Stocks Are Priced For Perfection

Full equity risk, minimal reward, and no cushion if expectations slip.

The Ivory Hill RiskSIGNAL™ remains green. Pullbacks are getting absorbed quickly because buyers keep stepping in at the same structural levels, confirming demand is still in control where it matters.

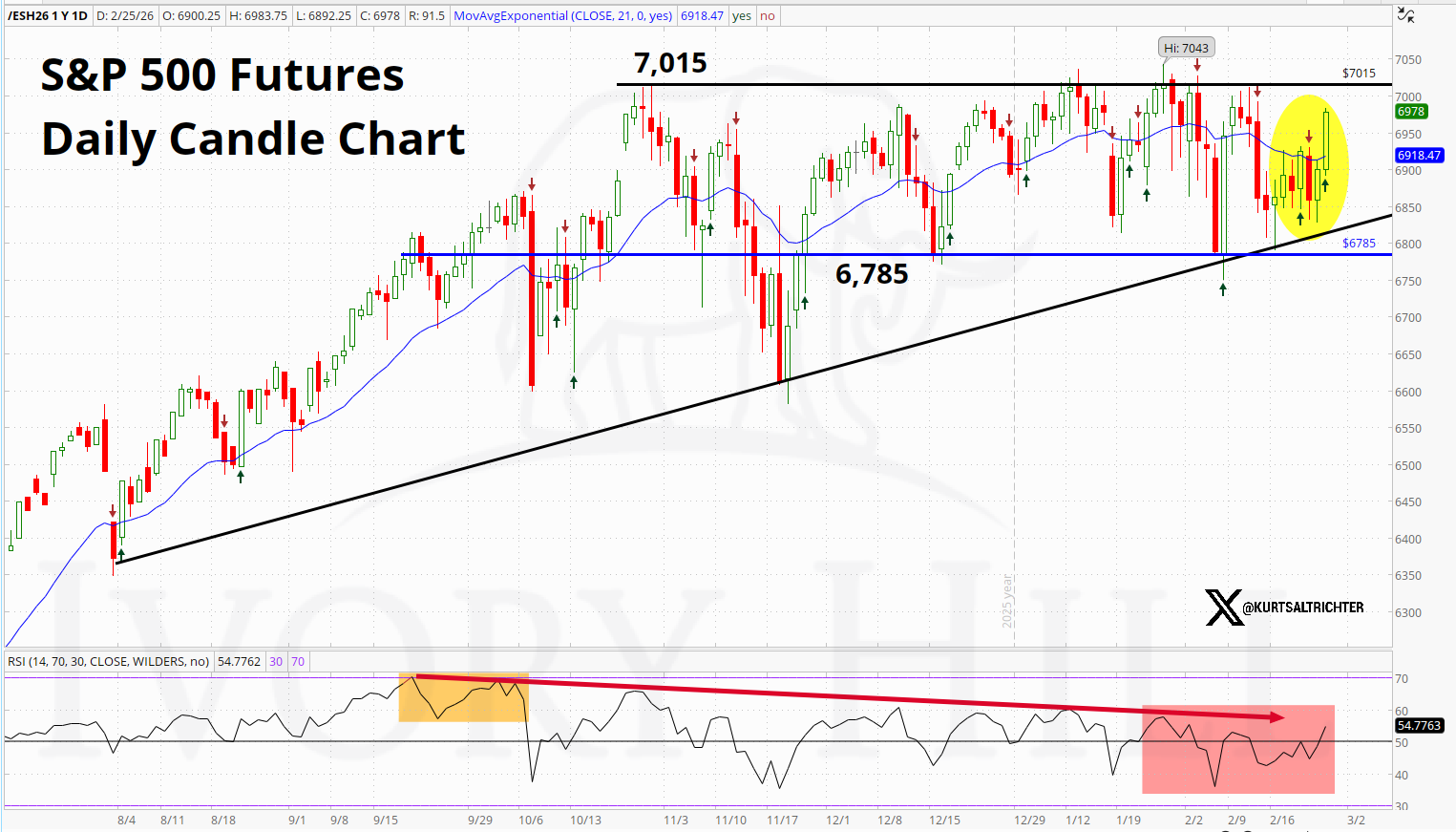

Technical Structure: Trend Intact, Conviction Fading

On the daily timeframe, the primary long-term uptrend in S&P 500 futures remains intact, but price action continues to lose structural quality. After breaking below the near-term moving average earlier last week, futures attempted to stabilize and have since drifted back above it. Instead of impulsive continuation higher, the market is now chopping sideways in a tight range beneath the 7,015 resistance level.

Rallies are lacking expansion and momentum confirmation. Each bounce has been met with selling pressure before reclaiming prior highs, while the downside is toward the 6,785 support zone, which continues to attract meaningful participation. The pattern is no longer a clean trend acceleration; it is rotational and indecisive.

Momentum reflects that deterioration. Daily RSI has recovered modestly from last week’s sub-50 breakdown but remains well below prior overbought readings and continues to show a clear bearish divergence versus price. Higher highs in price have not been confirmed by higher highs in momentum. That divergence remains unresolved.

In short, the trend has not broken, but the structure has weakened. The market is holding up, not breaking out or breaking down. As long as 7,015 caps the upside and RSI fails to expand, the burden of proof remains on the bulls.

Perfection is priced in. Protection is not at all priced in.

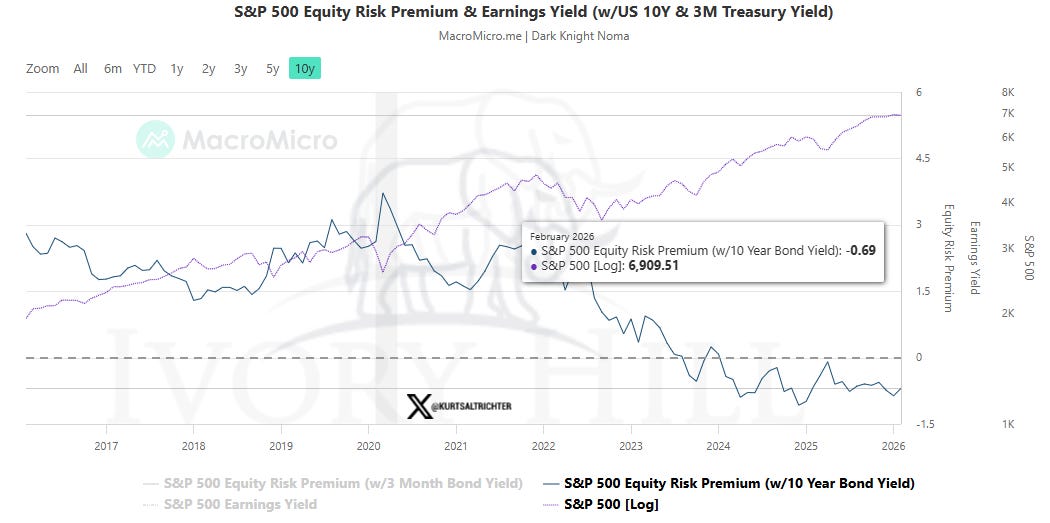

The Equity Risk Premium Has Collapsed

At the core of any disciplined investment process is a simple question: What am I being paid to take risk? Or said another way, right now, should I stay in Treasuries or buy stocks?

The equity risk premium calculation helps answer that.

The equity risk premium measures the additional return investors receive for owning stocks instead of “risk-free” U.S. Treasuries. It is one of the cleanest gauges of risk-reward in the broader market. When the premium is wide, investors are being compensated for volatility, drawdowns, and economic uncertainty. When it is narrow, they are assuming those risks with little incremental reward.

How It’s Calculated

There are variations in methodology, but the concept is consistent:

Calculate the earnings yield of the S&P 500.

This is the total reported earnings divided by the current index level.Subtract the yield on the 10-Year Treasury Note.

The result is the equity risk premium.

Using current reported earnings, not forward estimates:

Reported S&P 500 EPS: $294

S&P 500 index level: 6,940

Earnings yield: 4.24%

At the same time, the 10-Year Treasury yield is 4.17%.

That leaves an equity risk premium of just 0.07%.

Seven basis points.

Seven.

Essentially nothing.

In other words, investors are receiving virtually no excess yield for accepting equity volatility, recession risk, earnings risk, valuation risk, policy uncertainty, and geopolitical risk, rather than owning highly liquid, guaranteed U.S. government bonds yielding just under 4.20%.

That is historically very thin compensation for risk.

What This Implies

This does not mean stocks are going to fall tomorrow. Markets can remain elevated if earnings growth continues to deliver. Over the past three years, strong earnings follow-through justified elevated valuations and produced index returns of 17.9%, 25%, and 26.3%.

But today’s pricing leaves very little margin for error.

At an earnings yield near 4%, equities are not cheap relative to fixed income. With Treasury yields a rounding error away from 4.00%, the relative valuation argument for aggressive equity exposure is at best weak.

Current index levels are being supported by:

Elevated multiples

Confidence in continued earnings resilience

Assumptions that inflation does not re-accelerate

Expectations that policy remains supportive

A near-zero equity risk premium means those assumptions need to hold, or we will most likely have some downside.

Why It Matters Now

When the equity risk premium is this thin:

Even modest upside surprises do not create much valuation expansion.

Small disappointments can trigger outsized repricing and irrational moves to the downside.

Rising bond yields immediately pressure multiples.

Slowing earnings momentum quickly becomes a problem.

You do not need a catastrophe at these levels for markets to sell off. You only need expectations to be slightly too optimistic.

I am not arguing for abandoning US equities. I am arguing for investor awareness. On that, I should note that YTD we have carried our lowest exposure to US stocks in 5 years.

Broad index exposure today is not a deep value trade. It never was. It is a continuation trade.

With earnings yields compressed and volatility elevated since the late-January highs, downside risk relative to safe alternatives is meaningfully higher than it was when the equity risk premium was wider.

Here is my message:

If you are buying stocks at these levels, you are taking on maximum risk.

You are receiving very little incremental yield.

A lot needs to go right in 2026 for that to feel comfortable for anyone.

Let’s transition into where the fundamentals are today.

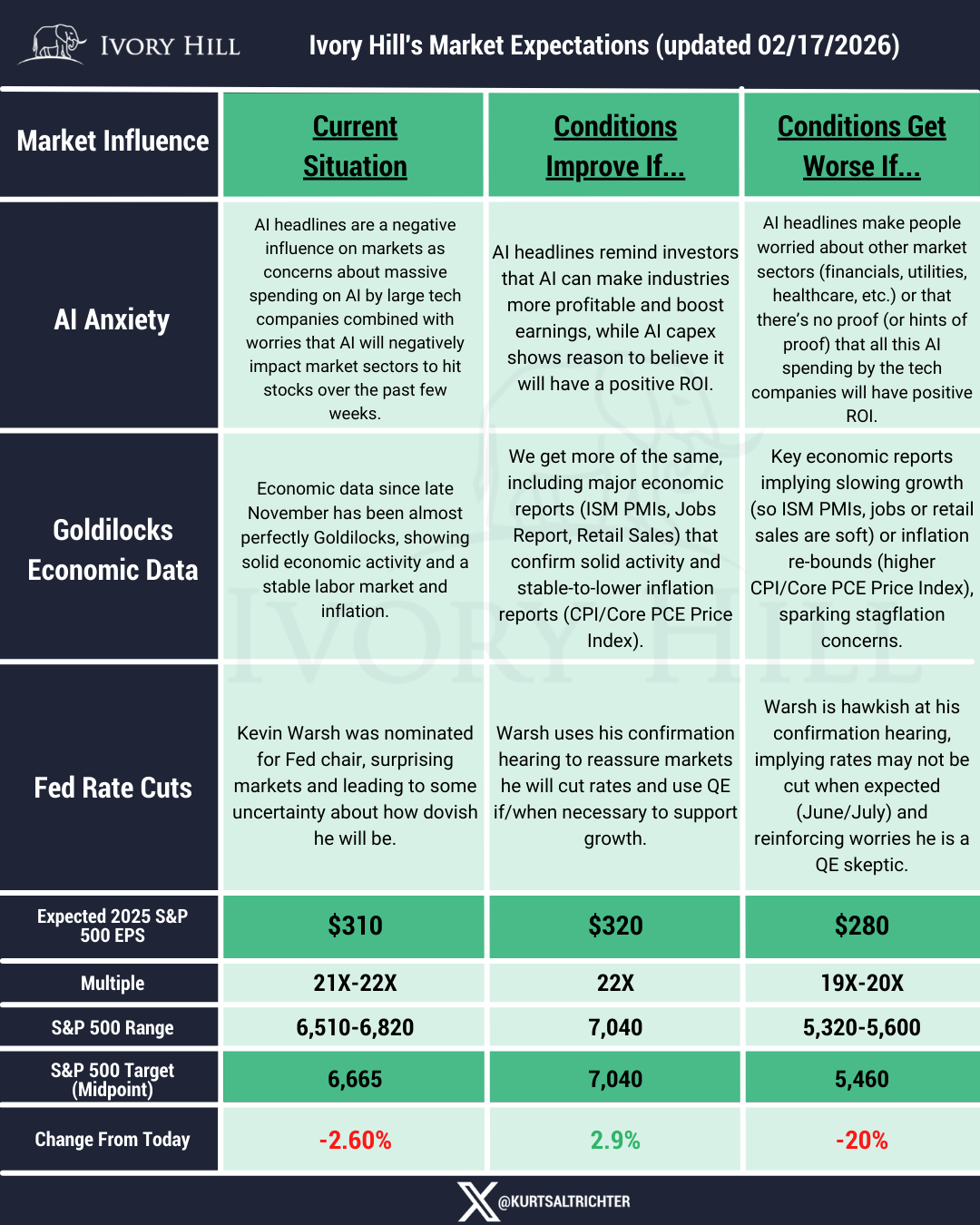

Market Expectations: Multiple Risk Is the Real Risk

The S&P 500 is effectively trading near 22x earnings.

The current baseline scenario assumes roughly $310 in 2025 EPS and supports an index level near 6,665. A better scenario, using 22x on $320 in earnings, implies 7,040. A worse scenario, using 19.5x on $280, implies 5,460.

That downside scenario is not fantasy math. It’s simply what happens when earnings expectations fall, and multiples shrink at the same time.

Right now, the market is priced for perfection. There is no downside priced in right now.

February Market Expectations Table: A New Dominant Influence

The February Market Multiple table highlights two critical changes:

AI Anxiety has replaced AI Enthusiasm as the dominant market influence.

This represents the first material narrative threat to the bull market in three years.

For the first time in this cycle, AI headlines are acting as a headwind instead of a tailwind. Concerns about heavy capex spending, uncertain ROI, and potential overinvestment have introduced volatility across the top 7 stocks.

This matters because multiples above 22x were largely tolerated due to expectations that AI would drive a multi-year earnings acceleration. Expected S&P 500 earnings moved above $300 per share largely on the back of that thesis.

If AI Anxiety grows, it impacts markets in two ways:

It pressures the multiple lower.

It reduces forward earnings expectations.

That combination is what creates downside asymmetry.

Importantly, that outcome has not materialized yet. The market is still trading around 22x. Economic data remains broadly Goldilocks. Inflation has cooled. ISM and jobs data have been stable. The Fed, despite the Warsh nomination introducing uncertainty, is still expected to cut in June or July.

So this is not a realized risk. It is an emerging threat.

The Three Pathways From Here

Conditions Improve If:

AI Anxiety fades, and capex spending shows credible ROI.

Economic data remains Goldilocks.

Warsh confirms a dovish bias and June/July cuts remain intact.

In that scenario, volatility falls, multiples hold, and earnings growth drives price higher.

Conditions Deteriorate If:

AI concerns spread to more sectors.

Growth slows or inflation firms.

The Fed turns more hawkish than expected.

That combo pressures earnings expectations and simultaneously shrinks the multiple. In that environment, a 20% to 30% decline would not be surprising. Not because of panic, but because valuation math resets. No one cares about fundamentals until they are down money.

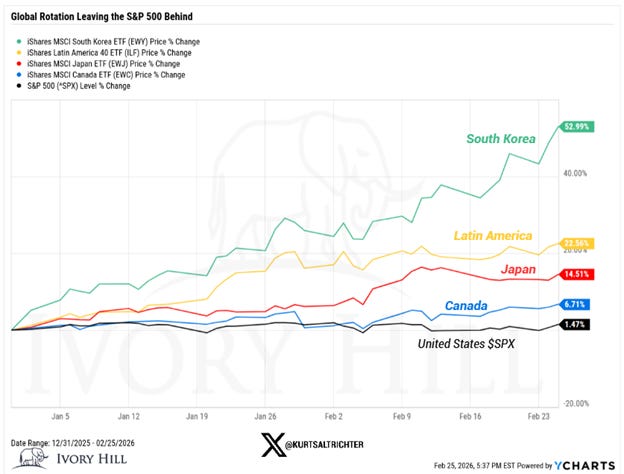

This is one of many reasons we are underweight U.S. equities and reallocating capital to markets with more favorable valuations and momentum, including Latin America, Japan, Canada, and South Korea.

Read more about this in my February 8th post below.

Bottom Line

The long-term trend remains intact.

The technical structure is weakening.

The equity risk premium is near zero.

The market multiple is elevated and dependent on execution.

AI has shifted from a tailwind to a headwind.

Economic data and Fed expectations are still supportive, but they must remain so.

When compensation for risk is this thin, small disappointments can havea huge impact. And when expectations are high, price becomes fragile.

That is where we stand today!

And remember - The one fact pertaining to all conditions is that they will change.

Follow me on X for more updates.

Best regards,

-Kurt

Schedule a call with me by clicking HERE

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Disclosure

The RiskSignal Report is published by Ivory Hill, LLC. All opinions and views expressed in this report reflect our analysis as of the date of publication and are subject to change without notice. The information contained herein is for informational and educational purposes only and should not be considered specific investment advice or a recommendation to buy or sell any security.

The data, models, and tactical allocations discussed in this report are designed to illustrate market structure and positioning trends and may differ from portfolio decisions made by Ivory Hill, LLC or its affiliates. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Ivory Hil, LLC, and its members, officers, directors, and employees expressly disclaim any and all liability for actions taken based on the information contained in this report.

Yeah....in agreement with about 20% cash personally. Problem is most money is owned by risk averse old people who aren't gonna take on high risk trades. And that's gonna get worse in next 5 to 10 years.