down. But the sequence of events is the record. Print $6 trillion. Call it transitory, without ever defining how long transitory is. Wait too long. Then slam the brakes. That is the tenure Kevin Warsh inherits, and it is exactly why he is standing in this building today calling it a regime that needs to change.

Kevin Warsh is now the 17th chair of the Federal Reserve. He was confirmed on Wednesday by the Senate in a 54-45 vote, the closest spread in the modern era. Only one Democrat, Pennsylvania Senator John Fetterman, crossed the aisle. Every other Democrat voted no, primarily on concerns about Fed independence under a president who has made no secret of what he expects from his hand-picked central banker.

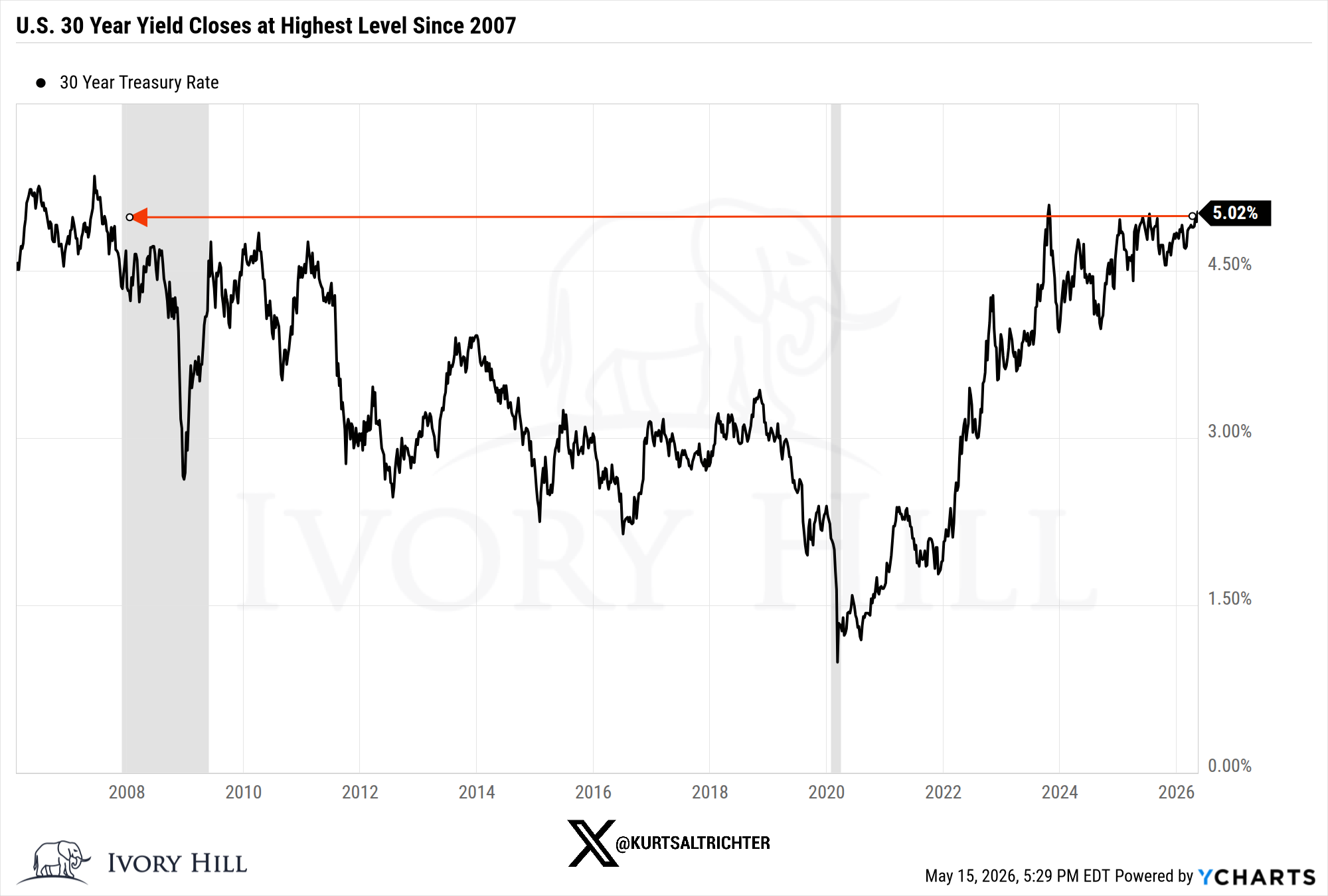

Warsh takes over at exactly the wrong moment for an easy entry. Inflation sits at 3.8% year-over-year as of April 2026, driven higher by energy costs tied to the ongoing Iran war. Wholesale prices came in at 6% in April. The 30-year Treasury yield crossed 5% this week. And the FOMC that Warsh inherits just posted the highest level of internal dissent since 1992, with four of twelve voting members breaking from the majority at the April meeting.

Markets noticed. The S&P 500 and Nasdaq climbed to new all-time highs on confirmation day. The Dow lagged. Investors are not waiting on policy clarity before positioning.

Who Warsh Is and What He Believes

The biographical case for Warsh is strong. He joined the Fed Board of Governors in 2006 at 35, the youngest person ever appointed to that role. Before that: Morgan Stanley VP of Mergers and Acquisitions, then economic advisor to President George W. Bush. He sat at the table for every major decision of the 2008 financial crisis, voting alongside Ben Bernanke as the system nearly came apart.

He left the Board in 2011. His reason matters: Warsh disagreed with the direction of Fed policy. He believed the institution was holding rates too low, expanding its balance sheet too freely, and stretching beyond its core mandate. He walked out on principle, not on convenience. That resignation is the most important data point in understanding what he might do now.

The Balance Sheet Problem

Warsh returns to a Fed carrying a balance sheet 51.8% larger than when Powell started. That is not a rounding error. That balance sheet is the product of two rounds of quantitative easing, pandemic-era emergency purchases, and years of slow drawdown that left the Fed deeply embedded in financial markets in ways Warsh has consistently criticized.

He has publicly argued that the Fed’s bond-buying programs undermine institutional independence because they amount to backstopping government borrowing. He wants the balance sheet reduced. The question is pace and sequencing, both of which carry significant market implications. Any aggressive balance sheet reduction that tightens financial conditions faster than rate moves alone would be a meaningful regime shift.

The Inflation Framework Shift

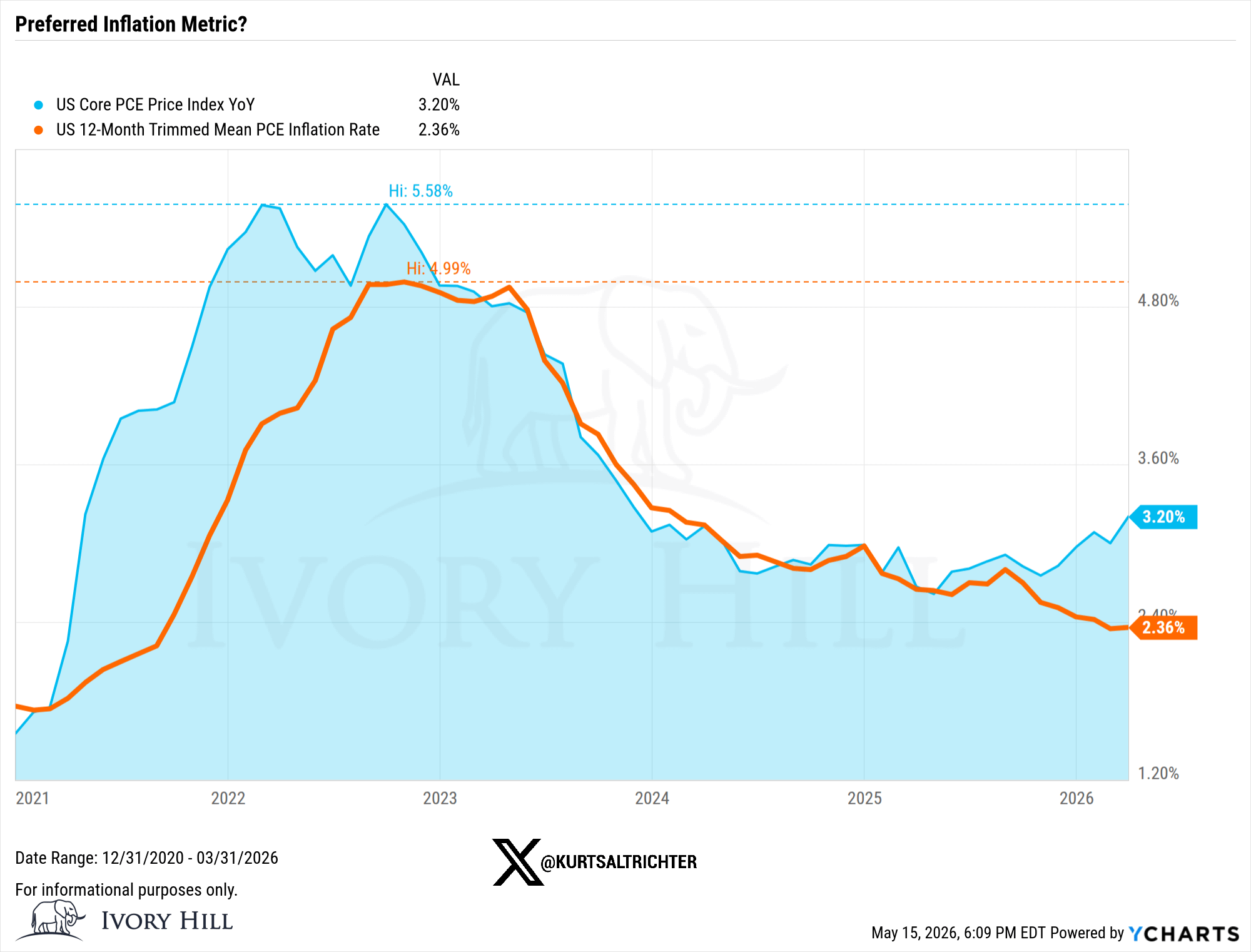

Warsh has signaled he wants to change the Fed’s preferred inflation gauge. The Fed has used Core PCE, which excludes food and energy, as its benchmark since 2000. Warsh favors Trimmed Mean PCE, which removes the most extreme price movements each month instead of excluding whole categories. The practical difference: Trimmed Mean PCE currently reads 2.36%, well below the 3.20% reading on Core PCE. Depending on which measure the Fed follows, the case for rate cuts looks very different.

This is not a minor procedural change. The metric the Fed uses to gauge inflation directly determines when it judges the economy to be at target. If Warsh moves the committee toward Trimmed Mean PCE, he is mathematically moving the Fed closer to a declared victory on inflation, which creates runway for rate cuts even as headline readings stay elevated. You’d think with 400+ Ph.D. economists and 500+ researchers on the payroll, the Fed would run the most sophisticated macro forecasting operation on the planet, leaving Bloomberg and every major hedge fund in the dust. Not even close. When the data doesn’t cooperate, just change the data. Same thing I saw in the Army when time or weather worked against leadership, and we would quietly move the goalposts rather than admit the standard couldn’t be met. Can you tell why I didn’t stick around for the full 20 years?

Less Communication, More Volatility

Warsh has also indicated he may not hold press conferences after every FOMC meeting. He said during his confirmation hearing that truth-seeking matters more than repetition. That is a pointed departure from the Powell era, where post-meeting press conferences became a fixture of market communication and the primary mechanism through which the Fed managed expectations in real time.

Markets spent the last several years trading heavily on Fed communication. Every word choice in a statement, every pause in a press conference, every shift from “patient” to “attentive” moved asset prices. If Warsh removes that communication pipeline, FOMC meeting days become higher-volatility events by design. Traders and AI quants who have built positioning strategies around parsing Fed language will need to adjust.

What the Markets Are Pricing

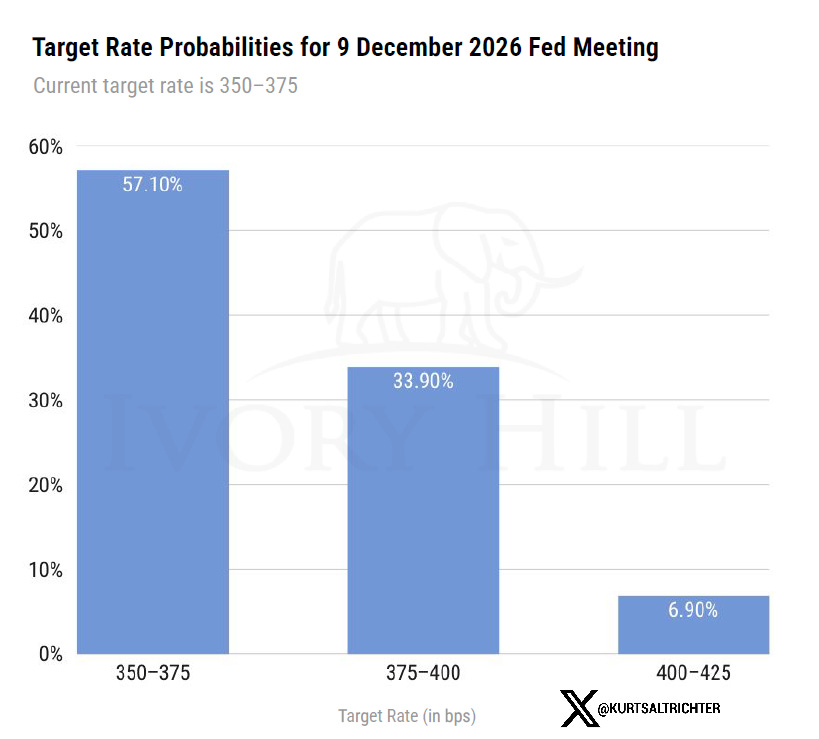

FedWatch probabilities as of this week show a 57% chance that rates remain unchanged through the December 2026 FOMC meeting, with roughly 34% pricing in one cut to 375-400 basis points and about 7% pricing in two cuts to 400-425. The probability of a rate hike has risen to approximately 20-30% by year-end on some measures, driven by the persistent inflation data and geopolitical energy risk.

That is not a rate-cut market. That is a hold-with-upside-risk-to-hikes market. Investors who entered 2026 expecting multiple cuts are being asked to reprice that view against an incoming chair who is hawkish by record, inheriting an inflation problem complicated by war.

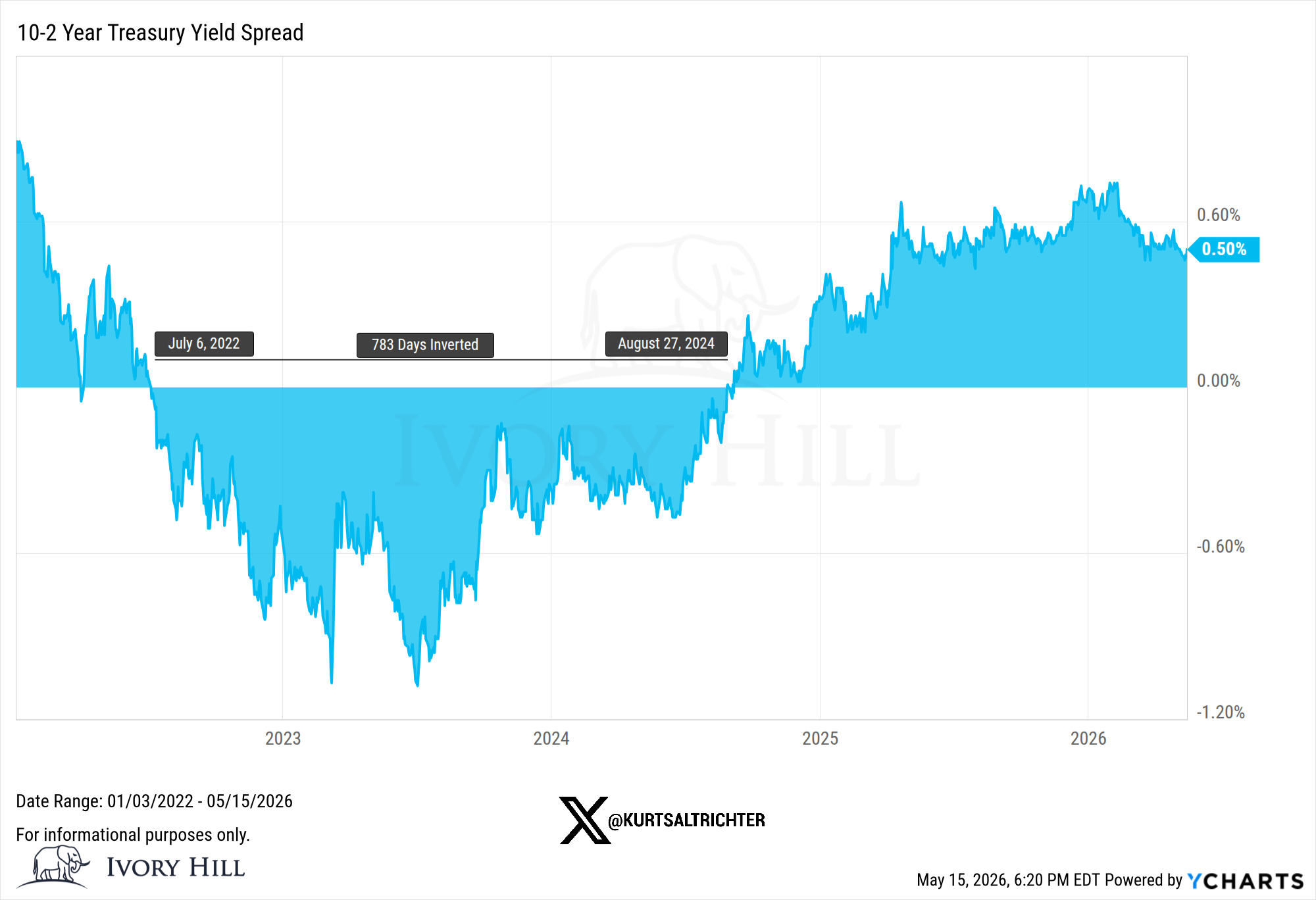

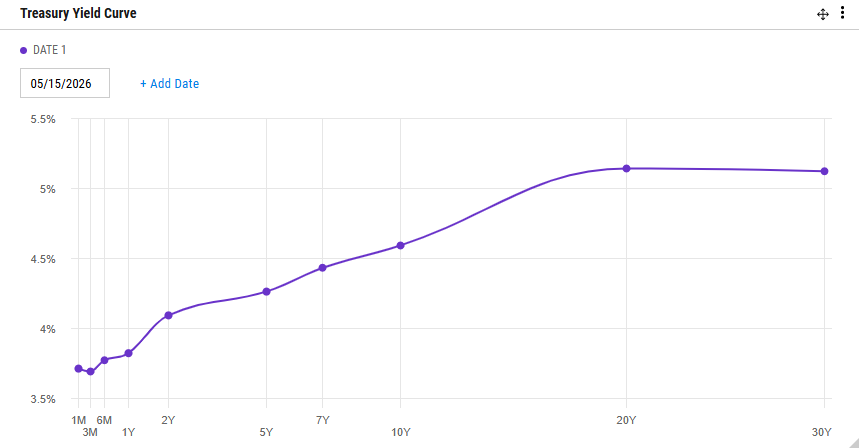

The yield curve has normalized after 783 days of inversion. The 10-2-year Treasury spread returned to positive territory in August 2024 and currently sits at 0.48%. Short-duration instruments are earning competitive yields today, but that yield resets as rates move. If Warsh holds longer than the market expects, short-term rates stay higher for longer, and the reinvestment calculus for fixed-income ladders changes.

The 30-year yield crossing 5% on confirmation day was the bond market sending a message. Long-duration borrowing costs are rising. That has direct consequences for mortgage rates, corporate debt refinancing, and valuations on any asset priced on a long-duration discount rate, including equities with long earnings runways.

Is Warsh a Sock Puppet for Trump?

This is the question that defined his confirmation fight, and it deserves a direct answer rather than a diplomatic one.

Senator Elizabeth Warren called him a “sock puppet” for Trump during his confirmation hearing. Republican Senator John Kennedy of Louisiana, in a moment of unvarnished directness, asked Warsh himself: “Are you going to be the president’s human sock puppet?” Warsh pushed back on both. He testified that he is committed to ensuring the conduct of monetary policy remains strictly independent and that independence is up to the Fed.

The skeptic’s case is not crazy. Trump nominated Warsh after more than a year of publicly attacking Powell for not cutting rates fast enough. The Wall Street Journal reported that Warsh spent the past year building a case for rate cuts that aligned closely with what the administration wanted. The DOJ opened a criminal investigation into the Fed’s building renovations during this period, a probe widely viewed as political pressure on the institution. That investigation was dropped in April, clearing the path for Warsh’s confirmation. Trump has already joked that he would sue Warsh if he does not cut rates.

The confirmation vote itself was the most partisan in Fed history. That does not happen in a vacuum. It reflects genuine concern that Warsh is a vehicle for executive influence over monetary policy, not an independent actor.

The Case He Is Not

Here is what cuts against the puppet narrative.

Warsh’s record is hawkish. He resigned from the Fed in 2011 specifically because he thought policy was too loose. His criticism of QE, his concern about the balance sheet, his focus on inflation credibility over near-term stimulus, these are the positions of someone who has historically wanted tighter policy, not easier. That is the opposite of what Trump wants.

Finance industry veterans tend to maintain hawkish instincts even under political pressure. Powell himself was a Trump appointee in the first term and resisted sustained pressure to cut rates. The pattern of Fed chairs ultimately governing with more independence than their appointments suggested is well established.

Warsh also faces a divided FOMC. He controls the agenda. He does not control the votes. Four members dissented at the April meeting. He cannot simply announce rate cuts and have the committee comply. Building consensus on a committee with serious inflation concerns and a history of recent dissent will require him to govern on the data, not on presidential preference.

The most direct framing is this: Warsh and Trump want the same near-term outcome, lower rates, but for structurally different reasons. Trump wants lower rates to stimulate the economy politically. Warsh wants a framework that justifies lower rates through a different inflation lens. If inflation stays elevated due to energy shocks and tariffs, their interests diverge. That is the moment that will define whether the independence concern was real.

Let me be direct. Whatever your political views, the market demands at least the appearance of Fed independence. The moment traders believe Trump is actually running monetary policy, equity markets crash. FAST. That reality alone makes it nearly impossible for Warsh to function as a White House proxy. The market enforces independence whether Washington wants it or not.

The Volcker Precedent

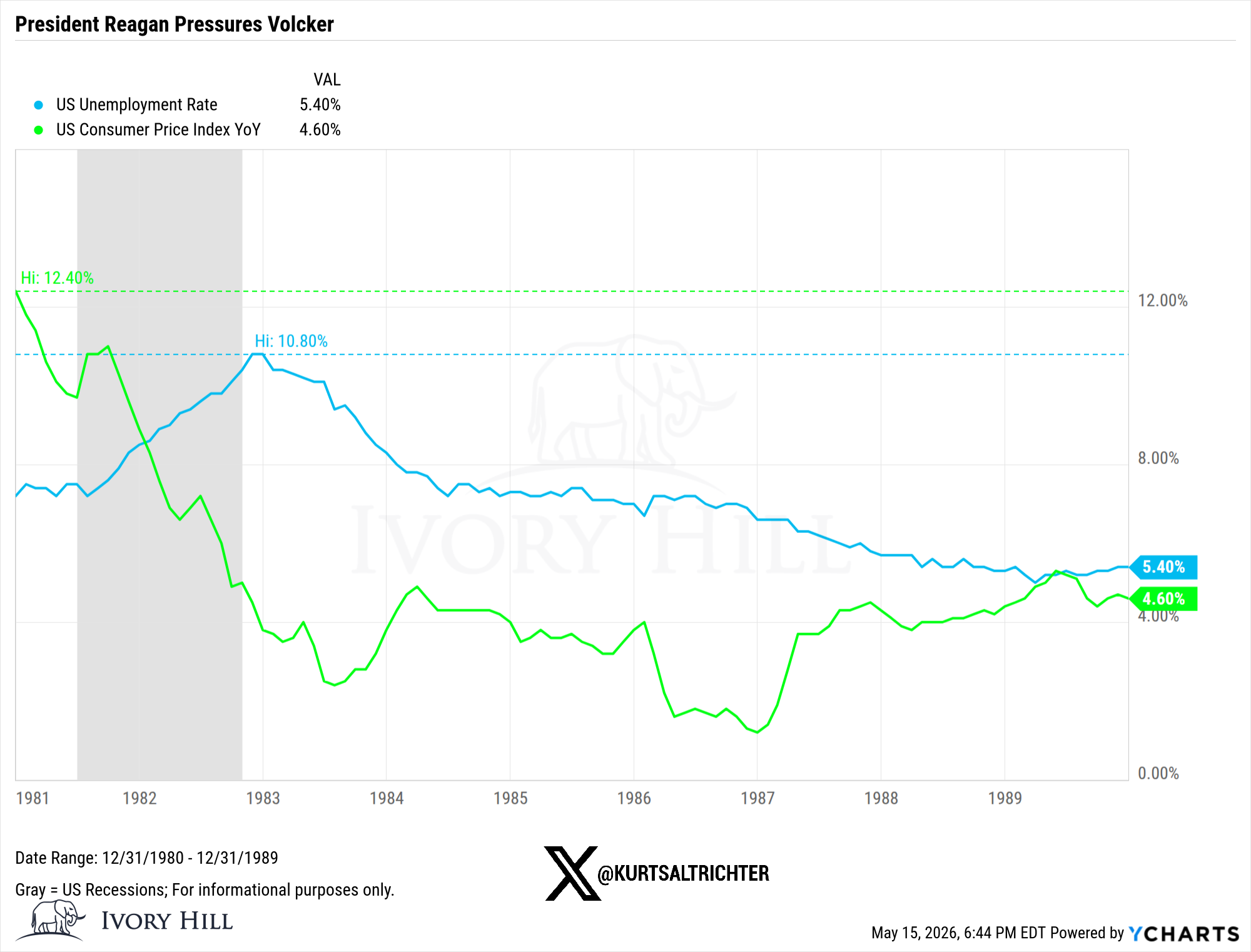

Reagan pressured Paul Volcker to cut rates in 1982 as unemployment neared 11%. Volcker held firm and let the data drive decisions. Inflation collapsed. The economy stabilized for the remainder of the decade. That episode remains the benchmark case for why Fed independence produces better long-run outcomes than politically convenient monetary policy.

Warsh knows that history. He has cited it. Whether he lives it when Trump is in his ear with rate-cut demands in Q3 is the bet investors are being asked to make right now.

What History Says About Fed Transitions

Every new Fed chair has stepped into uncertainty. The data is worth revisiting without the emotional filter of the current moment.

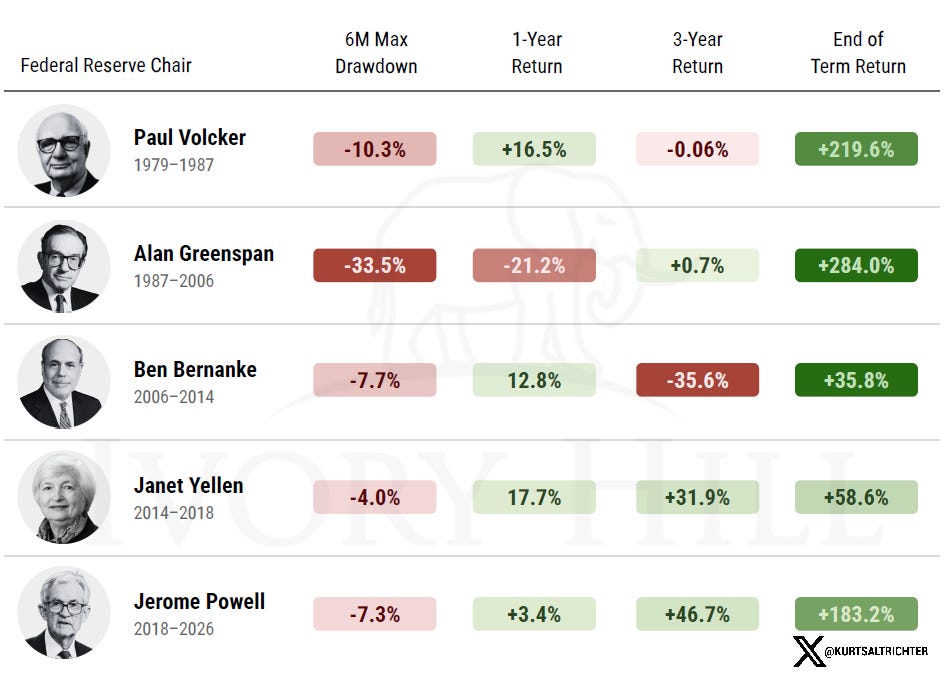

Paul “Raised Rates to 20%” Volcker served 1979-1987. His six-month maximum drawdown was -10.3%. His one-year return was +16.5%. His end-of-tenure S&P 500 return: +219.6%. The man who raised rates to 20% to kill inflation delivered generational equity returns over his tenure.

Alan "Irrational Exuberance" Greenspan ran 1987-2006. His six-month max drawdown was -33.5%, which includes the dot-com collapse. His one-year return was -21.2%. His end-of-tenure return was +284.0%. The volatility was real and severe, but the long end was strongly positive.

Ben "Too Big To Fail" Bernanke served through the 2008 financial crisis. His three-year return was -35.6%, a genuine catastrophe by any measure. His end-of-tenure return was +35.8%. He navigated the worst financial crisis since the Great Depression and the market still recovered.

Janet "The Consumer is Strong"Yellen’s tenure was the cleanest of the modern era. A -4.0% six-month max drawdown, a +17.7% one-year return, +31.9% over three years, +58.6% at end of tenure. Low volatility, methodical policy.

Jerome “It’s Transitory” Powell: -7.3% six-month drawdown, +3.4% one-year return, +46.7% three-year return, +183.2% end-of-tenure return despite a pandemic, 40-year inflation spike, and historic rate-hiking cycle.

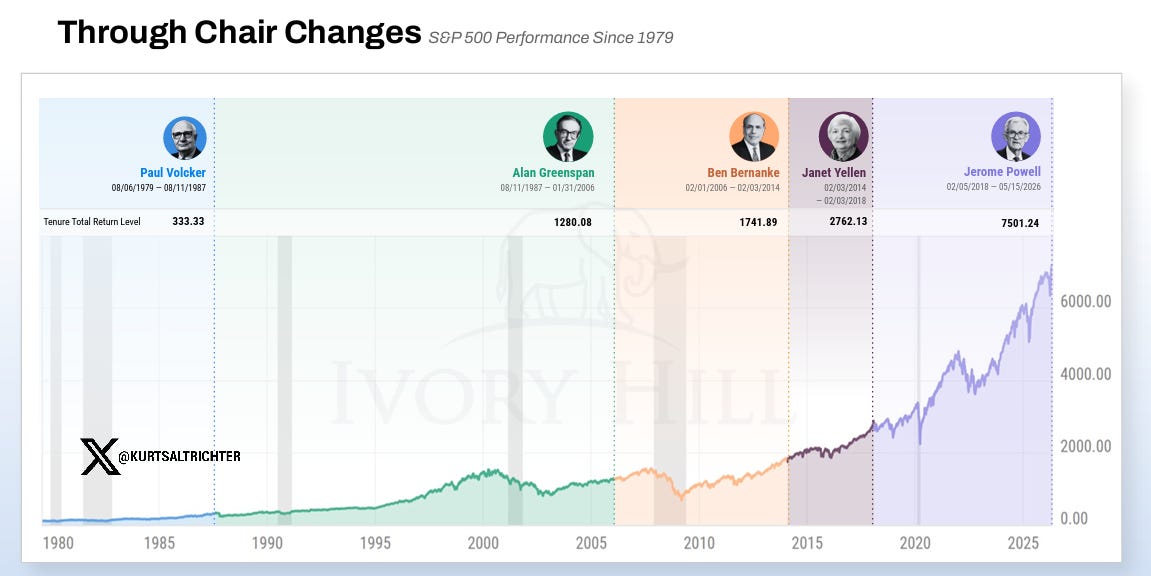

Since Volcker took the chair in 1979, the S&P 500 has returned over 3,840% through multiple recessions, bear markets, crises, and transitions. The noise of a chair change has never been the signal to abandon a disciplined investment strategy.

What Investors Should Take Away

The Rate Path Is Not Warsh’s Alone to Set

The Fed Chair sets the agenda. He does not set the rate. Twelve voting members of the FOMC decide, and Warsh inherits a committee with the most internal dissent in 34 years. Any meaningful shift in rate policy requires coalition-building, not declaration. Warsh’s first FOMC meeting as chair is June 16-17. Watch the statement language, the dissent count, and the press conference tone, if he holds one.

The Inflation Framework Shift Is the Most Consequential Variable

If Warsh successfully moves the Fed toward Trimmed Mean PCE as its benchmark gauge, he is changing the goalposts. At 2.36% versus Core PCE at 3.20%, that shift alone materially changes the rate-cut calculus. This is a policy change that does not require a vote. It requires persuasion and framework review. Watch for any language in FOMC communications signaling a review of the inflation measurement methodology.

Fixed Income Duration Risk Is Real

Short-duration instruments are earning competitive yields today, but yield resets with rate movements. If Warsh holds longer than market consensus expects, and the data suggest he might, the reinvestment risk on short-duration ladders matters. Advisors with clients heavily positioned in money markets and short T-bills should revisit duration assumptions in the context of a potentially extended hold.

The Long-End Warning

The 30-year Treasury at 5% is not a neutral signal. Elevated long-end yields tighten financial conditions, increase mortgage costs, raise the cost of corporate debt refinancing, and put pressure on equity valuations in rate-sensitive sectors. This does not require a rate hike to create tightening pressure. Watch the 10-year yield as the primary indicator of how markets are processing Warsh’s expected policy path.

The Transition Itself Is Not the Risk

Fed transitions have happened sixteen times since the institution was founded. Markets have processed every one of them. The uncertainty of a new chair is not structural risk; it is episodic noise. Investors who reposition dramatically based on leadership change rather than actual policy outcomes have historically given up returns they could not recover. The playbook is clear: monitor, adjust at the margin as the data develops, and resist the narrative that this time is categorically different.

The Bottom Line

Warsh is not Powell. He has sharper inflation instincts, different communication preferences, a balance sheet agenda, and a political patron who has publicly defined success as rate cuts. The tension between those last two facts is the dominant risk of his tenure. If inflation stays elevated, Trump wants cuts, and the data argues against them. That is where independence is either real or it is not.

The historical record says bet on independence. The structural record says the Fed Chair is one voice among twelve. The data record says Fed transitions do not determine long-run portfolio outcomes.

What Warsh does with the inflation framework, the balance sheet, and the first real test from the White House will answer the sock puppet question better than any confirmation hearing could.

The June meeting is the first real data point. Until then, the thesis is watch and stay disciplined.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.