Tune Out the Noise. Two Things Actually Matter.

Real earnings are holding up a 22X market. That's the good news, and why there's no cushion left.

The noise is deafening right now. Iran is flaring back up. AI capex is suddenly in question, and the memory names are getting torched. The dollar is ripping on a Fed that won’t cut, which is dragging the yen to the floor and putting the whole carry trade back on watch for an unwind. Pick any one of these, and it can hijack a whole week.

But does any of it really matter right now?

You know I lean into technicals and quant signals, and I watch flows more closely than most. That is my wheelhouse. When the tape gets this loud, though, I find it valuable to take five big steps back and look at plain, boring fundamentals.

Earnings backfilled the rally

July’s Market Multiple increased, and for once, it did so for the right reason. Earnings did all the work. But the setup that got us here leaves absolutely no cushion. Everything now hinges on two variables, and both have to keep moving in the right direction.

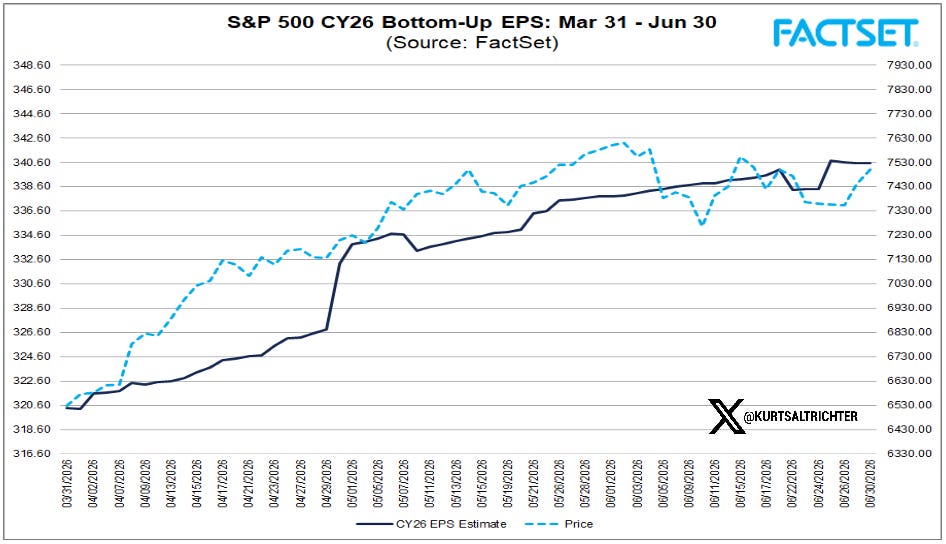

The bigger of July’s two changes runs through earnings. FactSet’s 2026 S&P 500 consensus jumped again after May results, from $320 to $340 a share. That’s a long way from the $305-$310 the Street penciled in at the start of the year. Aren’t Wall Street predictions so helpful? Not. So the market sits near 22X forward earnings. That’s a rich number, and the underlying earnings growth is keeping it honest.

Why does this matter? AI data center demand is pushing earnings expectations up quickly, and those higher numbers are backfilling the valuation gains. Higher estimates absorbed the run-up, so the multiple held roughly flat while the index climbed. That happened again last month.

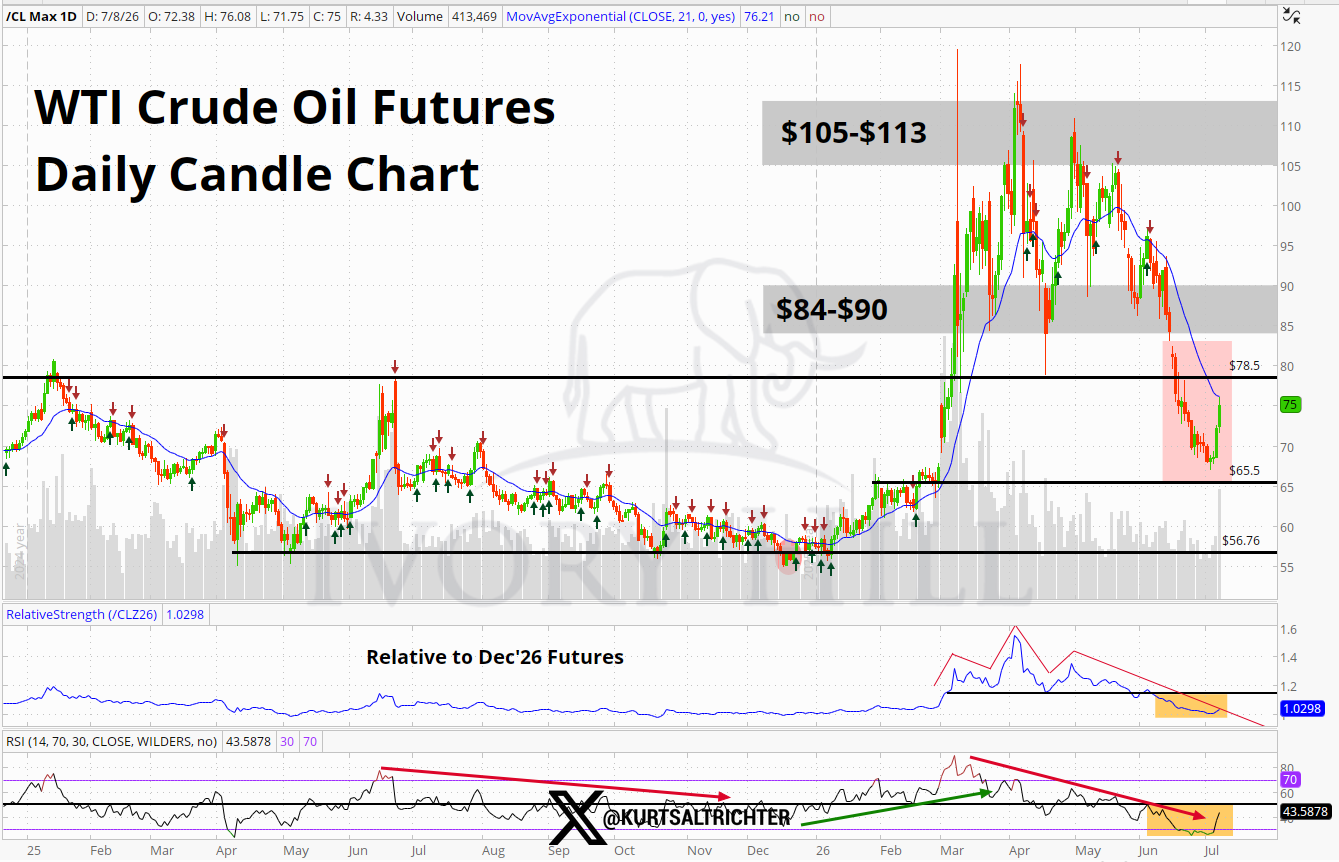

The second change. Geopolitics came off the board as a market influence. Oil fell back to, or just under, pre-war levels, which tells you investors have stopped pricing a reescalation out of Iran or Ukraine. Remember, Ukraine? With oil lower, the tape has narrowed its focus to the two influences that actually drive it right now.

Two influences, and no room to be wrong on either

AI and data center spending is first because it drives both economic and earnings growth. Inflation and rate-hike expectations are second, because a Fed hiking cycle is one of the few events that can pull the multiple lower on its own.

The news on both came in mixed, which is exactly enough to hold a stretched market in place and nothing more.

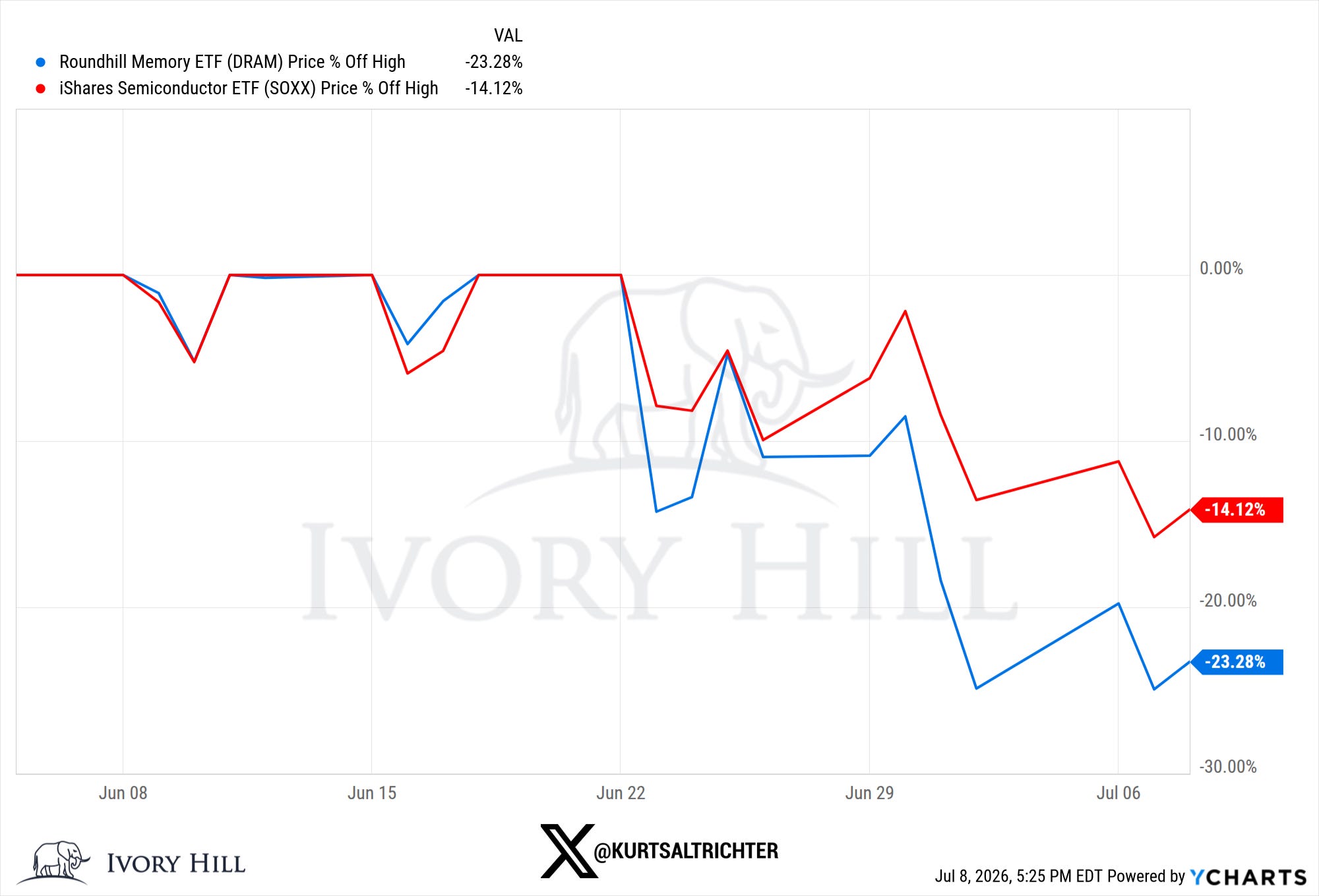

On the AI side, the infrastructure names fell in June, with memory and semis leading the drop. Nothing foundational broke. Every major player reaffirmed its buildout intentions, and the selloff looks like profit-taking after an unsustainable run. As long as spending intentions hold, treat the dip as consolidation inside a rising market. This is essentially a privately funded economic stimulus package.

On inflation, the news was skewed positive. The Warsh Fed carried a more hawkish tone than the market is used to, but it held rates steady, and Warsh himself sounded measured at the ECB’s Sintra conference. Some leading inflation indicators rolled over from last month’s peak, which aligns with the idea that lower oil prices take pressure off prices.

Add it up, and you get a market positive enough to hold a historically high multiple, and stretched enough that a bad surprise on both influences at once could take 5% to 10% out fast. That’s what a market does when it prices perfection and gets handed less.

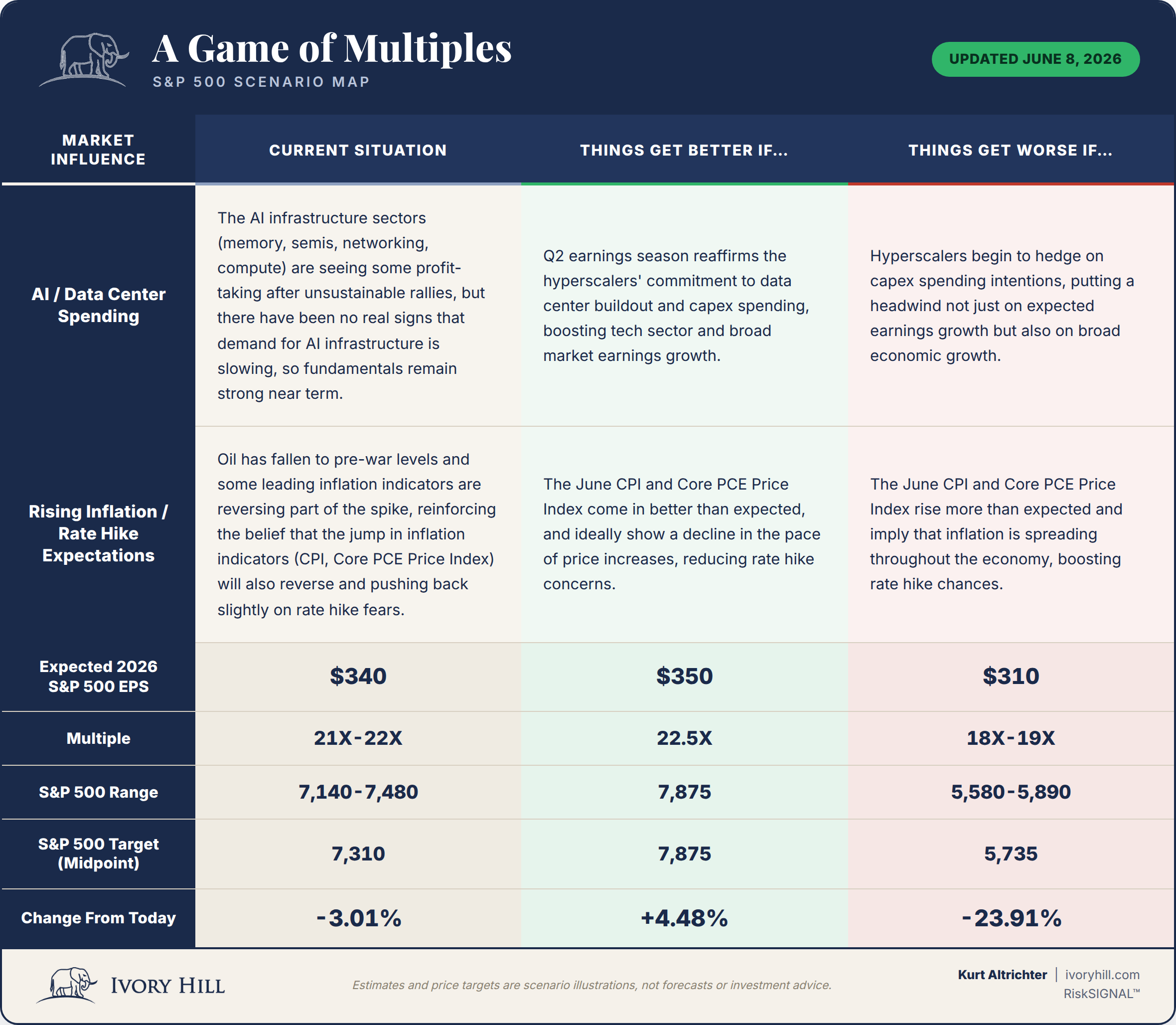

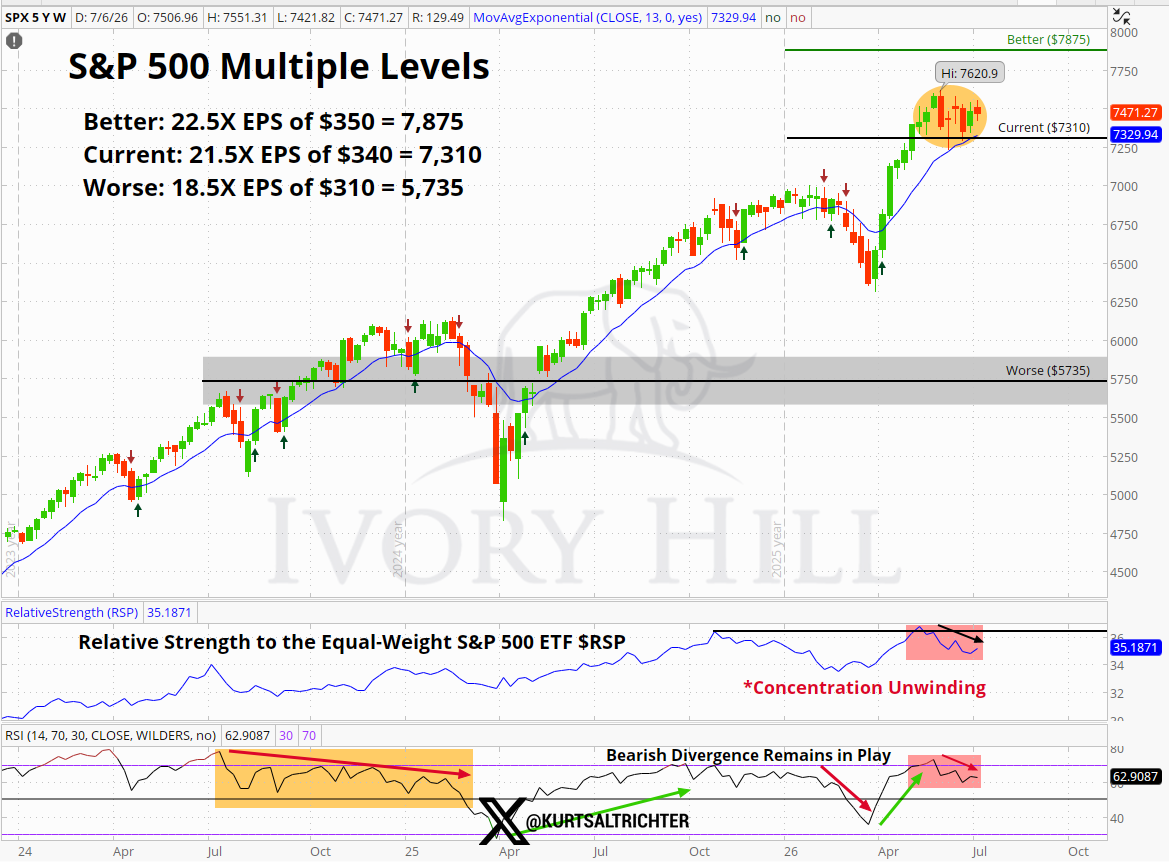

The three scenarios and where they sit on the chart

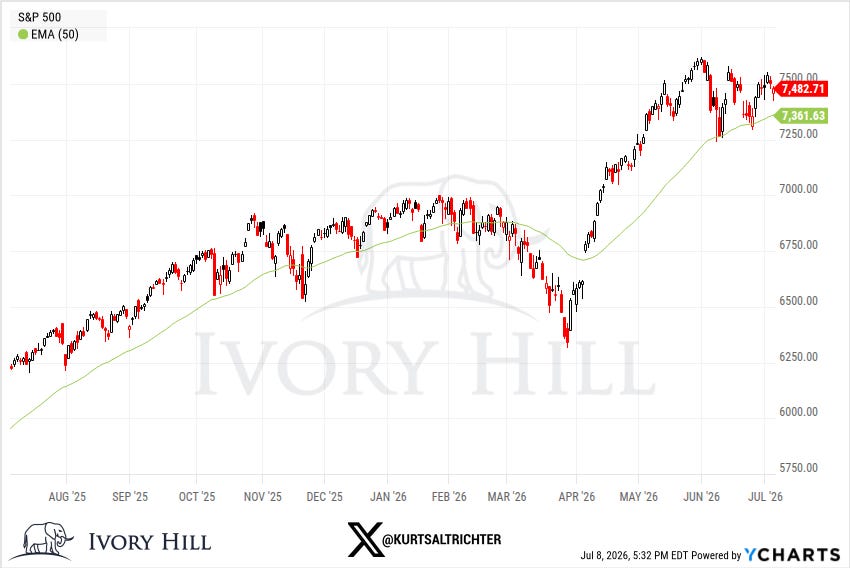

All three targets moved up this month, and every bit of that came from higher earnings. The multiples held steady. The S&P opened the week within 20 points of the current-situation upper bound at 7,480 and has traded sideways just above it since.

Current Situation. Data center spending is holding up earnings and growth. Inflation is still high, though lower oil and softening price indicators hint that the pressure is easing. One hike this year is about the ceiling here. At $340 in EPS and a 21X to 22X multiple, that’s a range of 7,140 to 7,480, with a midpoint of 7,310, up 6.3% from June. The midpoint is the level that matters. It lines up with the summer support that’s held through every dip, and the 13-week moving average sits right on top of it just under 7,325. The Fed is not going to raise rates in 2026. Inflation is about to print downwards over the next two months.

Better If. Q2 earnings reaffirm the growth path, and inflation metrics have fallen enough to ease fears of a hike. More of a good thing. On $350 in EPS and a 22.5X multiple, the target is 7,875, a fresh record and up 3% from June. There’s no price history up there yet, though two separate measured moves off recent pullbacks split the difference within 10 points of that number. If stocks stabilize and push back to the highs, 7,875 comes into play, and 8,000 stops look ambitious.

Worse If. AI spending intentions start getting cut, which hits earnings and growth at the same time, and inflation refuses to recede. This reverses the exact reasons stocks have rallied since April and drives the multiple toward 20 and below. On $310 in EPS and an 18X to 19X multiple, the range is 5,580 to 5,890, midpoint 5,735. That zone has the deepest price memory on the chart, running straight through the middle of the H1 2025 trade, so it should catch a real selloff. Lose it, and a downside measured move points at an even 5,000.

The multiple is high because the earnings are supportive for now. That’s the good news. It’s also the entire problem. 22X, prices zero disappointment, and this rally is now leaning on only two influences that both have to keep cooperating. I’m not short this market. I’m not going to overpay for it either.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.