S&P 500 Recession Targets

Late-Cycle Volatility, but a Market Top is Unlikely

I've been saying all year to expect higher volatility in the second half of this year. And, just as anticipated, it came bursting through our door like Cosmo Kramer in Seinfeld.

Our signals have not changed. Our long-term RiskSIGNAL remains green but is weakening. A bit more downside is needed to trigger a red signal, at which point we will increase our cash levels further.

The VIX, often called the fear index, hit 65 this morning, signaling widespread capitulation. In our view, the selloff has been excessive. Significant technical damage has occurred, and correcting it will require time and continued volatility.

Over the past few weeks, I noted that we’ve reduced our high-beta positions, leading to a 20% cash accumulation. If the market decline continues, I anticipate our long-term signal to turn red as early as this week, increasing our cash holdings further. This has/will provide us with significant buying power when the market eventually rebounds, which I believe it will.

Following a major selloff like this, I expect a brief rally, followed by another dip that retests the lows. This process should establish a new foundation for the market to rise.

It’s important to remember that 10% corrections are a normal part of market cycles, even during bull markets. The recent downturn has inflicted technical damage on equity indices, and it will take time to recover.

S&P 500 Recession Targets

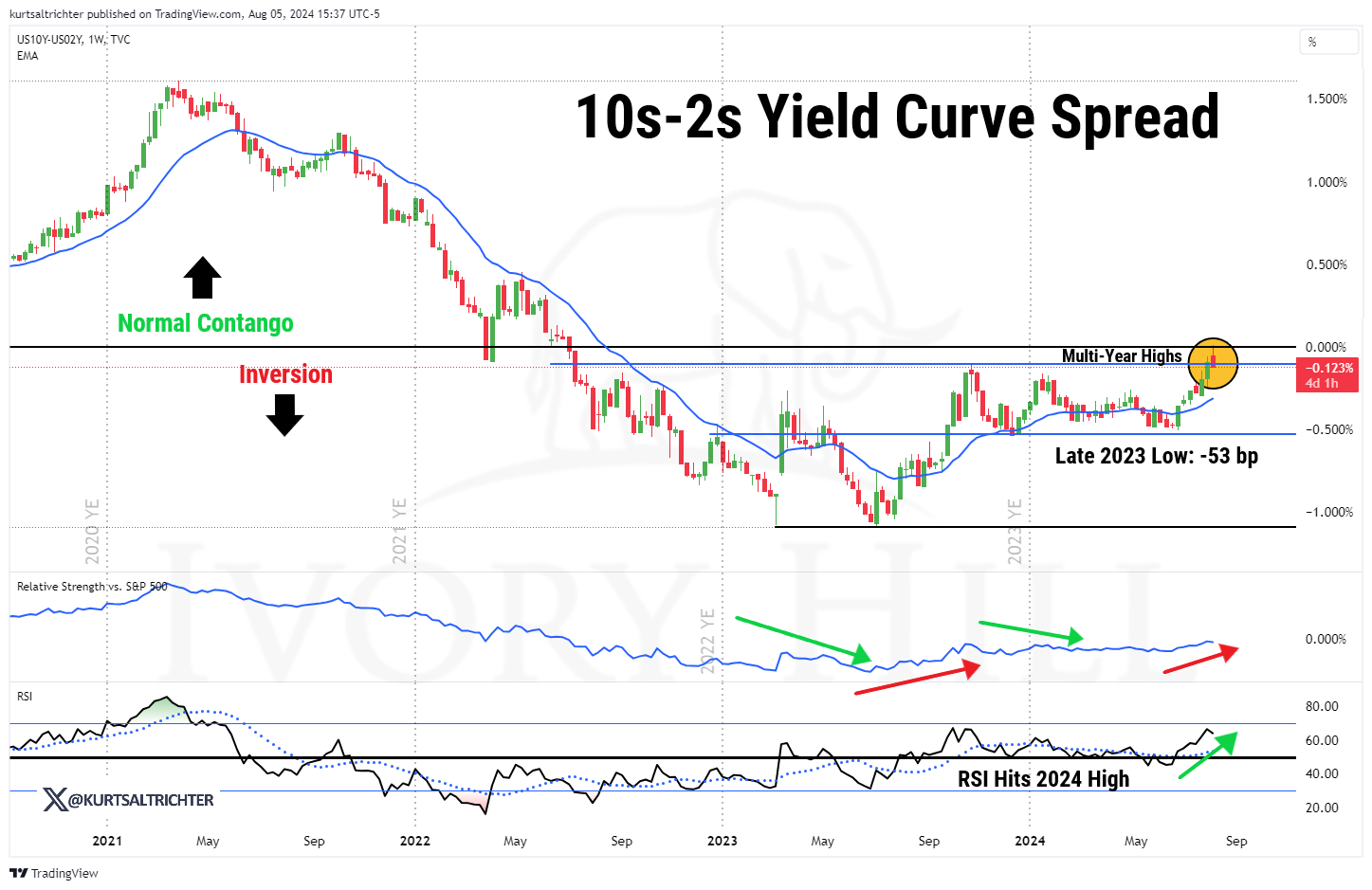

Following a series of negative economic data points last week, market volatility has surged significantly, resulting in a steep decline in stock prices. The inverted yield curve has indicated the risk of a recession for over two years. The market's heightened reaction to the unfavorable economic news was further intensified by the unwinding of the "Yen Carry Trade" and the subsequent unwinding of the "Short-Volatility Trade," both of which have supported equity markets for many quarters.

Looking ahead, it wouldn’t be surprising to see a relief rally or even new all-time highs in the stock market, similar to the dynamics seen in October 2007. However, my cycle analysis indicates that the risk of a prolonged bear market in stocks is currently as high as it was before the 2008 Global Financial Crisis. Therefore, it’s crucial to have target levels in mind to prepare for potential declines in stock prices.

Historical data shows that the S&P 500 has typically retraced gains following a yield curve inversion during subsequent recessionary bear markets. Using the two yield curve spreads, I have identified the following Recession Targets for the S&P 500.

10Y-2Y S&P 500 Recession Target: 4,440

10Y-3M S&P 500 Recession Target: 3,600-3,850

The market dynamics began to shift in July, with the unwinding of the overcrowded Yen Carry Trade. This shift saw money moving out of the concentrated mega-cap tech positions, which had driven most of the S&P 500’s 2024 gains, and into the broader market, including the Russell 2000. In mid-July, I discussed how the unwinding of the carry trade would impact markets, pressuring the tech-heavy Nasdaq 100 while boosting the Russell 2000. The USD/JPY remains the best indicator for tracking the influence of the Yen Carry Trade.

If the yen strengthens (USD/JPY falls), expect more equity market volatility. Conversely, if the yen weakens (USD/JPY stabilizes), it could set the stage for a stock market relief rally.

For those looking for a tradeable bottom in stocks, it’s important to see the yen rally stall and the VIX retreat from its 52-week highs; otherwise, more selling pressure is likely in the near term.

Several developments last week suggest that while the economy is trending toward a recession, there is still some time left in the current expansionary cycle. In Treasuries, the crash in yields across durations has shifted the trend in yields lower (bullish for bonds).

The 10s-2s yield curve spread on the brink of reversion underscores late-cycle risks, but the 10Y-3M spread dropping towards 2024 lows suggests more time for stocks to pursue new highs.

Credit spreads widened but remain more than 100 basis points from 52-week highs, typically reached before a recession. Be direct: Watch for new 52-week highs in credit spreads.

The surge in the VIX, likely amplified by market mechanics, suggests that a reversion towards 20 or below should support the S&P 500.

Bottom line, the combination of the declining 10Y-3M yield curve spread and still tight credit spreads favors equity bulls for now, suggesting this is a bout of low conviction, late-cycle volatility rather than a definitive lasting top in stocks.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Email: kurt@ivoryhill.com | ivoryhill.com