The Fed’s Tightrope: Policy Mistake Incoming?

Why the Fed’s next move could ignite volatility, why September seasonality matters, and how we’re positioning with cash ready to deploy into small-caps and industrials.

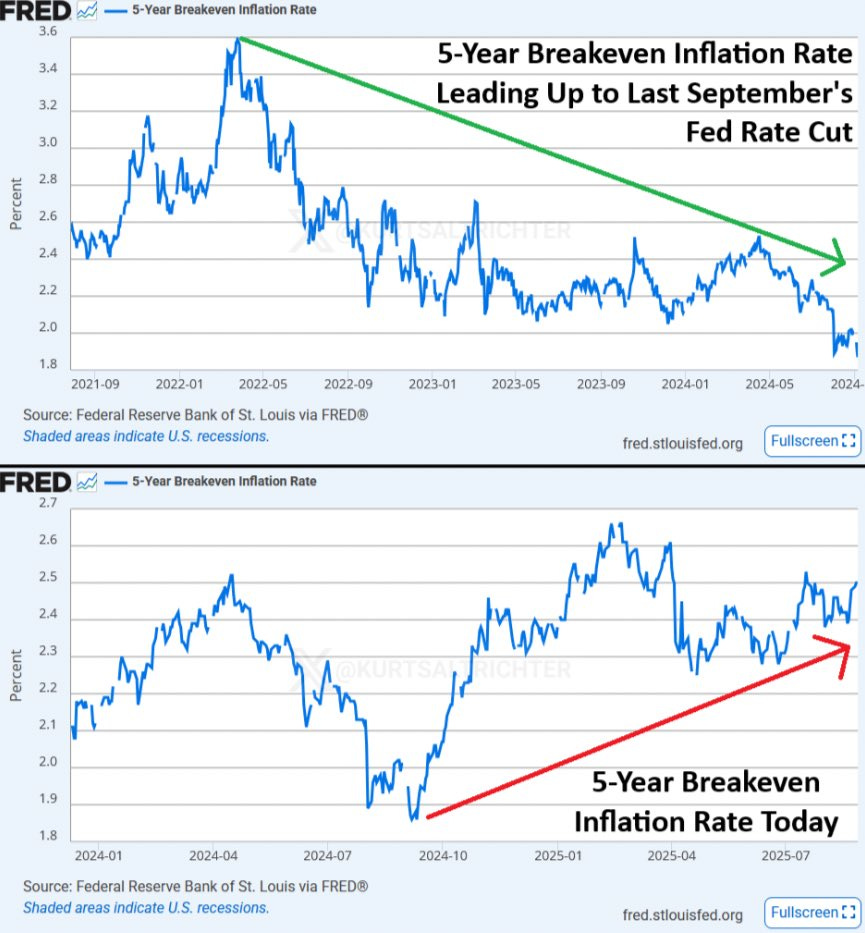

The Federal Reserve is standing on thin ice. Last fall, Powell cut rates as 5-year breakeven inflation trended lower. Fast forward to today, and those same breakevens are pressing back toward their highs, yet markets are still pricing in another cut.

This is where policy risk becomes real. If the Fed cuts again while inflation expectations are rising, they risk igniting 1970s-style runaway inflation. If they hold steady, the labor market could weaken further and push the economy into recession. Either way, the margin for error is razor-thin.

The bond market seems to be leaning toward the latter scenario, with the yield curve bull-steepening instead of twisting steeper, suggesting that investors see growth risks rather than runaway inflation as the primary threat. But that is a fragile equilibrium, and it can shift quickly.

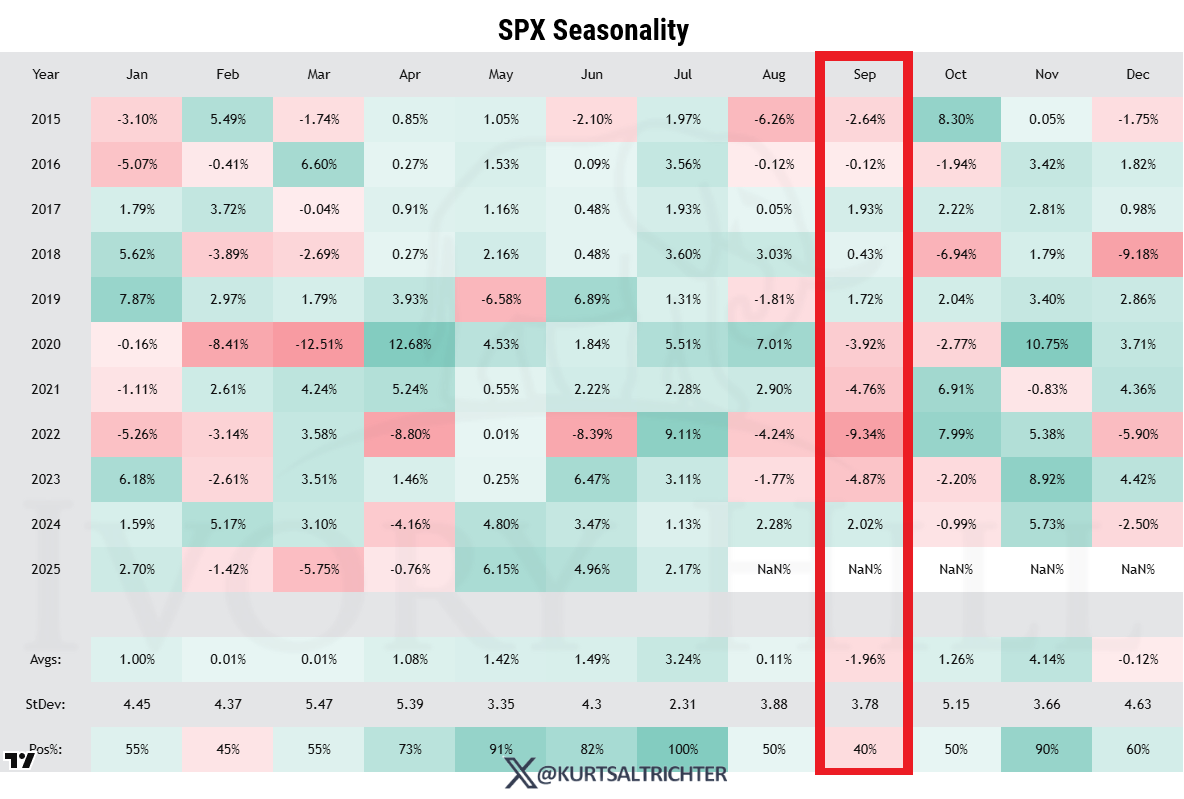

September Seasonality Is No Friend

Against this backdrop, seasonality is working against investors. Historically, September has been one of the weakest months for equities, and the data bears this out. Over the past decade, September has been red nearly 60% of the time. More importantly, it has often delivered outsized drawdowns relative to other months.

With equities sitting near all-time highs, the risk-reward balance favors patience. We do not lean on seasonality often, but when combined with current market positioning, the case for a tactical pullback grows stronger.

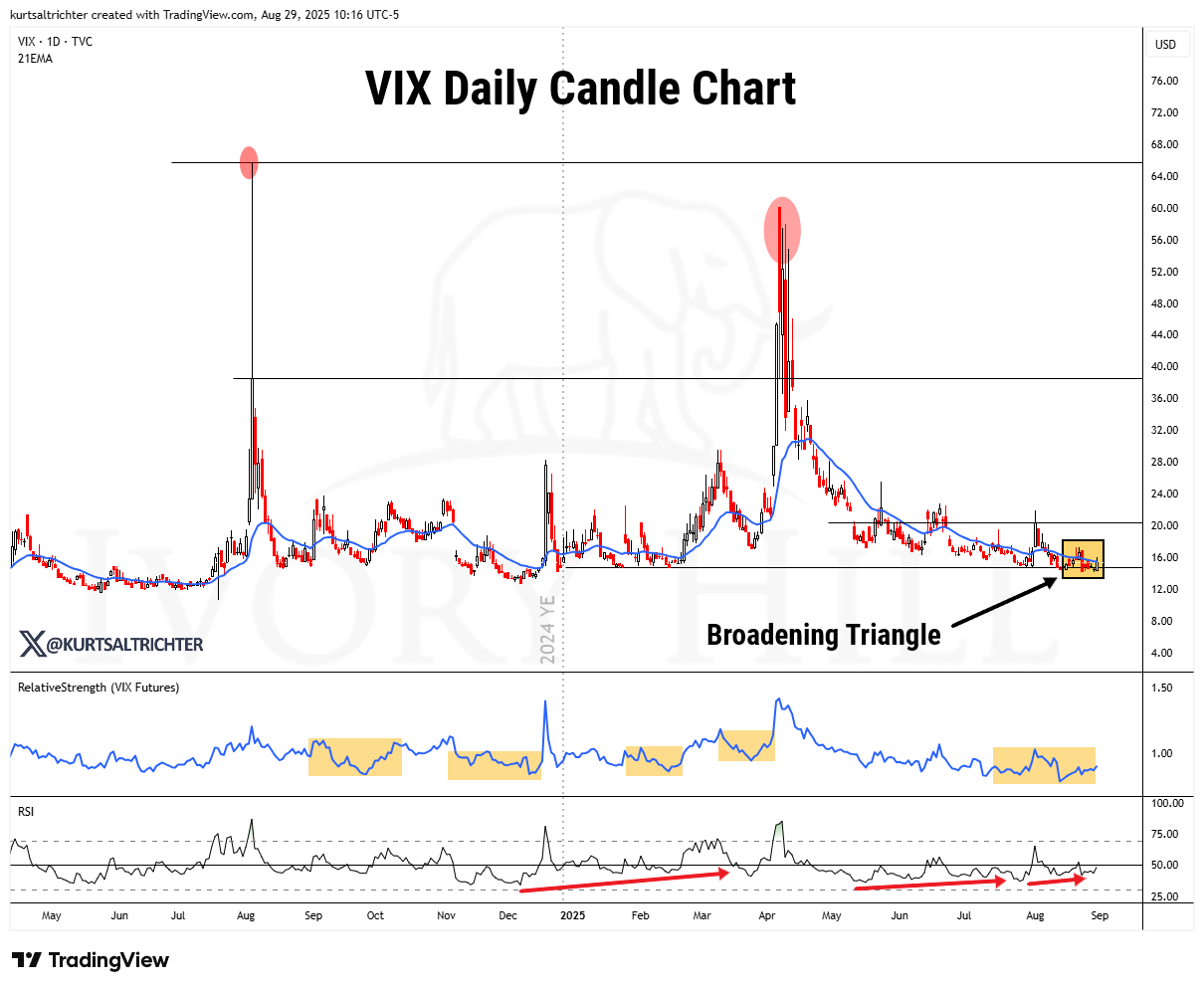

VIX: The Ball Underwater

Volatility is compressed. The VIX looks like a ball being held underwater, and history tells us that eventually, it pops. Right now, the broadening triangle pattern signals that pressure is building.

We took advantage of strong equity performance through the summer to trim high-beta and lock in profits. Today, we are sitting on roughly 15% cash, capital we plan to redeploy into high-quality opportunities if September delivers the kind of dip that seasonality and volatility structure suggest is possible.

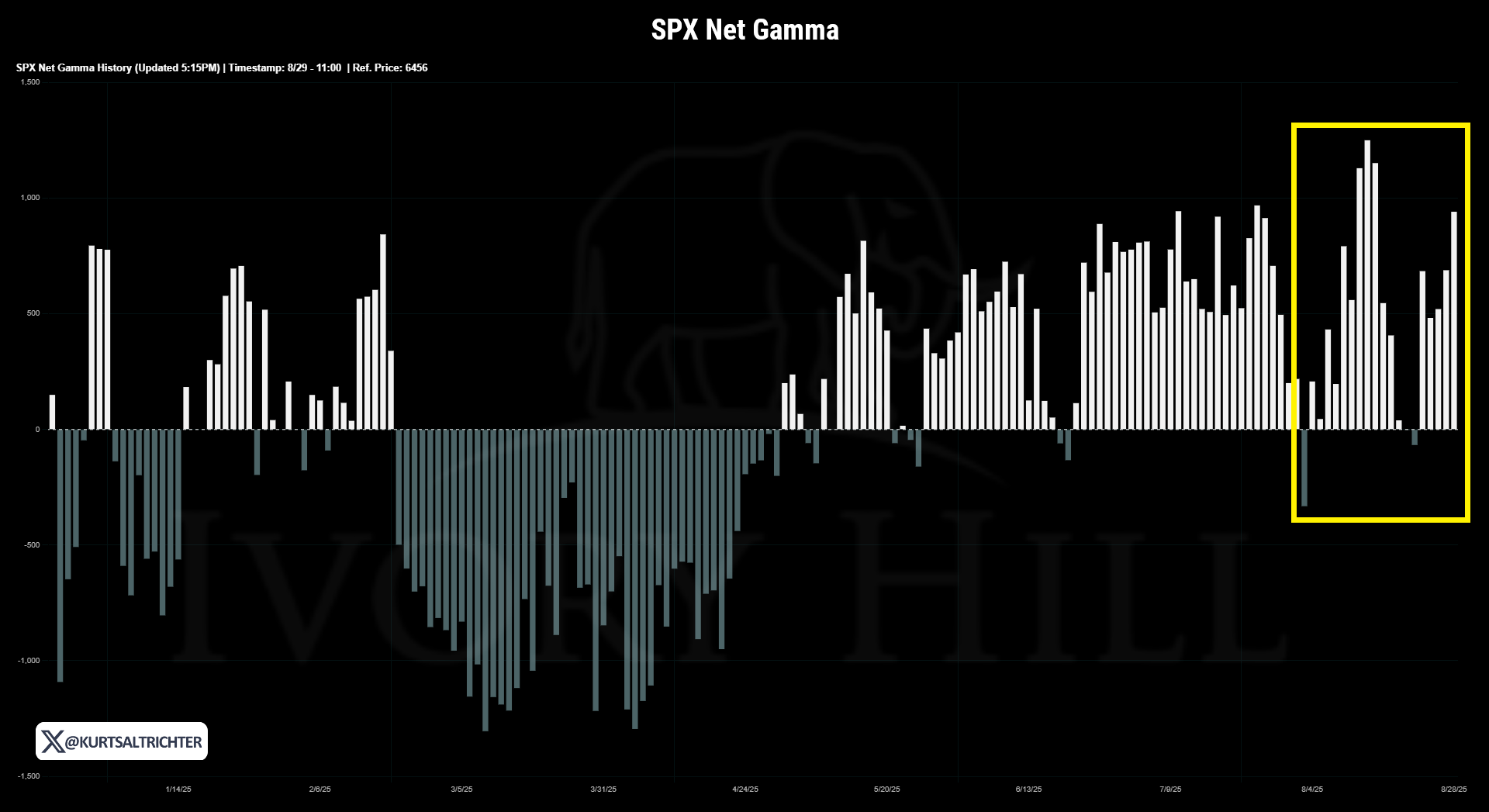

Dealer Gamma

Positioning in options markets is amplifying this setup. Dealers are back in positive gamma territory, meaning their hedging flows have been suppressing volatility. That helps explain why the VIX feels artificially calm despite risks building under the surface.

But here is the catch: once markets break below key levels, gamma can flip negative quickly, and dealer hedging turns from suppressing volatility to amplifying it. This transition is often the spark behind sharp downside moves, particularly when combined with weak seasonality and rising policy uncertainty.

Positioning for Opportunity

Our playbook is clear. If volatility spikes and equities pull back, we are looking to add exposure in two key areas: small-caps and industrials.

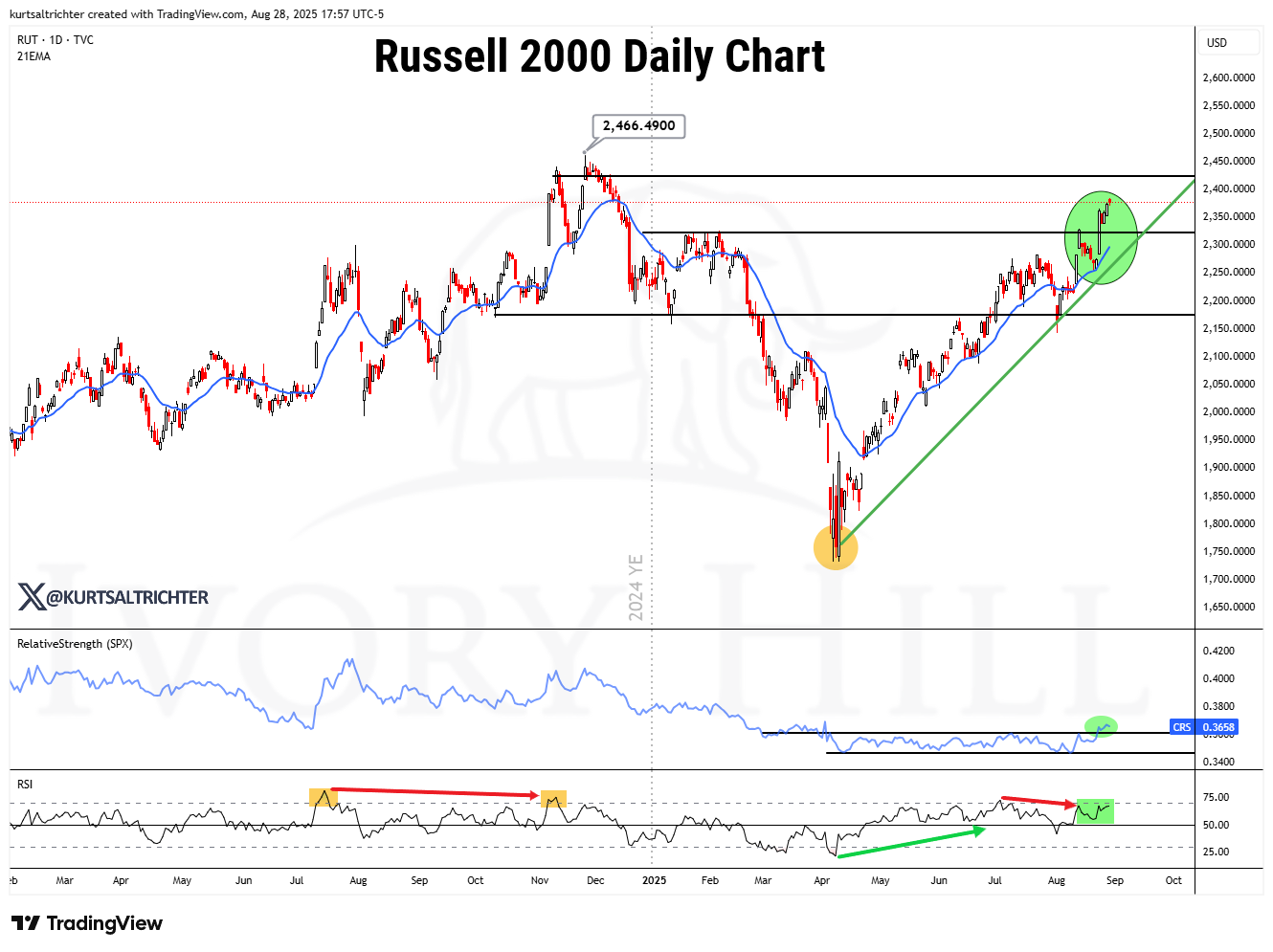

Small-caps have broken out of their spring lows with strong relative strength versus the S&P 500. The Russell 2000 chart shows constructive momentum, supported by rising RSI and relative strength. We also own ARKK.

Industrials (XLI) are consolidating in a bullish range near highs, with relative strength ticking upward and RSI holding above 50. Both setups offer attractive entry points if weakness materializes.

The Bigger Picture: S&P 500 Valuations and Trend

Valuations remain stretched, with the S&P 500 trading around 21.25x earnings. A better scenario assumes EPS growth toward $300, which could justify 6,600 on the index, while a worse scenario sees EPS slip to $275, taking the S&P down toward 4,813.

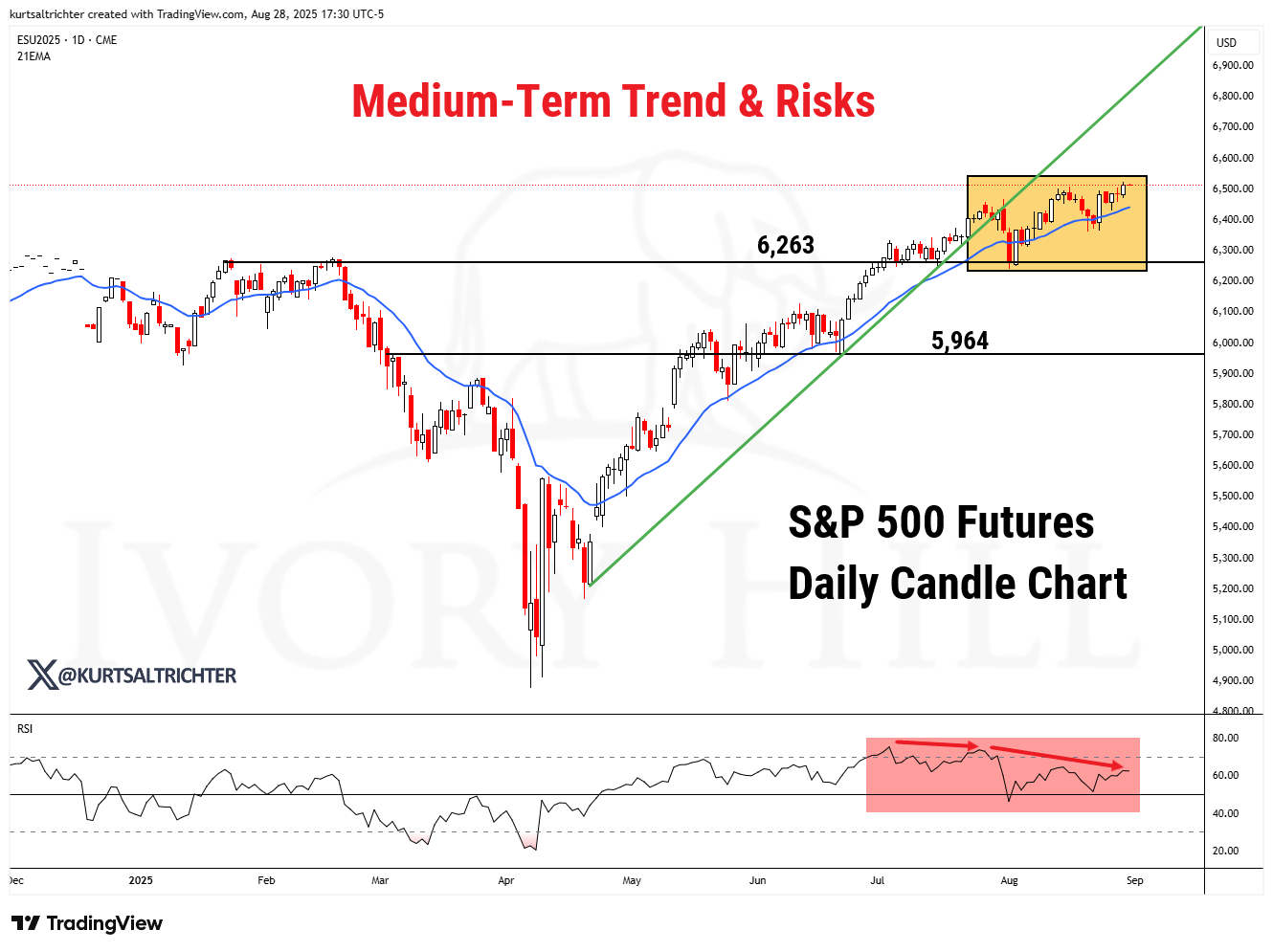

Technicals echo this pressure. S&P 500 futures remain in an uptrend, but momentum is waning. RSI has been diverging negatively, a signal that strength is thinning beneath the surface.

Where We Stand

We are not afraid of this market, but we are also not complacent. By trimming into strength and raising cash, we have given ourselves optionality. If September plays out as it often does, with weakness and rising volatility, we will be ready to step in and selectively add exposure to areas of leadership into year end.

Remember, the real game is not about September alone. Every move we make is about where markets will be in Q1 2026. That perspective keeps us disciplined, patient, and ready to take advantage of opportunity when others are shaken out by short-term noise.

And remember - The one fact pertaining to all conditions is that they will change.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President