October Market Expectations

Fundamentals Are Saying More Downside is Likely

The downturn in both stocks and bonds during September was foreseeable, given that three out of the four market drivers identified in the report from September 7th manifested in the "Conditions Get Worse" scenario, thus justifying the market declines based on fundamental factors.

More precisely, in the table for September, it was outlined that with respect to the Federal Reserve's policy outlook, should the Fed maintain the prospect of a 2023 rate hike while delaying the anticipated timing of the initial rate cut to post-June 2024, it would adversely impact the markets. This note was confirmed during the September FOMC meeting when the Federal Reserve's projections indicated:

An additional rate hike in 2023, and;

a mere 50 basis points of cuts in 2024, altering the market's anticipation for a rate cut to July, as opposed to the earlier projection of May or June.

In the September table concerning Treasury yields, it was pointed out a potential downturn if the 10-year Treasury yield climbed over 4.50%. This came to fruition when the 10-year yield soared to a new 16-year high last week, surpassing 4.80%, with the prospect of reaching 5.00% now appearing plausible.

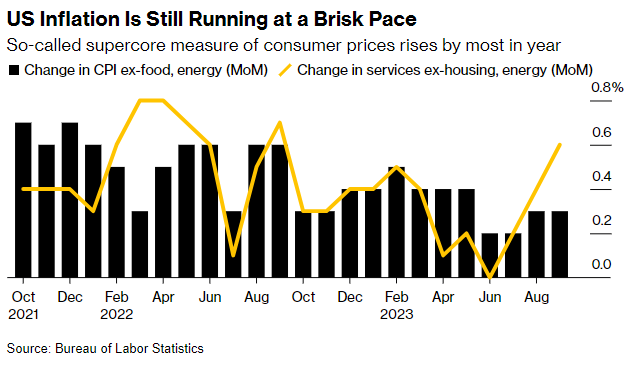

In September, it was also highlighted that the situation could deteriorate if the core Consumer Price Index (CPI) experienced a rebound in the subsequent months and persistent inflation left the door open for the Federal Reserve to implement another rate hike. Yesterday, it came to light that the Core CPI has indeed increased for the second consecutive month.

Here's the main takeaway: Observing three fourths of the prevailing market influencers deteriorate over the past month clarifies the recent declines in stocks, rendering them entirely rational.

Current Situation:

Current data continues to indicate a soft landing scenario, showcasing a moderated economic deceleration.

Disinflation is in progress, albeit not as robustly as desired, hinting at lingering inflationary pressures.

The possibility of a rate hike in 2023 remains, with no rate cuts foreseen until summer 2024, reflecting a cautious monetary policy stance.

Treasury yields have soared to 16-year highs, presenting a significant marker of sentiment.

Conditions Get Better If:

A 'no landing' or 'soft landing' scenario, supported by data, would indicate a favorable economic trajectory.

A substantial and continuous drop in core inflation nearing 3.0% year-on-year would be a positive sign.

Confirmation of no further rate hikes in 2023 and a softened 'higher for longer' stance would likely bolster market confidence.

A decline in Treasury yields could alleviate market pressures and foster a more favorable investment climate.

Conditions Get Worse If:

Economic data points to a hard landing

Core inflation levels off or bounces (inflation is rising)

Fed hikes again in 2023 (maybe)

10-year yield moves close to, or above 5% (closed today at 4.703%)

It's crucial to remember that you cannot control the market, your advisor cannot control the market, your elected officials cannot control the market so just let the market do what it is going to do; our role is to ride its waves, honing our focus on the controllables like risk management, position sizing, and maintaining emotional equilibrium.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President