This is a market that looks easy from a distance and pays poorly up close.

Low volatility and supportive breadth are masking a tighter risk box. Upside exists, but it is no longer free. From here, the difference between making money and giving it back comes down to respecting levels and avoiding emotional trades inside the range.

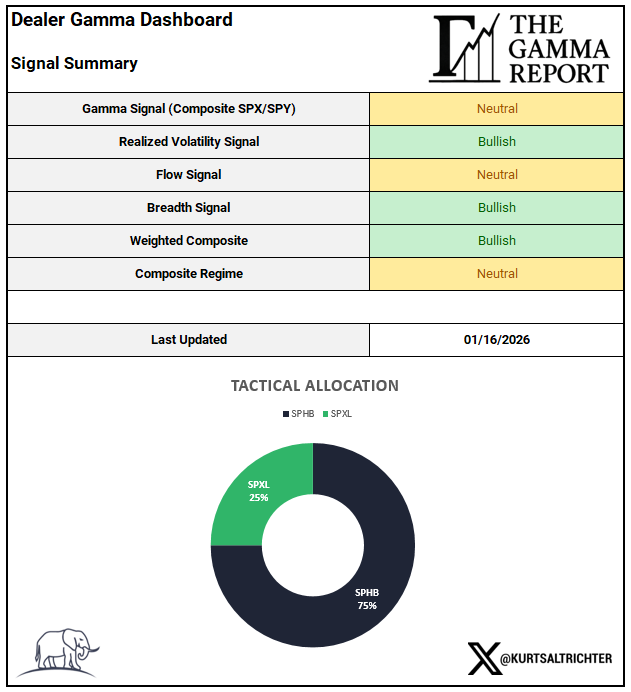

Dealer Gamma and Market Structure

Dealer gamma sits near neutral, not a tailwind but not a headwind either. When gamma is neutral, the market loses its automatic stabilizer button. Moves can extend, but they require real participation rather than mechanical hedging.

This moves the burden back onto breadth, volatility, and flows.

Without strong positive gamma, upside needs confirmation through participation. Without negative gamma, downside remains controlled unless something forces dealers to chase.

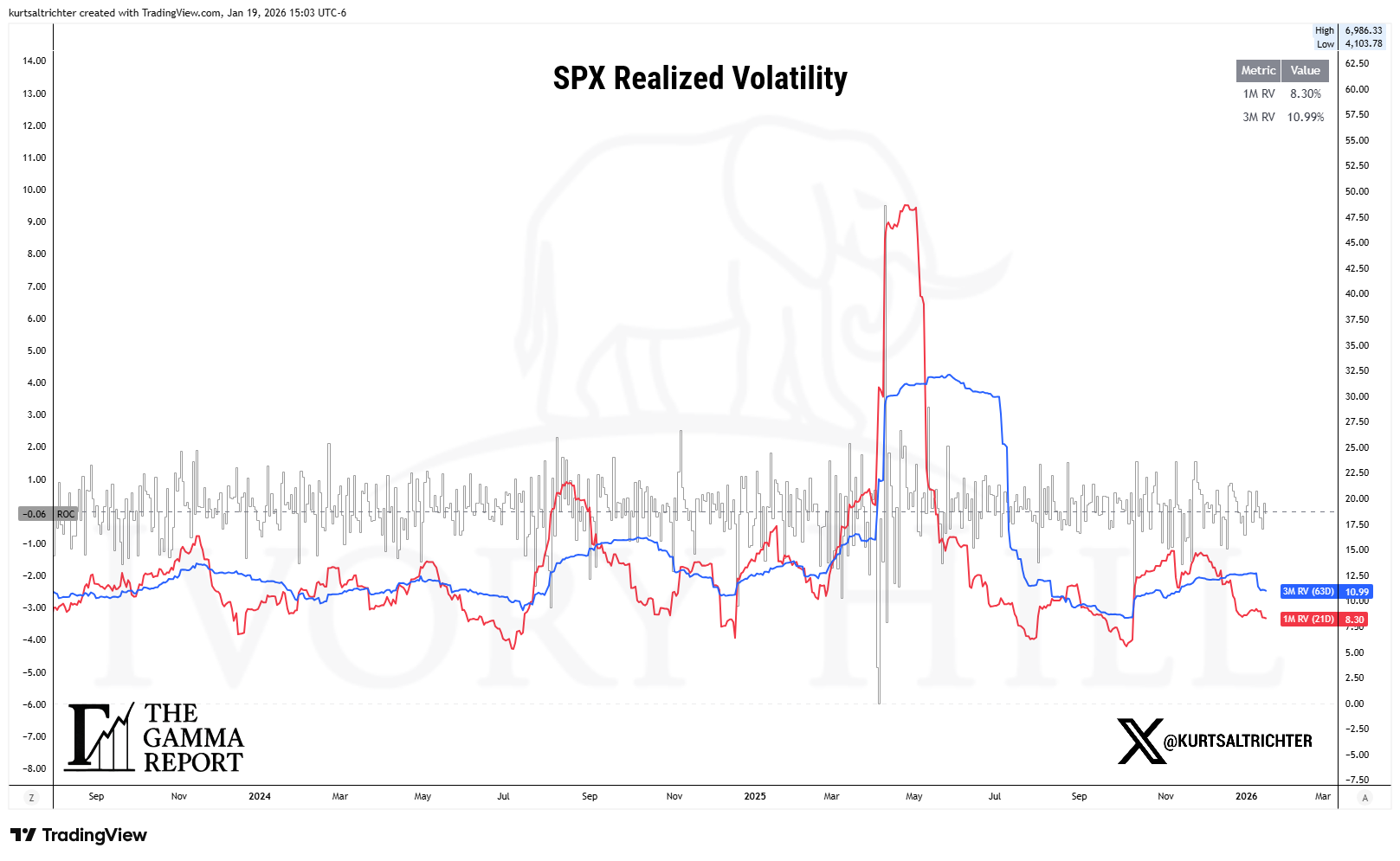

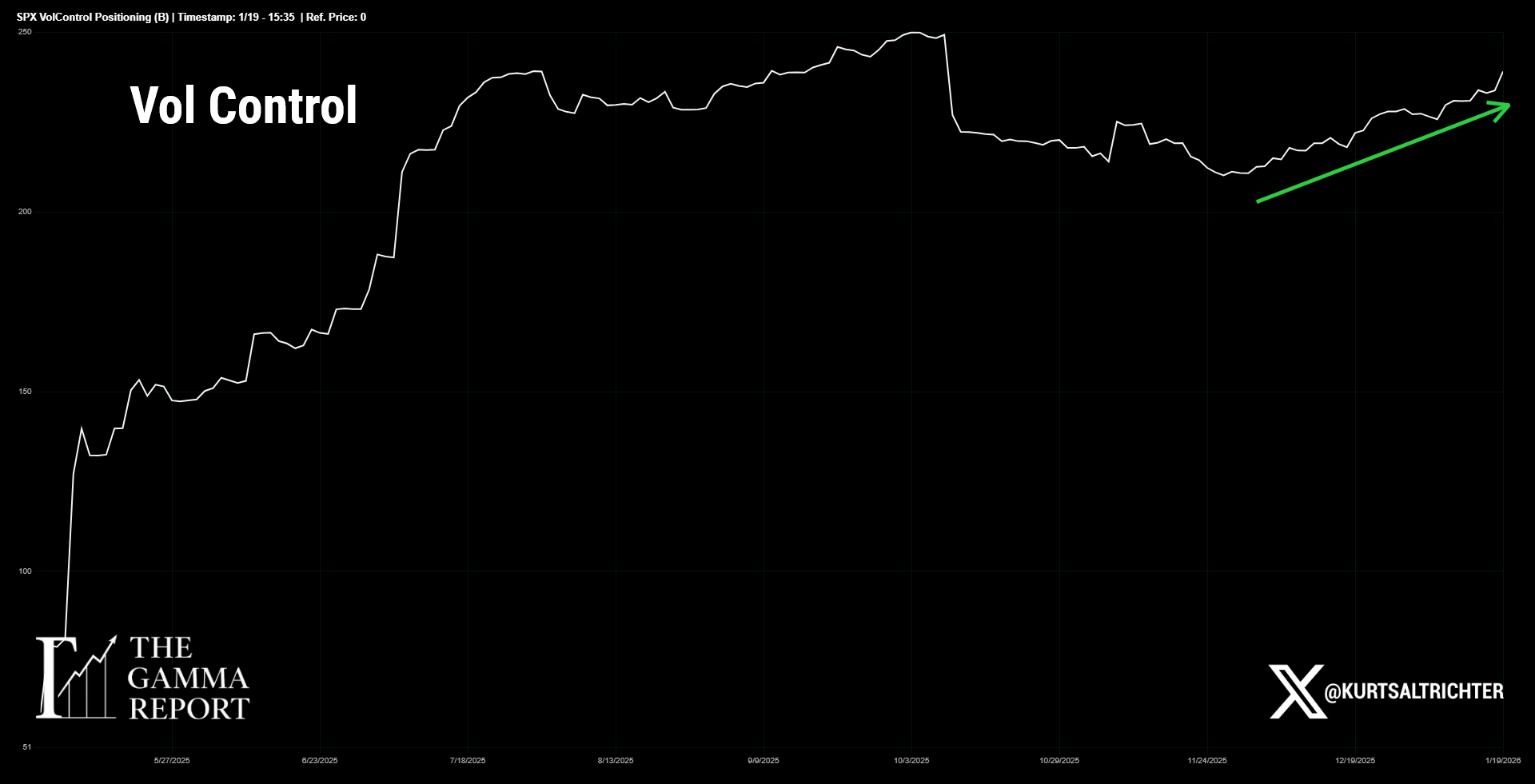

Volatility and Vol Control

Realized volatility continues to grind lower. One-month realized volatility sits near 8.30%, while three-month realized volatility is around 10.99%, both well below historical market stress thresholds.

Vol control strategies have responded exactly as expected. Exposure has been rebuilding steadily after the late 2025 drawdown. That acts as a slow, persistent buyer beneath the market.

This is important because it reduces crash risk but also caps momentum unless another flow source steps in.

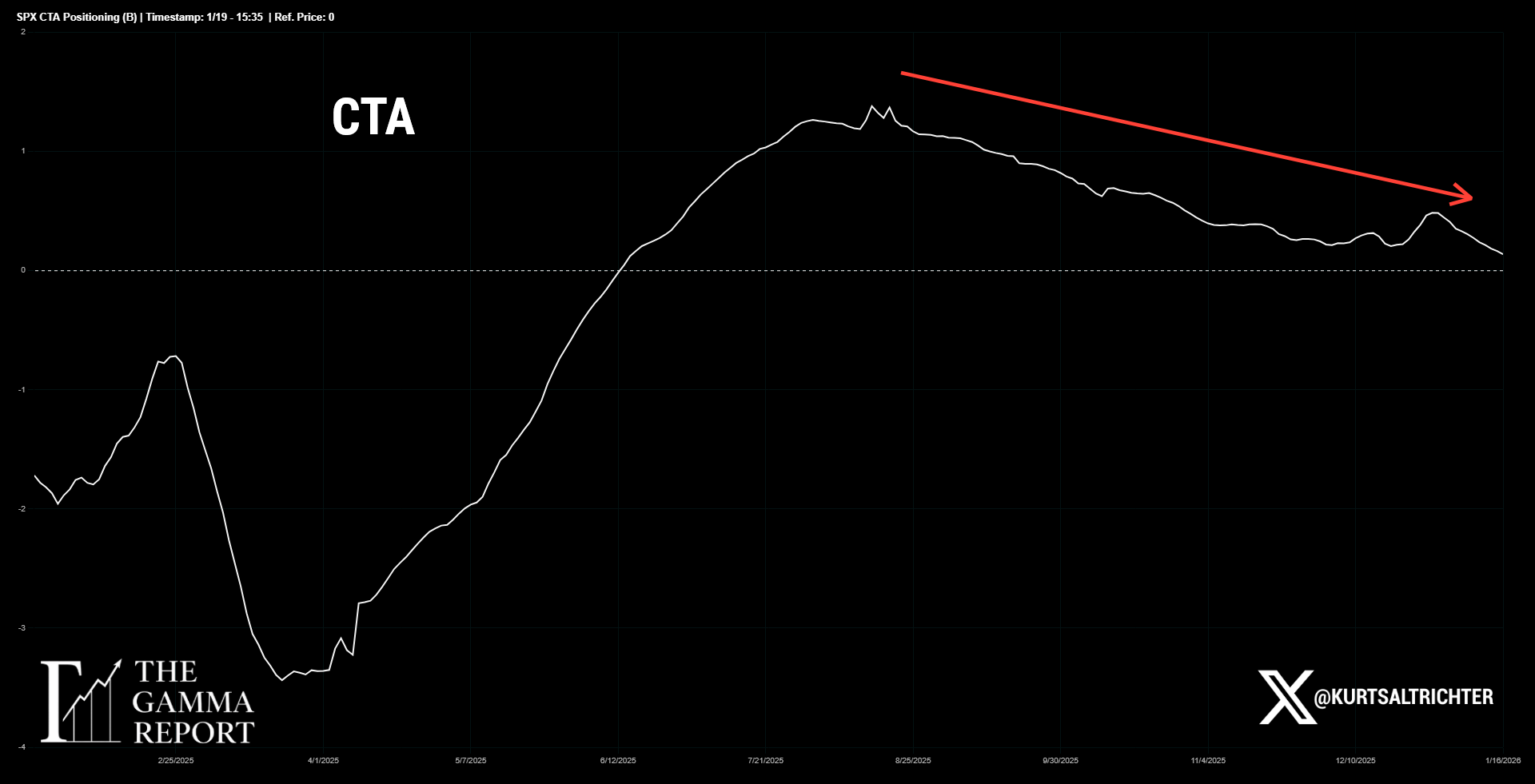

CTA Positioning

CTA exposure has rolled off its highs and is now flattening out. Trend models are no longer aggressively adding, but they are not outright sellers either.

This puts CTAs in wait and see mode.

When CTAs stop buying, and vol control stabilizes, markets tend to compress rather than trend. That fits what the price has been telling us for several sessions now.

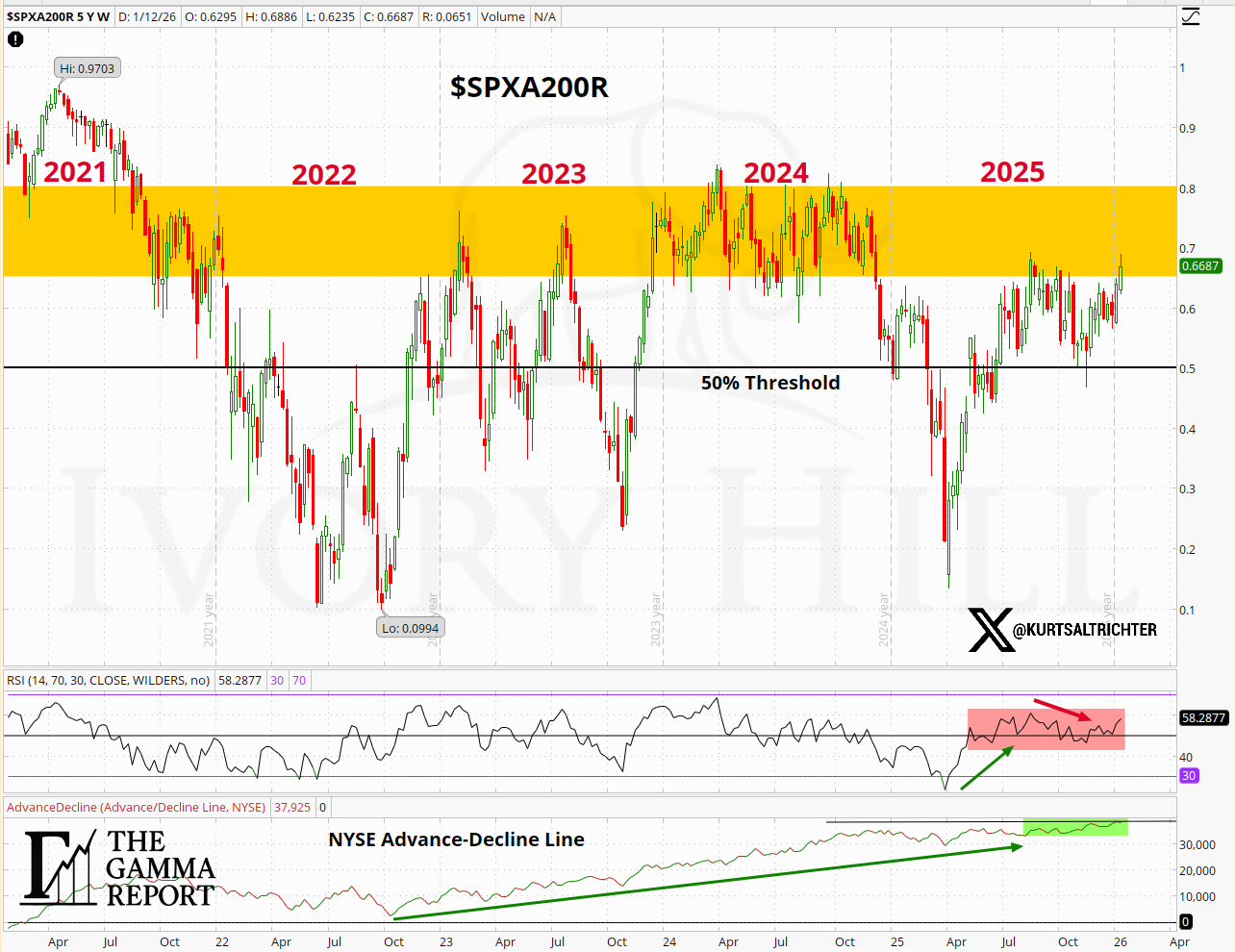

Breadth Still Doing the Heavy Lifting

Breadth remains constructive.

The advance-decline line continues to hold its uptrend and remains near cycle highs. That confirms participation beneath the surface, even as index-level momentum slows.

This is the single most important offset to softening flows. As long as breadth holds, downside should remain contained.

If breadth breaks, the entire setup changes.

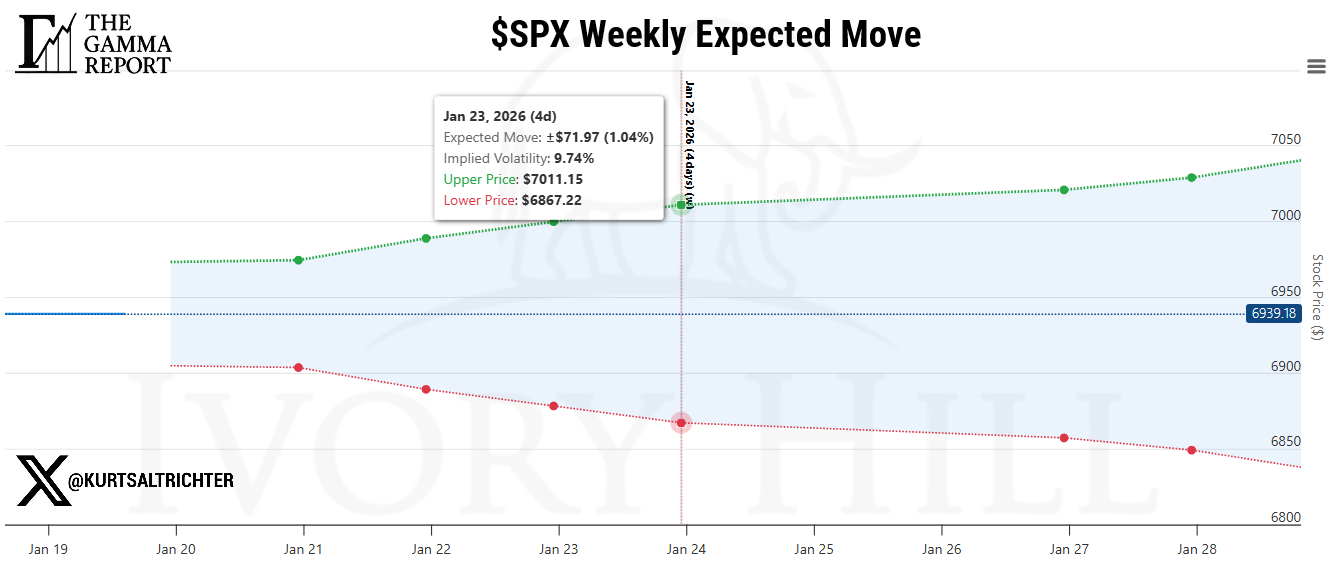

Price, Levels, and the Expected Move

The S&P 500 closed the week at 6940, sitting just above the gamma flip line near 6899.

The weekly expected move for the coming week is approximately ±1.04%, with an upper bound near 7011 and a lower bound near 6867.

The price remains within the dealer risk envelope.

That tells us two things. First, the market is not under stress. Second, chasing breakouts inside this range carries poor risk-to-reward.

Acceptance above the upper end of the expected move would force dealers to change their behavior. Acceptance below the gamma flip would do the same in the opposite direction.

Until then, this is a range that demands patience.

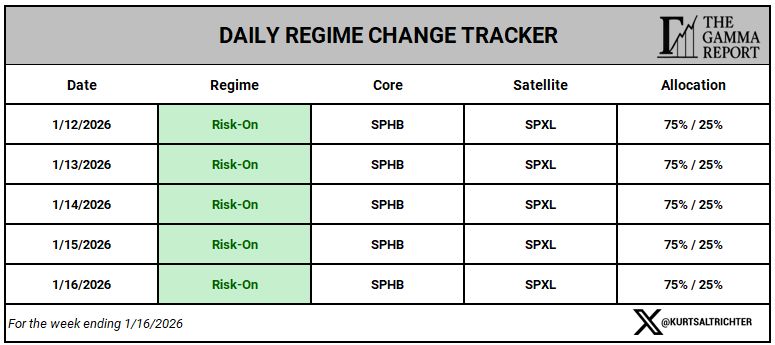

Tactical Allocation and Regime

The regime remains Risk On, with a 75% core allocation to SPHB and 25% satellite allocation to SPXL.

This reflects a market that is still constructive but no longer offering asymmetric upside. The structure favors quality beta with controlled leverage, not aggressive chasing.

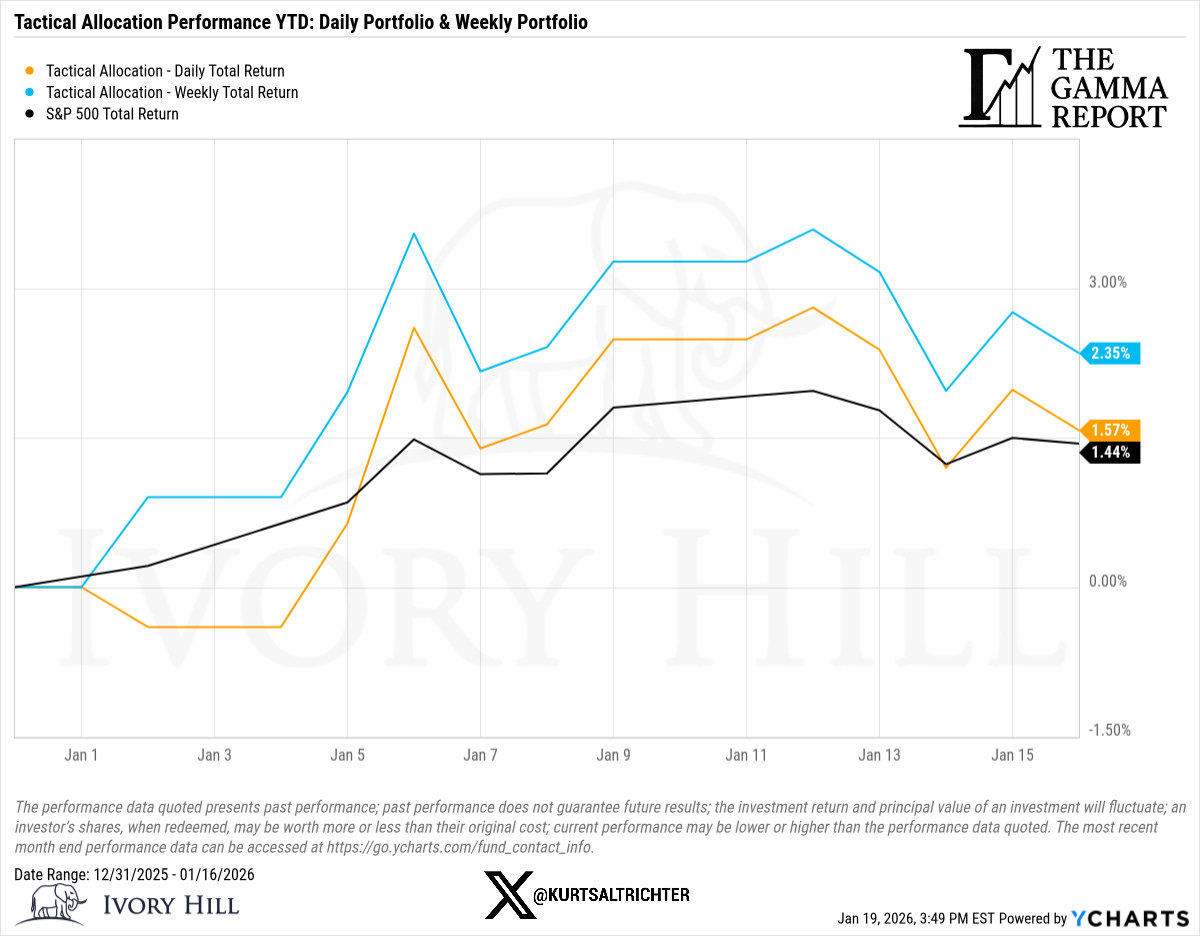

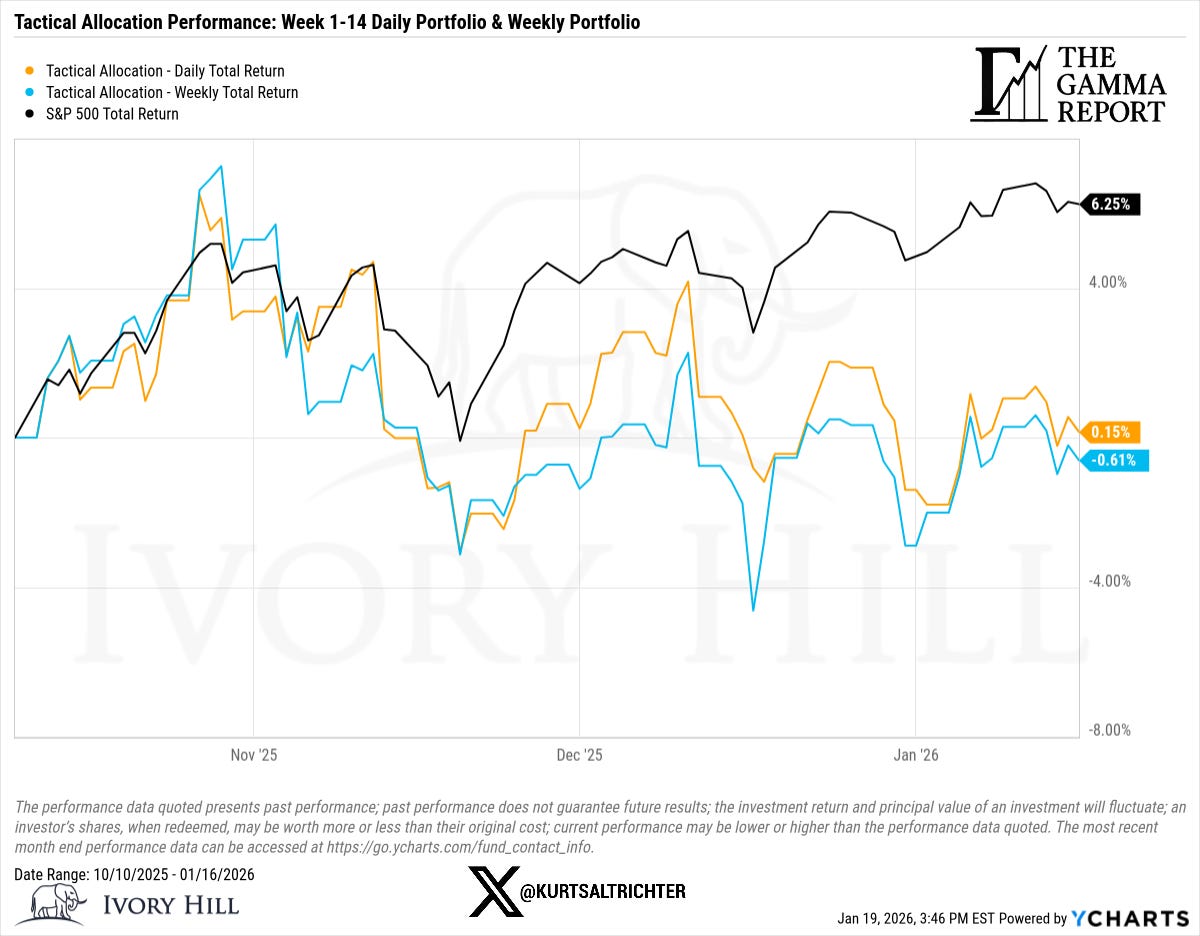

YTD Performance Update

Year to date, the tactical allocation has delivered 1.57%, compared with 1.44% for the S&P 500 over the same period. The weekly portfolio sits higher at 2.35%, reflecting the benefit of regime consistency and volatility control.

This is not about outperforming every day. It is about avoiding large drawdowns when the environment is uncertain and pressing exposure only when the setup improves.

The spread versus the index is not accidental. It comes from respecting the regime change, reducing exposure when volatility rises, and avoiding emotional decision-making inside tight ranges. That edge compounds over time.

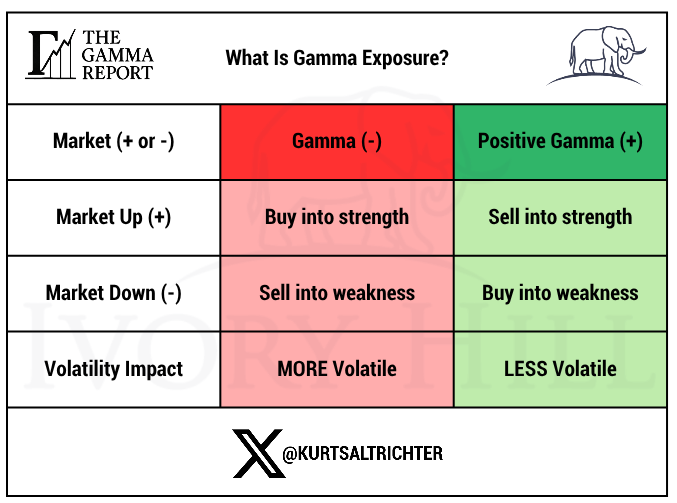

What Gamma Exposure Actually Means

When dealers are short gamma, they buy into strength and sell into weakness. Volatility expands, and trends overshoot.

When dealers are long gamma, they sell into strength and buy into weakness. Volatility compresses, and ranges dominate.

Right now, we are closer to the latter than the former.

That explains why momentum has slowed and why discipline matters more than conviction.

Bottom Line

This market is still investable, but it is not forgiving.

Breadth is strong. Volatility is contained. Flows are stabilizing.

That combination rewards process over prediction.

Stay patient. Respect the range. Let price prove acceptance before adding risk.

This is not a market that pays you to guess.

Feel free to use me as a sounding board.

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The Gamma Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.