The Nasdaq Went Full Top Gun

70 Degrees, 28%, 42 Days. This Doesn't End With a Smooth Landing.

The uptrend is intact. Pullbacks are buyable.

The market is overbought and a pullback is coming. Patience here is not a bad idea. Our S&P 500 target of 7,700 is close.

The S&P 500, Nasdaq, and Russell 2000 all pushed to fresh record highs this week. Crude fell below $100 on U.S.-Iran deal hopes before bouncing hard off Thursday’s lows near $90. Chips and AI names led again but took real hits Thursday while software staged a comeback. Treasury yields finished the week higher after a choppy ride in both directions.

The Nasdaq 100 trend line since March 30th is sitting at 70 degrees. That is not a typo. Up 28% in 42 days. The only other thing I can think of that moves at 70 degrees is a Navy fighter pilot leaving a carrier deck in an F/A-18. At some point, this thing has to come back to earth. Literally.

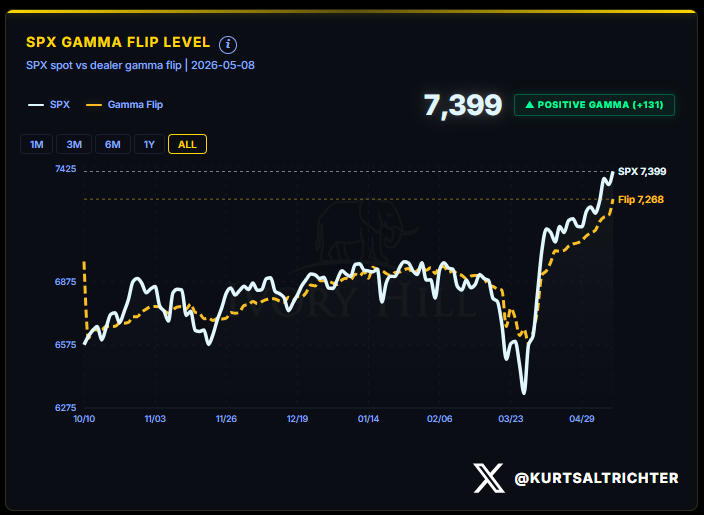

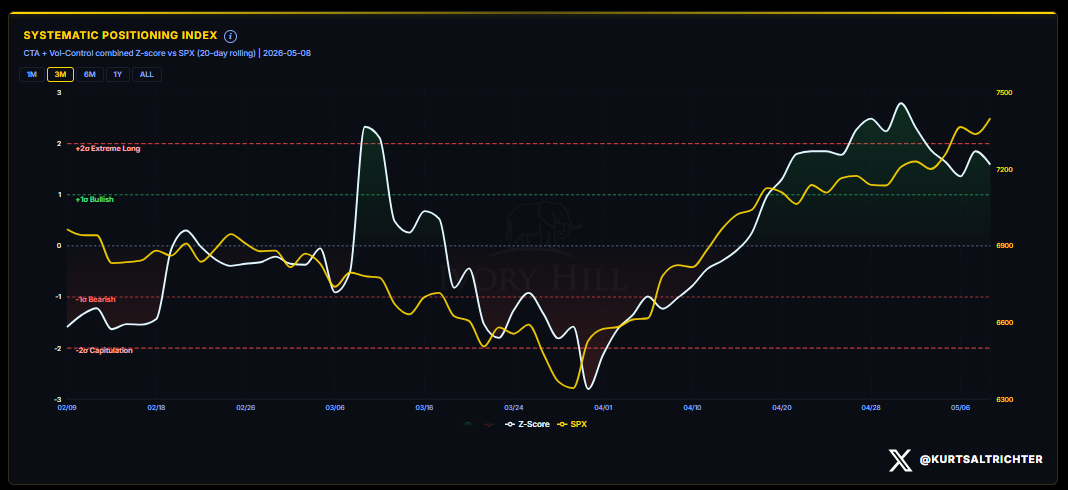

Systematic flows are paused and tilted slightly to the downside. But dealers are still in positive gamma, and that limits how far any selling can run. There is no obvious air pocket here as long as that holds.

The wildcard is the weekend. A few #TrumpTapeBombs would change this setup fast.

My base case is that if this market is going to let some air out, it will happen in the next week or so, and most likely following next week’s options expiration. Once front-month gamma rolls off, volatility has more room to move. That is when the setup gets interesting. The CPI report could also be the start of a volatility spike.

For now, on positioning alone, a significant drawdown is not my base case.

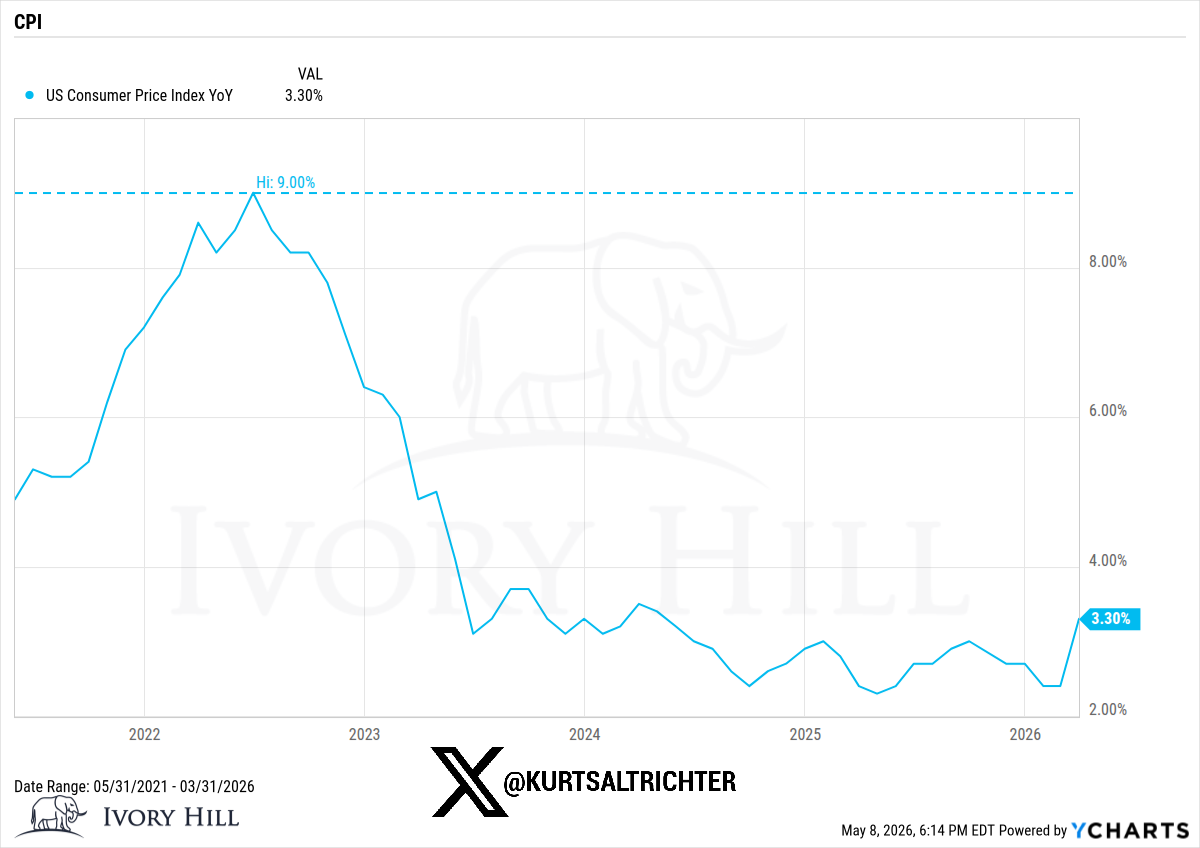

April CPI drops Tuesday, May 12 at 8:30 a.m. ET.

The last read was March CPI at 3.3% year-over-year, with a big 0.9% month-over-month jump driven almost entirely by a 21.2% spike in gasoline prices.

For April, the setup is more complicated. The U.S.-Iran ceasefire sent Brent crude down roughly 22% in early April, which a lot of people think will logically pull headline lower. But offsetting that, airfares were running up 10-15% for April-May travel, and used vehicle prices jumped 6.2% year-over-year on the Manheim index as the auto tariff pushed buyers out of new cars and into the used market.

The market consensus has shifted toward a 3.0%-3.5% year-over-year range for April CPI, with the prior consensus of 2.8% largely abandoned after the energy and geopolitical repricing earlier this spring.

I think the market is completely wrong on this month’s CPI print. I think 3.5% is the floor, and the high end of the range is closer to 3.80%, so my base case would be ~3.65% year-over-year on the headline.

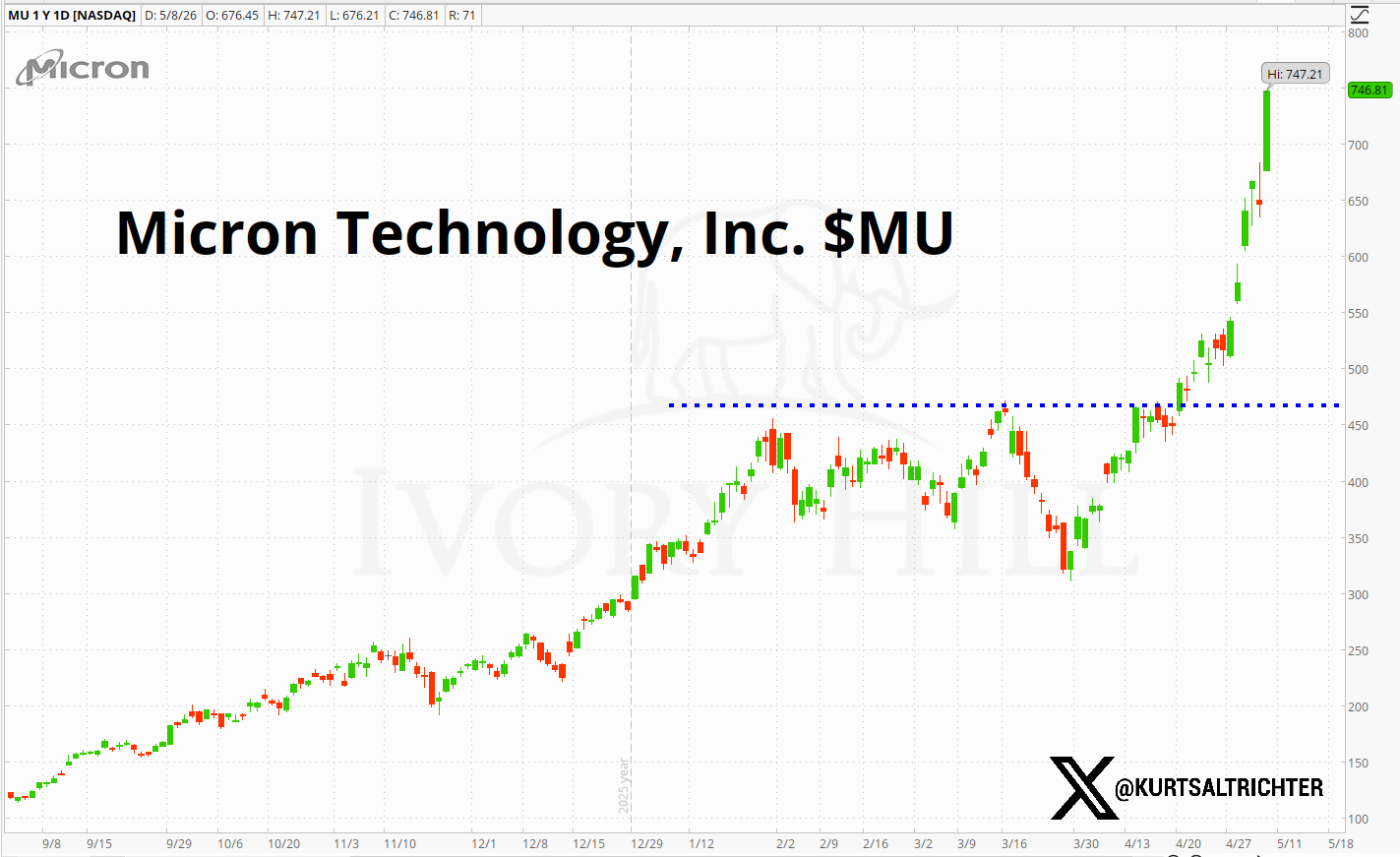

Micron MU 0.00%↑ is breaking out, and I think this stock is still deeply undervalued here. You’re getting 190% YoY revenue growth and 57% net margins at 11x forward P/E. That’s a mispricing. Fully committed 2026 HBM capacity and leadership in SOCAMM2 and HBM4 put Micron at the center of structural AI memory demand, and the multiple has no business being this low.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.