The Bond Market Isn't Buying This Rally. Neither Am I.

The equity market is pricing in the best case. Here's what two other major markets are telling you instead.

“Rule #2: Excess moves in one direction will lead to an excess move in the opposite direction.”

– Bob Farrel

The S&P 500 has fully erased every point it lost from the U.S./Iran war. As of yesterday, the index is sitting 1% above where it was on February 27, the day before the first strike on Iran. Less than 1% from an all-time high.

We have done a full round trip in just 10 trading days.

And I’ll be direct, if you’re only looking at equity markets right now, this looks like a clean bill of health. The war started, market drops, then the market recovers, everyone moves on. Except that’s not what’s actually happening when you look at the full picture.

The bond market hasn’t confirmed this rally.

Oil hasn’t confirmed this rally.

And when two of the most important markets in the world are telling a different story than equities, that’s not something you just ignore.

What stocks are pricing in right now

For the S&P 500 to be sitting above pre-war levels, you have to believe all of this simultaneously:

Oil at these levels isn’t high enough to slow the consumer down in any real way.

The Fed is going to look past hot inflation prints and cut rates anyway.

Higher input and transportation costs won’t show up in corporate margins.

And the Middle East conflict is close enough to being resolved that none of this matters in six months.

Maybe that’s how it plays out. I’m not saying it’s impossible. But that is an aggressive set of assumptions, and right now, the data coming out of bonds and oil is not backing any of it up.

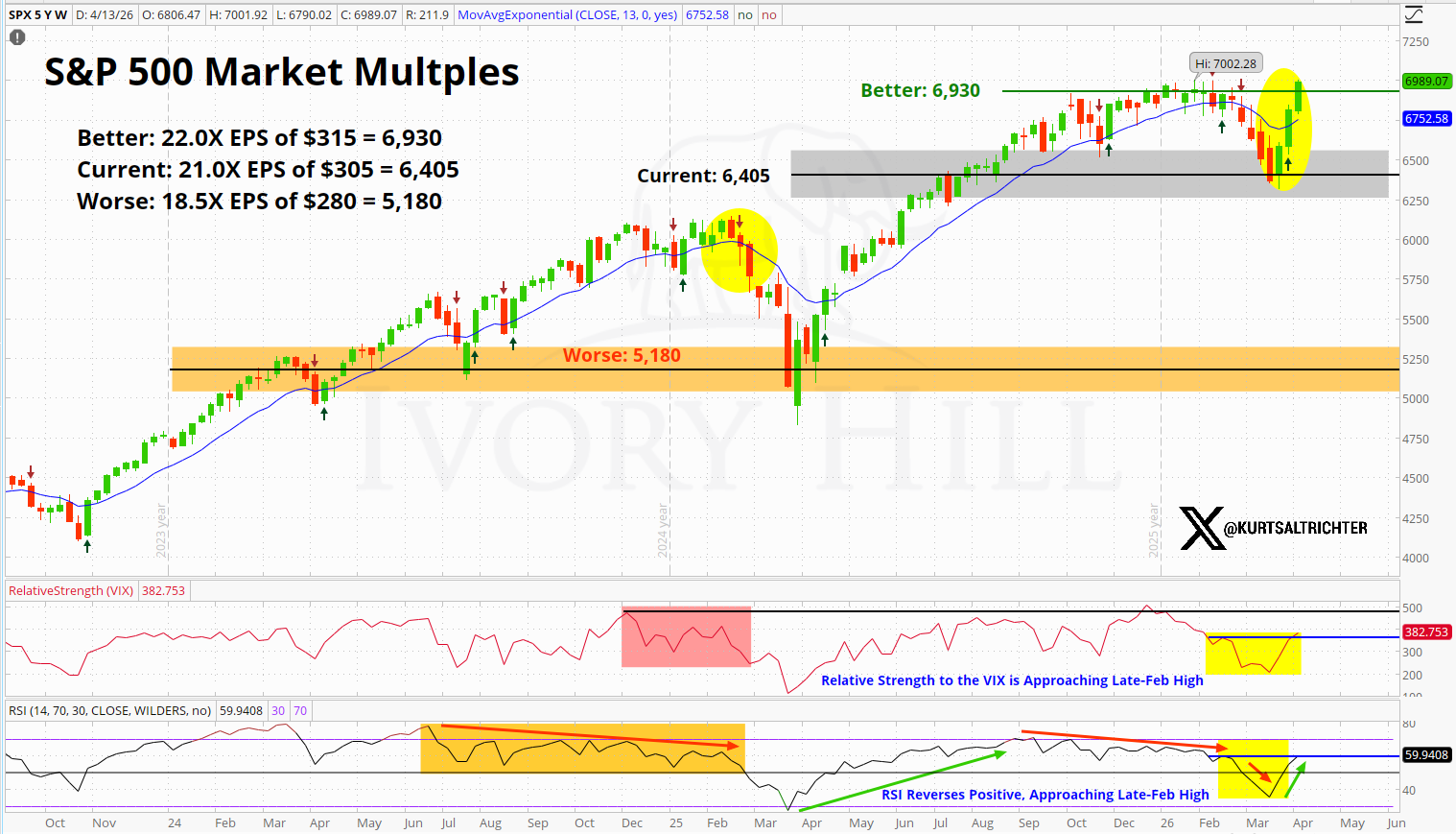

Based on fundamentals, stocks are priced for perfection.

Let’s talk about the actual numbers

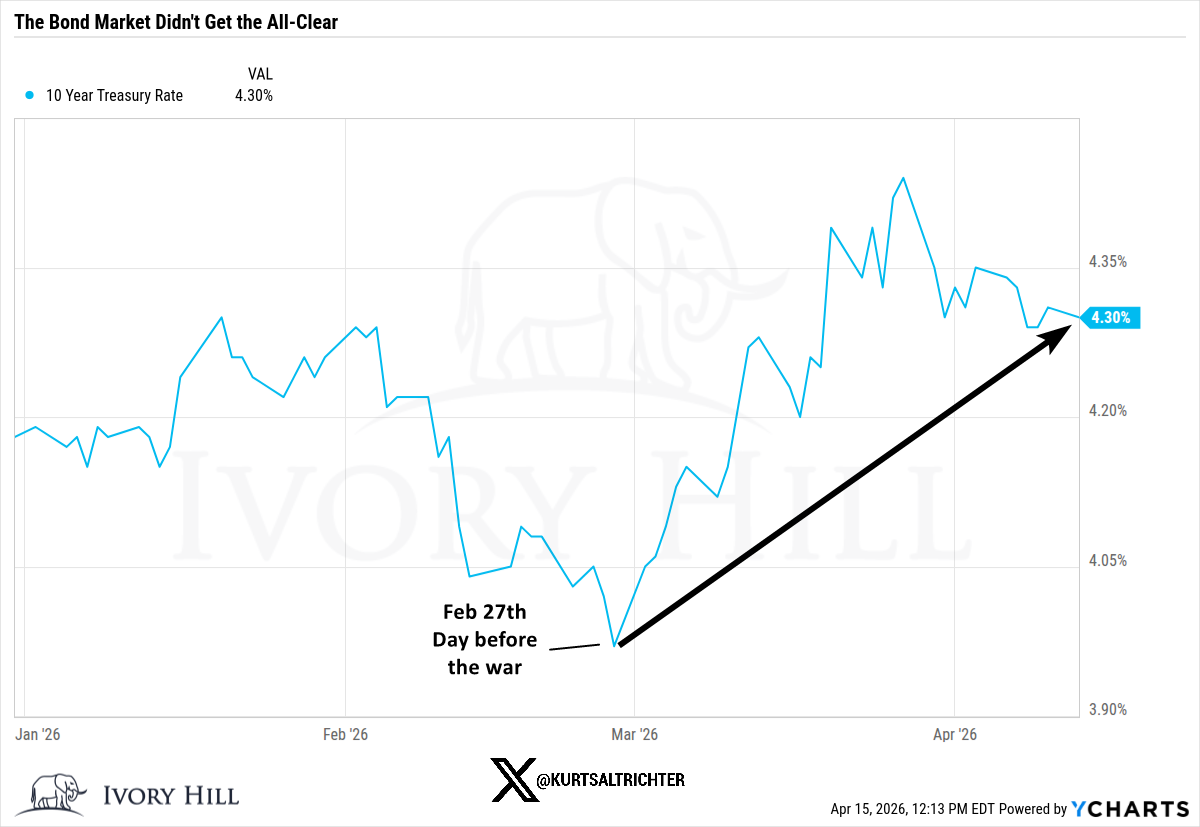

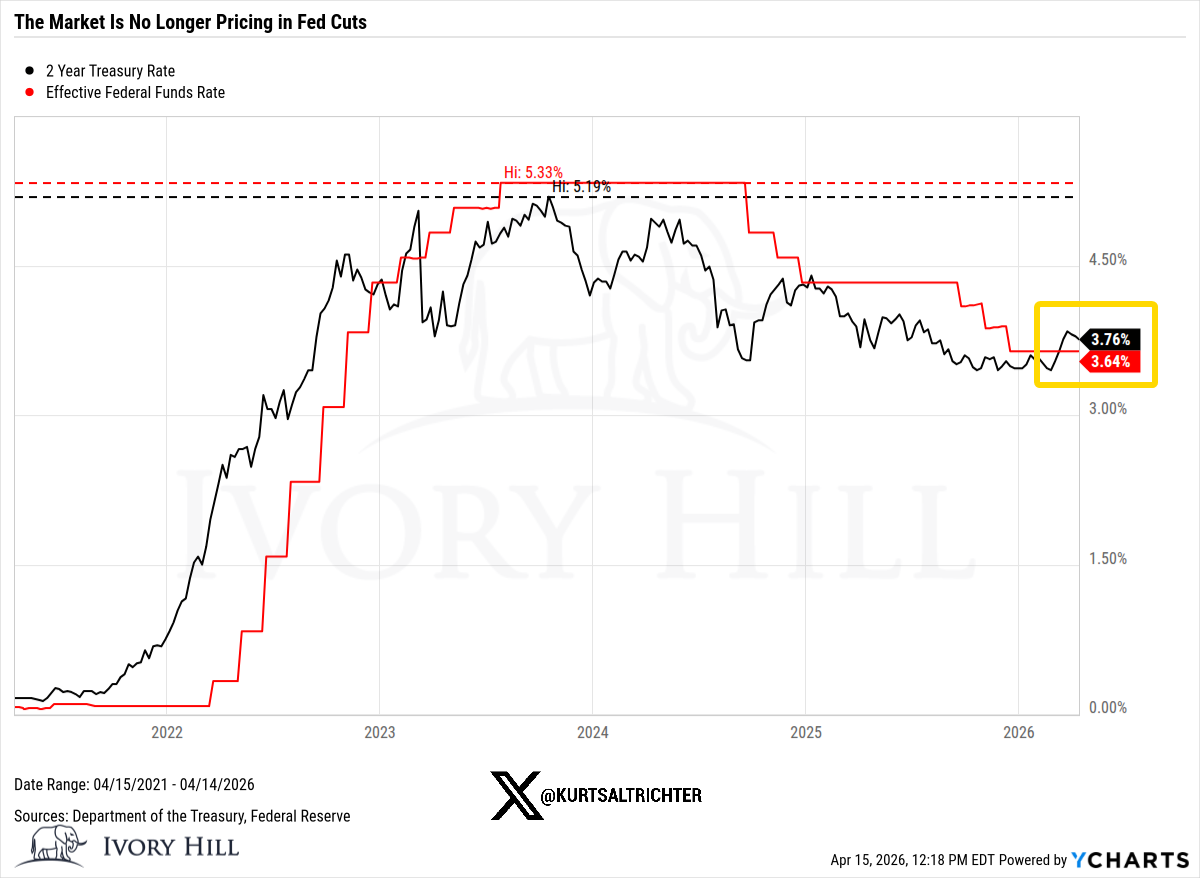

February 27. The day before the war. Here’s where things closed:

10-year Treasury yield: 3.95%. Yesterday it closed at 4.25%. That’s 30 basis points higher than pre-war.

WTI crude: $67.02. Oil is sitting roughly 37% above that level right now.

2-year Treasury yield: 3.38%. Yesterday it closed at 3.75%. That’s nearly 40 basis points higher than before any of this started.

Now, let’s work through what each of those actually means.

The 10-year yield doesn’t rise 30 basis points after a war starts because the bond market is feeling good about growth. Consumer sentiment is down. Confidence is weak. That move is the bond market pricing in inflation without making headlines. It’s saying higher oil is going to feed through into prices, and the Fed may not have as much flexibility as the equity market is assuming.

Oil up 37% in 6 weeks is not what a market looks like when it believes a real, lasting deal between the U.S. and Iran is coming. If traders were genuinely confident in a durable ceasefire, oil would already be back in the high $70s and moving lower. It isn't. It's still elevated, which means the oil market is not pricing in the same resolution stocks appear to be.

And the 2-year yield sitting 40 basis points above pre-war levels is a direct challenge to the Fed cut narrative. The 2-year is the most rate-sensitive instrument we have to look at. It tracks Fed expectations more closely than anything else. Right now, it's saying the Fed has less room than you think, and that matters for every valuation argument supporting this equity rally.

So who has it right?

Stocks could be right. I want to be fair about that. Bond yields could drop fast if we get a real ceasefire announcement. Oil could fall hard on any credible supply resolution. It wouldn’t be the first time equities led and everything else caught up.

But there’s another explanation that I think deserves more attention than it’s getting right now. A lot of this rally isn’t fundamentals-driven. It’s momentum-driven. Traders do not want to be short into strength. That kind of buying can keep a rally going for longer than it should, but it doesn’t change what’s underneath, and what’s underneath is still a market carrying elevated oil, rising yields, and a Fed with less room to cut than the bulls need.

Rallies driven by fundamentals tend to be more durable. Rallies driven by momentum tend to be weaker and more short-lived. The difference matters a lot when you’re deciding whether to add exposure near all-time highs. And as the market multiples chart shows above, stocks are priced for absolute perfection.

Where I actually stand

The situation has improved over the past 10 days. I’m not going to pretend otherwise, and I’m not in the business of being bearish for no reason.

But the gap between what stocks are priced at and what bonds and oil are priced at is something I am watching closely, and it has not closed. Stocks are at the optimistic end of the range right now. Bonds and oil are somewhere in the middle, still reflecting a world where inflation is a problem, the Fed has less room than people think, and the conflict isn't fully resolved. That gap has to close eventually, and it only closes one of two ways. Either we get a real ceasefire, oil falls back toward $70, and the Fed gets clear room to cut rates, and stocks turn out to be right. Or none of that happens, and stocks fall back down to where bonds and oil have been sitting this whole time. Right now bonds and oil are not moving toward stocks. It looks more like stocks have to come down to meet them.

The next inflation report drops on May 12th. If my estimates are right and CPI comes in north of 3.5%, the rate cut narrative is effectively dead for 2026.

If you’re adding exposure up here, you’re making a bet that everything breaks right. The war wraps up cleanly with no Trump Tape Bombs. Inflation stays contained. The Fed cuts on schedule. Earnings hold up. That’s four things that all have to go your way at once.

One real disappointment with any of them, and this market doesn’t have much cushion before the move lower gets fast and ugly.

I’d rather be patient here than chase something that two major asset classes are quietly telling me isn’t as solid as it looks.

If our long-term signal tells us to buy, then we will mechanically add more exposure.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.

Excellent article.

Bonds are the smarter money. When credit markets and equity markets diverge this sharply, the data historically favors the bond signal. Asset allocators who ignore that divergence tend to find out why it mattered after the fact.