What Sectors Should Outperform Under A Republican Sweep?

How Pro-Growth Policies, Sectoral Shifts, and Key Risks Shape the Path Forward for Equities and Economic Stability

CLIENT REMINDER:

If you haven’t already, please schedule your Q4 meeting (click here)

Thank you for the feedback on yesterday's report. I apologize for the length, and moving forward, I'll be more mindful of keeping these reports concise.

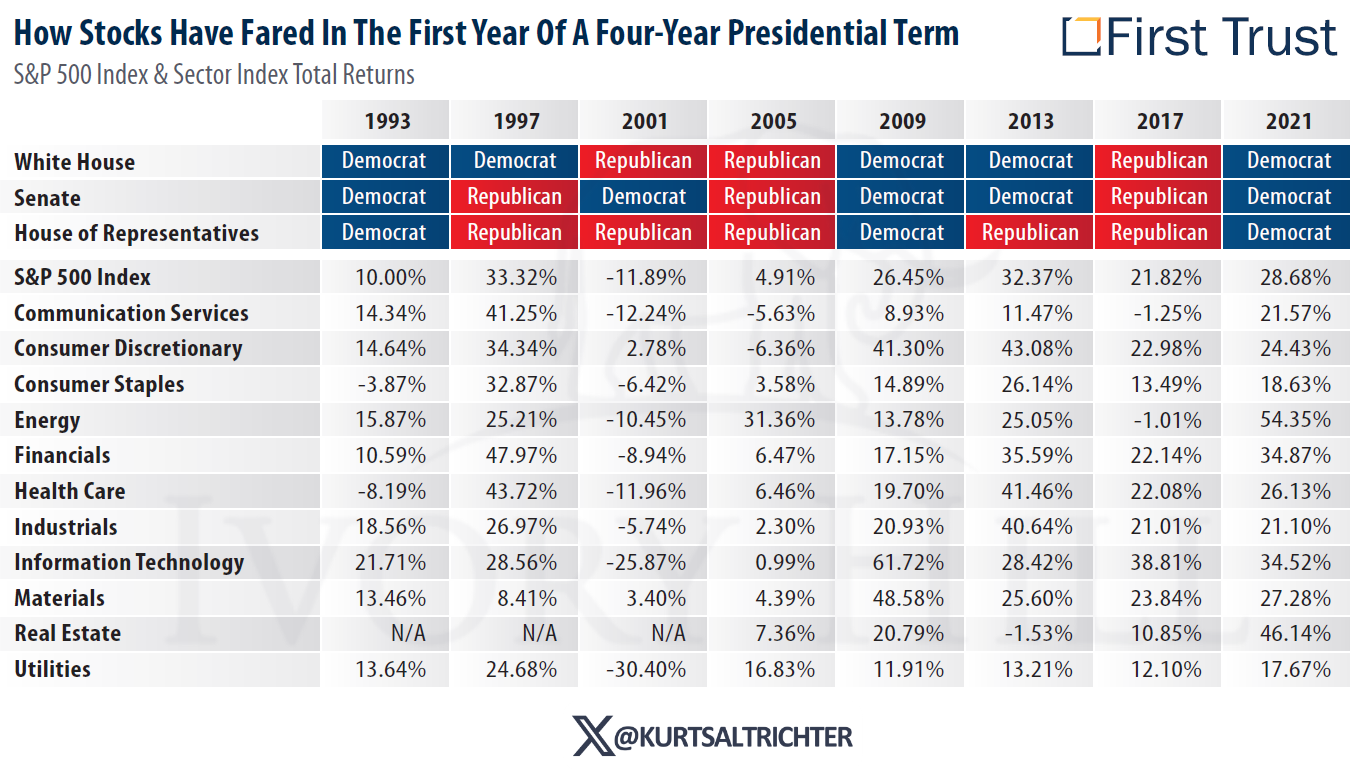

Donald Trump secured a second, non-consecutive term as President, making him only the second in history to achieve this after Grover Cleveland. In addition to Trump’s victory over Kamala Harris, Republicans reclaimed control of the Senate, and while the House of Representatives remains officially undecided, the substantial Republican gains make a Republican majority highly probable. This electoral result meets our “Good” scenario outlined in yesterday’s report and is factored into the current market reaction, as evidenced by the sharp surge in futures this morning and major indexes making new highs.

Market Impact

While this political shift is favorable, I do not consider it a full-scale “bullish gamechanger,” given that markets have already rallied hard this year on sky-high valuations. However, the political outcome is expected to catalyze a year-end rally, barring any unforeseen disruptions. Investors are now likely to anticipate and price in a pro-growth policy agenda, including an extension or even an increase of the Tax Cuts and Jobs Act (TJCA). Historical precedent in 2016 saw a 4.5% market rally post-Republican sweep, and in the current favorable macroeconomic climate—characterized by solid growth, declining inflation, and potential Fed rate cuts—an S&P 500 rally to, and even beyond, the 6,000 threshold before year-end is both probable and logical.

What sectors should outperform?

The anticipated Republican agenda emphasizes pro-growth policies through tax cuts, deregulation, and a focus on strengthening domestic industries, along with renewed trade negotiations. In line with this policy stance, sectors likely to outperform include:

Value Stocks (VTV)

Small Cap Equities (IWM)

Cyclicals and Domestic-Focused Sectors such as Industrials (XLI), Defense (ITA), Energy (XLE), Materials (XLB), Commodities (HAP, DBC), Transports (IYT), and Financials/Insurance (KBE, KRE, IYF, KIE).

What sectors should underperform?

On the other hand, sectors and asset classes that may underperform (though still benefit from an overall market rally) include:

Global Traders: Tech, Communications, Consumer Discretionary (XLK, XLC, XLY)

Large-Cap Growth (VUG)

China and Emerging Markets (FXI, VWO)

Defensive Sectors: Utilities, Staples, Health Care (XLU, XLP, XLV)

Large Importers (RTH)

This should further extend the rally we've seen since July, allowing the broader market to gain ground and potentially outpace bubble-cap tech.

Key Risks

This environment has risks, especially given potential responses to fiscal policies and international trade. Primary risks include:

Treasury Yields: Whether accurate or not, the market perceives Republican control in Washington as negative for debt and deficit levels. Consequently, Treasury yields could be reacting to this outlook, with the 10-year Treasury yield rising by 17 basis points this morning. This trend will likely continue until Republicans address rising debt and deficits. It could be due to the hundreds of billions in new Treasury issuance planned through the end of 2024, which is struggling to find buyers. Or perhaps the market is overreacting to inflation concerns, pushing yields higher than warranted. While I've been cautioning about the resurgence of inflation for months, I believe the market may be getting ahead of itself here.

Trade Wars: Trump does not hold unlimited power to impose tariffs unilaterally. His administration must first meet a specific burden of proof to “green light” tariffs against a country; once this condition is satisfied, he gains broad authority. This applies to China, where his powers are extensive. However, with other countries with formal agreements, such as Mexico—his powers are limited. Despite these distinctions, increased trade volatility is expected, and distinguishing facts from rhetoric may prove challenging. As a result, it’s reasonable to anticipate ongoing trade-related fluctuations.

What’s next?

Stocks: Bullish

Treasuries: Bearish

Gold: Neutral

Dollar: Bullish

House election results are the next key data point necessary to confirm a Republican sweep, which is likely but not guaranteed. In the Senate, a potential 55-45 Republican majority would strengthen support for GOP legislative initiatives.

Looking past the final election outcomes, the next significant developments will be cabinet appointments. These choices will clarify the new administration's priorities, helping us better understand their potential effects on the markets.

Bottom line: This likely gives us the “green light” for a year-end rally. Markets are likely to respond positively as attention shifts back to the Fed and stable economic growth. Similar to 2016, market watchers may overlook certain comments from Trump, meaning trade or fiscal policy concerns may not significantly impact markets until 2025. However, it would be prudent to prepare for potentially higher market volatility in 2025 compared to 2024.

This week's next key event will be the Federal Reserve meeting, where the central bank is expected to cut rates by a quarter-point, likely without any surprises. After this meeting, the inflation data will determine if the Fed cuts rates again. One notable takeaway, however, could be its view on the labor market. In its last meeting, the Fed signaled a shift in focus from inflation toward broader economic stability and labor conditions. With inflation largely “controlled,” it will be interesting to see if the Fed comments on the weaker-than-expected October jobs report. Powell's tone in the previous press conference hinted at some concerns about the economy’s direction, and he didn’t come across as fully confident about balanced risks. While recent data doesn’t indicate a significant shift in conditions, Powell's perspective on the job market could provide essential insights.

In the coming days and potentially weeks, we’ll fine-tune our strategies to align with the new political landscape, focusing on the key sectors highlighted above.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Email: kurt@ivoryhill.com | ivoryhill.com