Turn Off the News. Panic is Not an Investment Strategy

A no-nonsense breakdown of every major market worry right now, and what I think you should do about it.

The Ivory Hill RiskSIGNAL™ remains green. If that changes, we reduce risk, but we do not make investment decisions based on how we or anyone else feels, because markets do not care about your feelings, period. And if the trend does shift, I do not think it will take long to reverse. My 2026 target for the S&P 500 remains 7,700 by year-end, roughly a 16% return from yesterday’s close.

Markets pulled back again this week, and emotions are running hot. I fielded more client calls this week than usual, all asking some version of the same question: what is going on with everything going on? In my experience, for every one client who picks up the phone, there are ten more thinking the same thing. So this week’s note is dedicated entirely to answering those client questions.

There is a lot of noise right now. War in the Middle East. Oil spiking. Stagflation warnings. Is the Fed possibly hiking rates? Private credit is blowing up. AI trade is unraveling just as AI is proving itself. The stock market hit new year-to-date lows yesterday.

Most of what you are reading in the news is either incomplete, late, or engineered to keep you coming back for more stress. I know this from personal experience. Every time I post a high-conviction take on X, my engagement goes through the roof (like 20-50X) compared to a more thoughtful post. The news works the same way as your social media feed. They need eyeballs, and extreme headlines, whether wildly bullish or wildly bearish, get clicks. The sky is always falling somewhere. That drives advertiser dollars. Said another way, reporting the facts clearly and concisely does not make the network’s money because you won’t watch it.

Most people still treat mainstream news like it’s some sacred institution dedicated to truth. It’s not.

Believe it or not, my younger clients in their 20s-30s filter through the noise significantly better than my clients who are in their 50-60s. Because they don’t watch the news. They get their news from Substack, social media, and independent research.

CNN is owned by Warner Bros. Discovery, the same company behind the Bachelor franchise. NBC News is a division of Comcast’s NBCUniversal, a corporation that makes its real money from theme parks and streaming subscriptions. ABC News belongs to The Walt Disney Company, a business built on fairy tales and the Backelor franchise. Fox News operates under Fox Corporation, which also runs Fox Entertainment. These aren’t journalism companies with entertainment side hustles. They’re entertainment conglomerates with news divisions bolted on because outrage and fear generate reliable ratings. In financial markets, every single one of these parent companies is classified under “Communication Services” or “Media & Entertainment,” not under some special journalism category, because no such category exists. The FCC’s Fairness Doctrine, the one regulatory guardrail that once required broadcasters to present issues honestly and with balance, was killed in 1987, and nothing replaced it. Cable news was never subject to it in the first place. So when you watch a primetime news anchor work a story into an emotional frenzy, understand that you’re not watching journalism. You’re watching a product, designed by an entertainment company, engineered to keep you glued to the screen long enough to sell you a pharmaceutical ad. The sooner people internalize that reality, the sooner they’ll start thinking for themselves instead of outsourcing their opinions to a teleprompter reader in a $3,000 suit and $500 haircut.

So the incentive is never to give you the full picture. It is to give you the most alarming version of it, as fast as possible.

One more thought on the CNBC FOMO factory.

I genuinely cannot believe people who call themselves serious investors take anything on that network at face value. If you spend five minutes actually listening and doing basic research, the conclusion is obvious: it's a TV show. That's it. Just like Landman and Everybody Loves Raymond. The difference is, you're actually better off watching those shows, because at least you won't emotionally react your way into an irreversible financial mistake.

Take The Halftime Report on CNBC. Every single day, Josh Brown from Ritholtz Wealth Management sits down and drops a new stock pick. Fresh conviction. Fresh enthusiasm. New ticker, new story. And then tomorrow, a new one. He does this 252 days a year.

Josh Brown runs a $4B+ RIA. Client assets pour through the door every week, and the credibility that drives new business to his firm is manufactured directly by his daily appearances on CNBC. He is being positioned as an elite stock picker, a market authority, a guy you should listen to. But nobody is keeping score. There is no win/loss ratio. No batting average. No scoreboard. He and the other talking heads say “I like this stock” on national television, and it disappears into the air. No follow-up. No accountability. You could pull SpongeBob SquarePants out of Bikini Bottom, sit him behind that desk, and the segment runs the same way. “I’m bullish on Krabby Patties.” Brilliant call, Sponge. Same conviction, same follow-up, same accountability. Absolutely none.

That is professional and intellectual dishonesty. Because the average investor watching at home has no idea that’s how the game works.

And here’s the part that should really convince you: last time I checked, Josh Brown’s firm doesn’t even use individual stocks in their model portfolios. They use ETFs and mutual funds. The guy who built a national reputation as a stock picker doesn’t run stocks in his own client book. How stupid is that?

So you have someone pumping individual names on television every day to millions of viewers, collecting the credibility that comes with it, growing a $4 billion business off that credibility, and not even using those ideas himself. Connect those dots however you want.

Bottom line: CNBC is a joke. And sadly, most of the free institutional research is as well. Build your own framework, do your own research, or pay someone you trust and read their research. I am happy to make recommendations.

Here is my actual read on every major worry in the market right now, in plain language.

Worry #1: The U.S.-Iran War Is Going to Crash the Market

Maybe. But probably not the way you think, and I want to push back on some of the fear being generated around this.

The war itself is not what matters to your portfolio. What matters is one body of water: the Strait of Hormuz. That chokepoint carries roughly 20% of global daily oil consumption. It is effectively shut right now. That is why oil went from $60/bbl in early 2026 to a high of $120 this week before pulling back to around $94 today.

If the Strait reopens, this selloff reverses fast and hard. If it stays closed for another 30 days, we test the November lows on the S&P 500 around 6,534. That is it. That is the whole equation. Everything else, the missiles, the rhetoric, Trump’s press conferences, Iran’s new Supreme Leader, is noise unless it directly affects oil moving through that Strait.

I want to be direct about something. I believe the conflict in the Middle East should be seen more as a buying opportunity than as a reason to run for the hills. Some are drawing comparisons to the Iraq war in 2003 or Russia’s invasion of Ukraine in 2022, suggesting this could drag on for years rather than weeks. That comparison adds real weight to the uncertainty, and I get it. The mind hates not knowing the outcome. We want immediate resolution, especially in a world where we expect answers in seconds.

But think back to the Iraq war. Markets moved sharply at times. Oil prices spiked. There were stretches of deep uncertainty. Yet over the full span of that conflict, the U.S. economy continued to grow. Businesses continued to operate. Long-term investors who stayed disciplined were not destroyed. The same dynamic played out when Russia invaded Ukraine in 2022. Oil spiked above $130, markets sold off hard, and investors who panicked locked in losses right before the recovery.

History is not a guarantee. But it is data, and the data says that geopolitical conflicts, even prolonged ones, rarely end bull markets on their own.

The market has also been playing a pattern called TACO, Trump Always Chickens Out, where every scary geopolitical headline eventually gets walked back, and stocks bounce. It has worked reliably for the past year. The problem this time is that war is not a domestic policy you can reverse with a social media post. Even a U.S. ceasefire does not guarantee that Iranian factions will stop harassing tankers.

There is another factor worth naming directly: unpredictability. The Trump administration has shown repeatedly that tone and policy can change in literally five seconds. None of this should be a surprise. That back-and-forth feels destabilizing in the moment. But it also means that any legitimate good news, a ceasefire signal, a credible Strait reopening, even a softer presidential comment, should send stocks sharply higher and oil sharply lower. The same volatility that is hurting you on the way down will work in your favor on the way up. If you are holding an oil trade, move your stops up. This can unwind just as fast as it was built.

My read: a ceasefire likely brings oil back to $70-75, not $60. Stocks rally hard on that news, but probably do not make new highs immediately. The more dangerous scenario is oil holding above $90 for another month, which starts to do real economic damage.

Worry #2: Stagflation Is Back, and It Is Going to Be the 1970s Again

This one is real, but it is not inevitable, and most people explaining it do not actually understand what makes stagflation dangerous.

Stagflation is not just “inflation is high.” It is inflation running hot while growth is stalling at the same time. The reason it destroys portfolios is that it removes the hedge. Normally, when stocks fall, bonds rally because growth slows and the Fed cuts rates. In stagflation, both fall together. There is nowhere to hide in a traditional 60/40 portfolio. We saw this in 2022. Stocks fell 30% while 20-year Treasuries fell 40%. No offset. No relief. Just losses on both sides of the portfolio simultaneously. This is where hiding in cash makes sense. Not yet, though.

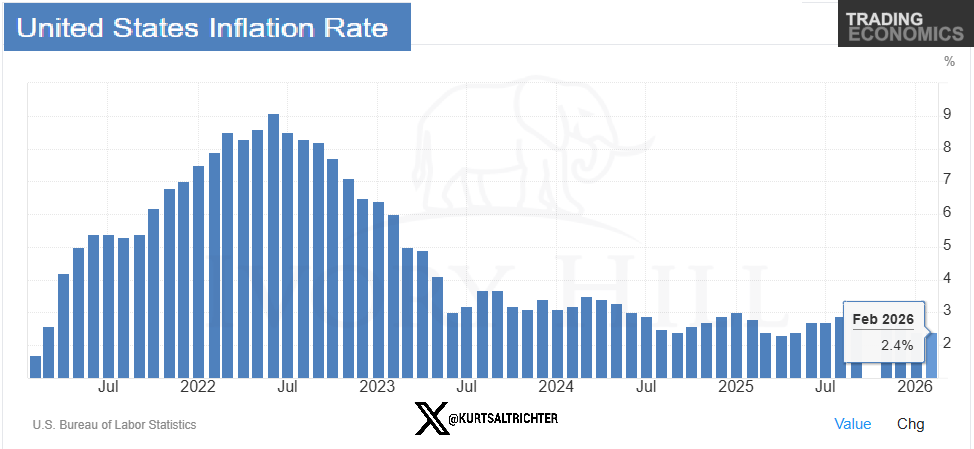

Here is where we actually stand today. On the growth side, February payrolls came in at -92K versus an expectation of +60K. Unemployment rose to 4.4%. Continuing claims jumped 46K in a single week. On the inflation side, Core PCE is at 3.0%, the highest since April 2024, and that is before a single barrel of $90+ oil shows up in the data. The March inflation numbers will not be released until mid-April, and they will be ugly. I expect an acceleration in headline inflation to +2.85% y/y, and it could push closer to 3%.

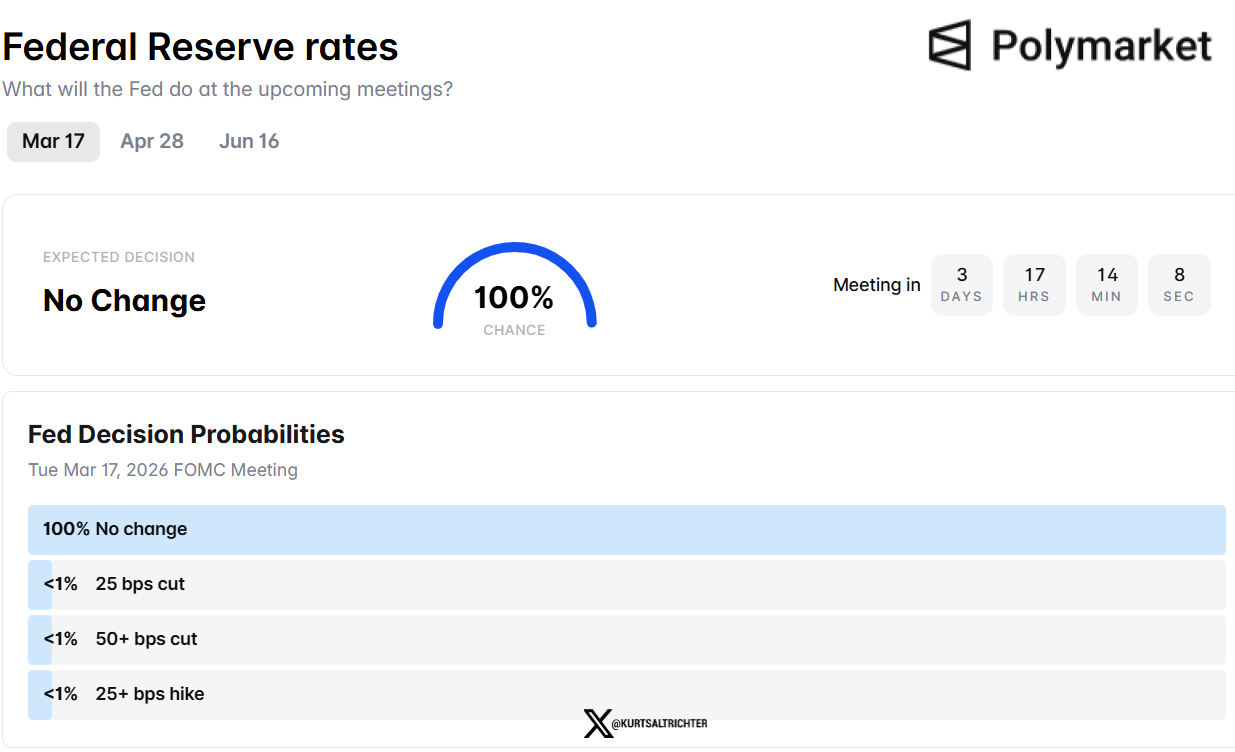

The Fed is now paralyzed again. The market went from pricing in three rate cuts this year to pricing in zero in a matter of weeks. Today, the odds of even one cut in 2026 fell below 100%. Rate hikes are now being discussed, and the rumors are spreading. The ECB and Bank of England are already pricing them in.

But here is what I want you to understand: one bad jobs report is not a trend. The ISM Services Index hit a multi-year high of 56.1 in early March. ADP showed +63K private payrolls the same week. Initial jobless claims were solid. The economy is not in recession. The stagflation risk is real and rising, but it is not confirmed. If March payrolls also come in negative, the calculus changes completely and this becomes my base case. Until then it is an elevated risk, not a certainty.

Worry #3: The Fed Is Going to Hike Rates and Destroy Everything

This is the newest and most alarming headline making the rounds, and I want to address it directly because it is being badly mischaracterized.

Yes, rate hike expectations are being discussed in markets for the first time in years. Yes, the 2-year Treasury yield spiked to a seven-month high of 3.75% yesterday. Yes, the bond market is pricing in a harder Fed path. But here is the context that is getting lost: the Fed does not hike into a weakening labor market. Full stop. That would be an extraordinary and historically unprecedented policy error. What the bond market is actually pricing is that cuts are off the table for now, not that hikes are coming.

The real risk is a Fed that is frozen, unable to cut because inflation is rising from oil, and unable to hike because the labor market is showing cracks. That paralysis is itself a headwind for stocks because it removes the safety net that investors have relied on for the better part of two years. The Fed cannot ride to the rescue this time. That changes the risk calculus even if hikes never actually materialize.

Worry #4: Private Credit Is Going to Blow Up the Financial System

This one is being dramatically underreported, and I think that is actually more concerning than if it were getting the coverage it deserves.

Blue Owl has stopped redemptions on one of its private credit funds. JPMorgan is writing down the value of private credit collateral. A significant portion of these loans were made to software companies at valuations that assumed continued revenue growth. AI disruption and a slowing economy put those assumptions at risk. When fund marks have to come down, it hits earnings at financial institutions holding these assets.

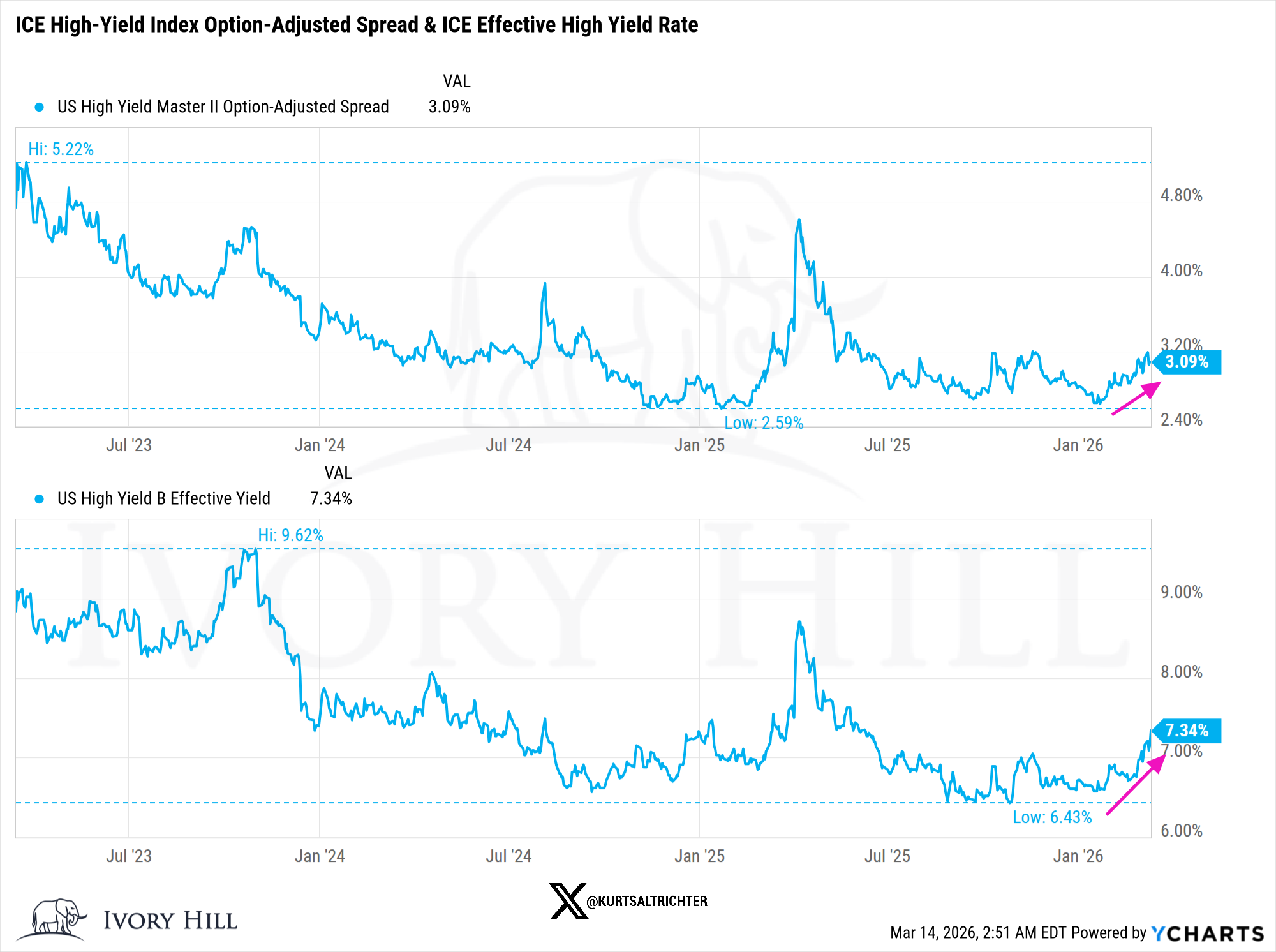

Is this 2008? No. The scale is different. The contagion pathways are different. But the pattern, opaque assets with illiquid redemption terms getting marked down in a risk-off environment, is one that has caused problems before. The financial sector has been quietly underperforming for this reason. Junk bond yields hit a three-month high of 7.34% last week. Credit spreads are in an early 2026 uptrend.

This is not a sell everything signal (yet). It is a know what you own signal. If you hold alternative credit funds or BDCs, now is the time to read the fine print on redemption terms and understand the underlying loan portfolios. Well, actually, before you invested in it, it was time to read the fine print. I got all of my clients out of private credit in 2022, following the headline news on BREIT limiting investor redemptions, forcing them to sell their casinos in Las Vegas. This does not end markets. But it adds another leg to the stool of things that could go wrong simultaneously. And that list is getting longer.

Worry #5: AI Is a Bubble, and It Is Popping

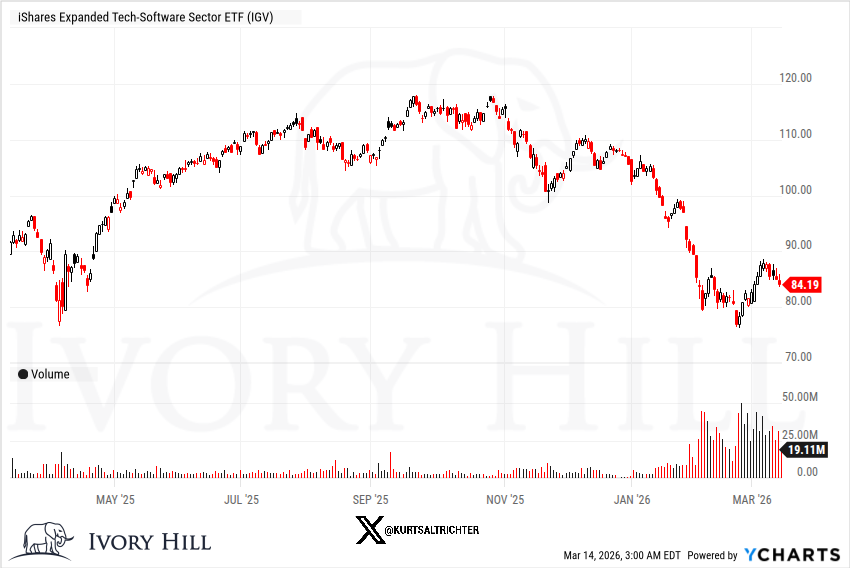

The OpenAI and Oracle data center cancellation headline from last week hit the market hard and reignited every concern that has been simmering since DeepSeek rattled tech stocks in January 2025. And those concerns were legitimate. That is a real problem for the stocks trading at the valuations that assume it will.

But here is what is getting lost. AVGO and ORCL both reported solid earnings last week with strong guidance. The software ETF IGV has bounced meaningfully off its February 24 low of $76.26. OpenAI’s latest model release with “extreme reasoning” capabilities generated genuine enthusiasm. The AI trade is not dead. It is digesting a lot of uncertainty about ROI timelines and competitive dynamics. I think this year is the year for AI to prove itself.

The line in the sand technically is $76.26 on IGV. That is the level the entire AI trade pivots around right now. If geopolitical volatility and growth fears drag it back through that level, AI anxiety is re-accelerating and tech leads the market lower. If it holds, the AI trade is in a consolidation, not a collapse.

Worry #6: The Stock Market Is Crashing

Let me give you the honest numbers as of Friday, March 13, 2026.

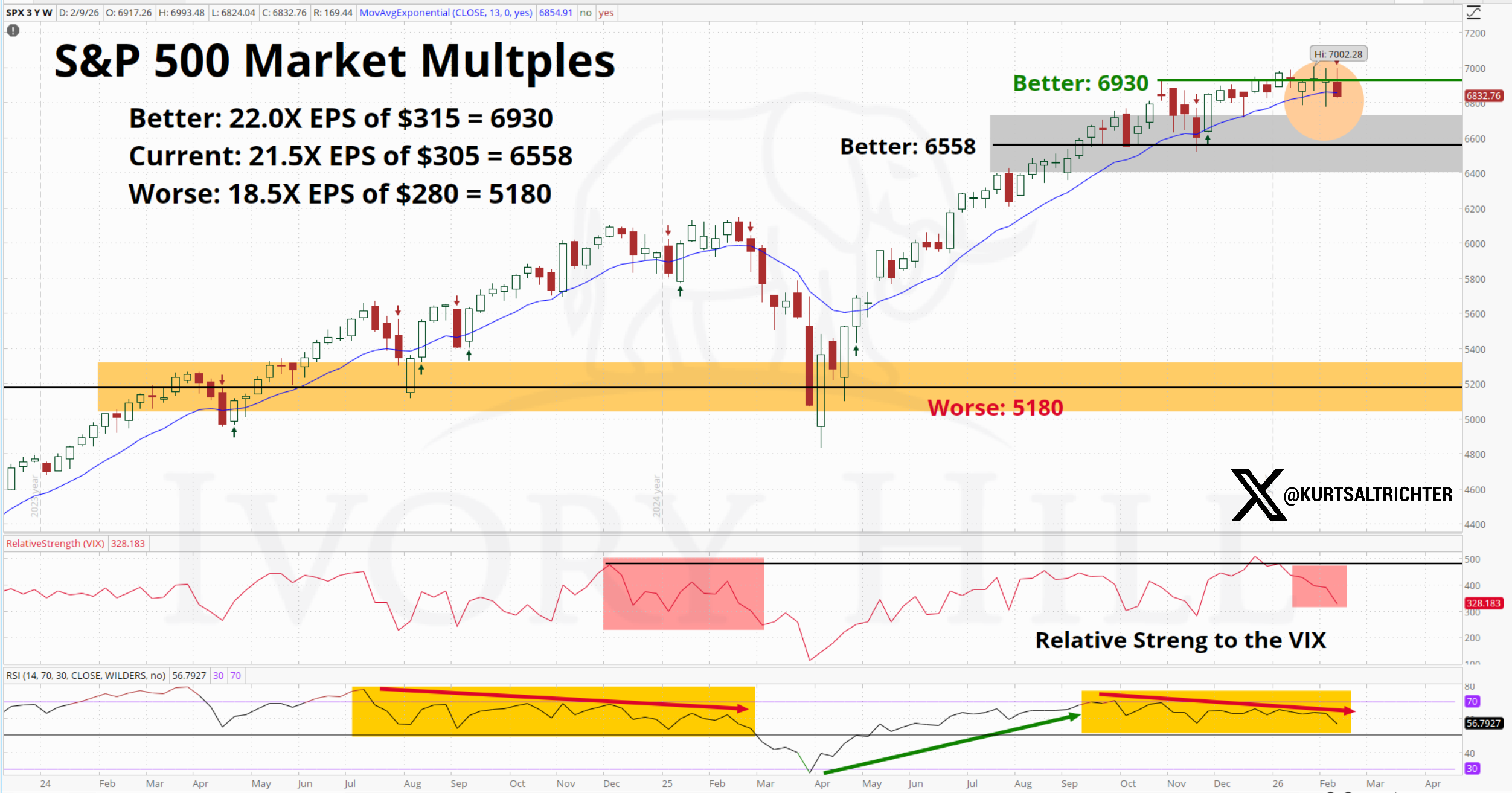

The S&P 500 closed at 6,632, down about ~3.3% year to date and approximately 4.3% off the all-time intraday high of 7,000 reached on January 28, 2026. The Dow closed at 46,548, down 0.28% on the day and now down over 4% from its February high above 48,500. The market has broken below its 50-day, 100-day, and 13-week moving averages. The S&P 500 has been trading below its 50-day moving average since February 27. The index closed out its third straight week of losses.

There are four technical similarities right now to early March 2025, which preceded last spring’s sharp selloff. That is not something to dismiss. The threat of a 20-25% correction is as elevated as it has been in almost exactly one year.

But here is the honest counterpoint. Fair value on the S&P 500 right now, using $305 in 2026 earnings estimates at a 21.5x multiple, is approximately 6,558. We are not far from fair value. The worst case scenario, using $280 EPS at an 18x-19x multiple, puts the floor around 5,040-5,320. That is real downside. But it requires multiple things to go wrong simultaneously: the Strait stays closed for months, stagflation is confirmed, and private credit stress spreads to major banks. That is a lot of dominoes.

The bull case, Hormuz resolves, AI stabilizes, growth holds: $6,930 on the S&P with a short-squeeze potential to 7,350 if we clear 7,000.

This is not a crash. It is a correction in the context of a bull market that has serious headwinds piling up at the same time. The difference matters enormously for how you should be positioned.

What I Am Actually Doing

Trimming overweight positions in high-multiple tech. Not selling tech entirely, trimming where we were overweight.

Holding energy oil stocks and commodities as a direct hedge against oil staying elevated. Energy equities did not fall hard even when oil dropped 18% intraday on Monday. That tells you the equity market does not believe oil is going back to $60.

Adding to our gold position. It is up 19.6% this year. It is the cleanest expression of two separate trades simultaneously: a geopolitical fear bid and a long-term currency debasement trade. Both of those stories have legs beyond this conflict.

Staying short duration on bonds. The 10-year at 4.26% is not yet in the danger zone, but there is no reason to reach for long bonds when the Fed is paralyzed and oil is actively inflationary. This is exactly where the 60/40 portfolio breaks down. Long bonds do not behave like a safe haven in this environment. They trade like stocks, and right now that is the last thing you want on the other side of your equity exposure.

Holding cash. Not a lot. But some. Because the best outcome here is that things get worse before they get better and you want the ability to buy quality at better prices.

Not panicking. Because the data does not support panic. It supports caution, selectivity, and knowing exactly what you own.

The market is pricing in a ceasefire. If it gets one, we rally. If it does not, we go lower. Everything else is a sideshow around that one variable right now.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.